Since demographics, Freddie Mac says, drive the housing market, the company's economists focused part of its November Insights and Outlooks on the over age 55 population of homeowners. Sean Becketti, Chief Economist and others in his office point out that the press "overflows with questions about Millennials - when will they form households and buy homes?" While the direction the Millennials take in their housing choices will matter greatly, the choices made by the older generation, the article says, will be just as impactful.

First there is the matter of home equity. While almost 60 percent of the population is under 55, two thirds of the primary home equity is owned by those over 55.

The 55+ age group is currently composed of the very tail-end of the so-called Greatest Generation (those born before 1946) and Baby Boomers (born between 1946 and 1964). Each year over the next 15 a portion of Generation X will join the group and some of the existing 55+ will pass away.

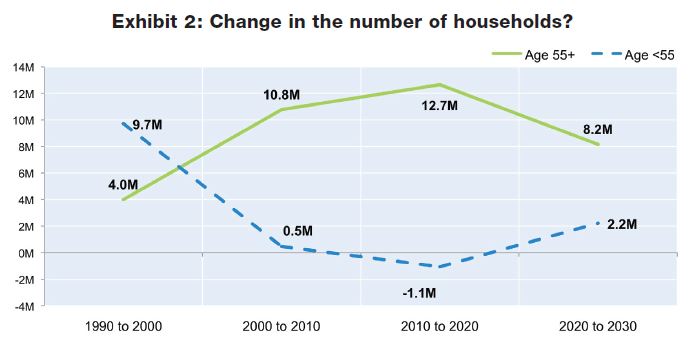

An Urban Institute report says that households over the age of 55 will account for more than half of the growth in households in the current decade (2010-2020). The number of older householders will grow by between 12.4 and 12.9 million while households headed by those 54 and younger will decline by between 0.4 and 1.7 million.

The choices made by this 55+ group will to a large extent define the housing opportunities available to those in the under 55 group, especially Millennials. If the older group decides to age in place that will limit the supply of homes available to the younger generation. If they avail themselves of senior focused housing that means revving up toward a demand not currently met. Housing finance will be affected if they decide to monetize the equity in their homes. Freddie Mac's economists say understanding this age group better is essential to anticipating the future of housing.

One reason the over 55 age group holds such a high share of the nation's home equity is the large share that have no mortgages on their primary residence. While only 19 percent of those under age 55 have no mortgage, 52 percent of the older group own their homes free and clear and so the entire cohort accounts for only one-third of all mortgage debt including home equity loans. And the incidence of mortgage debt continues to decline with age - only one-fifth of households aged 80+ have a mortgage on their primary residence.

The high wealth of the 55+ age group in aggregate masks the significant disparities in wealth within the group and a significant number remain challenged by housing costs. About 30 percent of the older households - 15 million - pay more than 30 percent of their income for housing (gross rent or housing payments). And half of those 15 million households devote over 50 percent of their income to housing costs. This demonstrates a need, Freddie Mac says, for affordable housing for this age group.

Freddie Mac says there are some significant issues regarding decisions of the over 55 age group. Among these are:

- Their future housing plans. Will more of them age in place or downsize? How will that decision affect housing supply and prices? How will the prospect of longer lifespans affect those decisions? Are they responsible for dependents - children or parents - for longer than they anticipated? Are their plans affected by other family members' geographic locations?

- How did the Great Recession impact this group? How greatly were retirements delayed because of financial set-backs? Did the recession have different impacts on the already retired as opposed to the not-quite retired?

- Does this generation need better information about their housing alternatives? How well do they understand their financial situation? Is age appropriate housing counseling readily available? How well are affordable housing needs being addressed for this age group?

- How will the 55+ group manage their housing wealth?

- How is the construction industry adapting to the growth in 55+ households?

Freddie Mac says the answers to some of these questions are already apparent while others will require speculation. It plans to address these concerns in future editions of Insights.