Most households buy a home to live in and raise a family. Consequently, they may not view a home as a financial asset in the same way they view their cash savings or their retirement accounts.

Only half of American workers are confident that they have or will have enough in savings to fund a comfortable retirement.

These are two seemingly disparate statements, but a new study from the Urban Institute (UI) says the first could provide a partial solution to the second. A home is the most commonly owned asset in America and the most valuable one. It can be a critical source of financial security for elderly households that lack other income and savings.

The study, conducted by Laurie Goodman, Karan Kaul and Jun Zhu, was commissioned by Finance of America Reverse to find how many borrowers could benefit from equity extraction, the amount of equity they could extract, and how these might vary by income, race, and wealth. The analysis was conducted using data from the 2016 Survey of Consumer Finances (SCF).

Concerns about retirement arises from discussions about changing Social Security, rising medical and long-term care costs, the shift away from defined benefit pension plans to 401(k) and IRAs that depend on employee contributions and investment returns, and longer life expectances that mean the money must last longer. Many studies predict that the next generation of retirees may see a decline in their living standards.

While homeownership has dropped overall by about 6 percentage points, to 63.7 percent, since the housing boom, the rate for those over 65 is 78.2 percent. Homeownership rates also exceed ownership of most other financial assets; only 52.1 percent of households have retirement accounts, 19.4 percent own cash-value life insurance, 13.9 percent have stocks and 8.6 percent have savings bonds. For most Americans, their principal residence is their most valuable asset. Even where there are other assets, that cash value is dwarfed by the median $185,000 value of their homes and their equity is the largest source of net worth. UI points out that that the lower that net worth, the larger is the share made up of home equity and while black, Asian, and Hispanic households have a much lower homeownership rate than white households, where they do own, equity makes up a greater share of their overall wealth.

Extracting all or part of home equity would allow financially constrained senior households to access cash, possibly eliminating the need to cut spending on essentials. Higher income households could leverage that equity to modify their homes and to make improvements and age in place more safely and conveniently. Extraction mechanisms include Federal Housing Administration (FHA)-insured Home Equity Conversion Mortgages (HECMs), closed-end home equity loans, home equity lines of credit (HELOCs), and cash-out refinancing. Selling and renting or buying a less expensive home is another option.

Yet UI says that few retirees tap into their home equity, and most who do appear prompted by a serious financial shock. A Fannie Mae survey of homeowners over age 55 found 80 percent were "not at all interested" in tapping into home equity in retirement. They were especially disinclined to use a reverse mortgage.

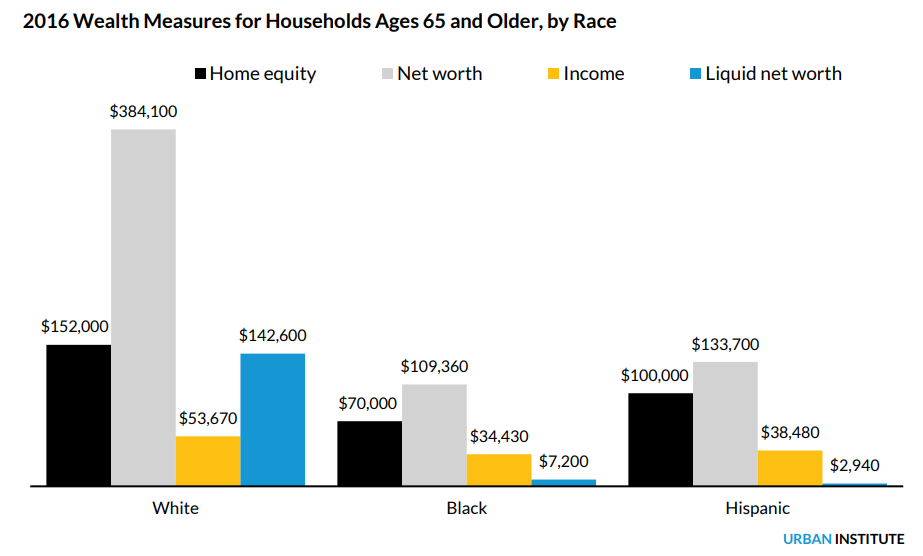

UI looked at household wealth by race along four dimensions, total net, housing wealth, income, and liquid assets.

Although black and Hispanic homeowners lag white homeowners along all four measures, the difference in liquid net worth is especially striking and indicate that black and Hispanic senior households are disproportionately more likely than white senior households to deplete their savings sooner, and that home equity represents a larger share of their net equity than in white households.

The study broke out the 26 million owner households aged 65 or older into four annual income groups; those earning up to $20,000 (3.3 million), those earning $20,000 to $40,000 (6.8 million), $40,000 to $60,000 (4.7 million) and more than $60,000 (11 million). The last group was eliminated from the analysis under the assumption they would not need to tap their equity.

The lowest income group had aggregate home equity of $406.9 billion, but after eliminating those with high liquid net worth (over $50K) who may not need to borrow and those with too little home equity (under $100K) to be worthwhile, the number of households that could benefit drops from 3.3 million to 921,000 with aggregate home equity of $208 billion. When the same analysis was performed on the second lowest group, their numbers fell from 6.8 million to 1.6 million and $354 billion in equity. There were 810,000 households remaining in the third group with equity wealth of $211 billion. The aggregate after the screening was 3.3 million households, 13 percent of all households over the age of 65. Their combined home equity wealth was more than $775 billion. A disproportionate share of these households would be minorities.

This is a staggering amount of home equity wealth, and it is widely distributed among millions of households. Even if the numbers were adjusted to account for factors such as HECM borrowing limits or that many households will not tap equity, the sheer scale of the numbers suggests that home equity lending could be a larger market. "Even if just 10 percent of the estimated 3.3 million households tapped into their home equity, that would be 330,000 households, more than six times the current annual HECM endorsement count of roughly 50,000 loans."

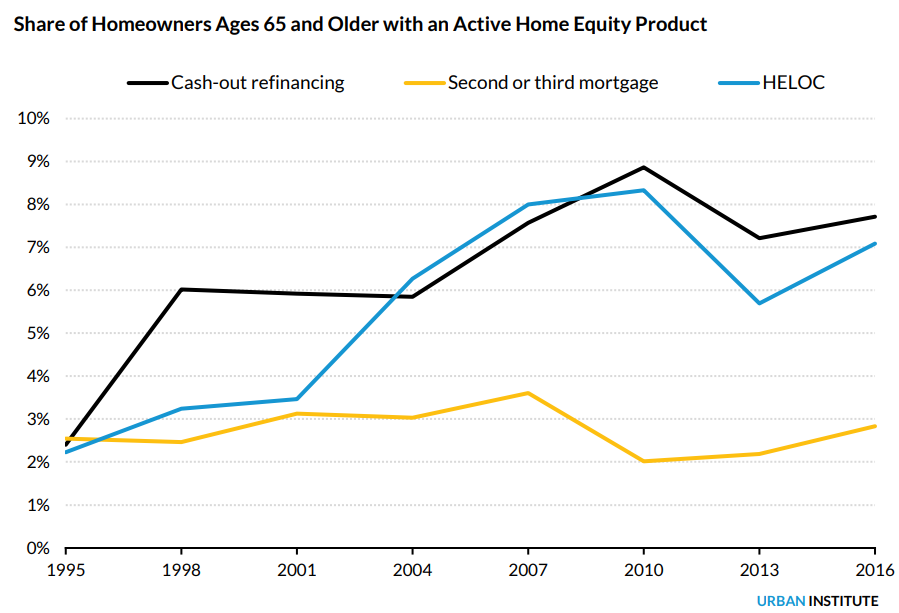

Still, current rates of extraction are low. The survey dataset does not have information on reverse mortgages but does have data on HELOCs, cash out refinances, and second mortgages and information on borrowers who use them.

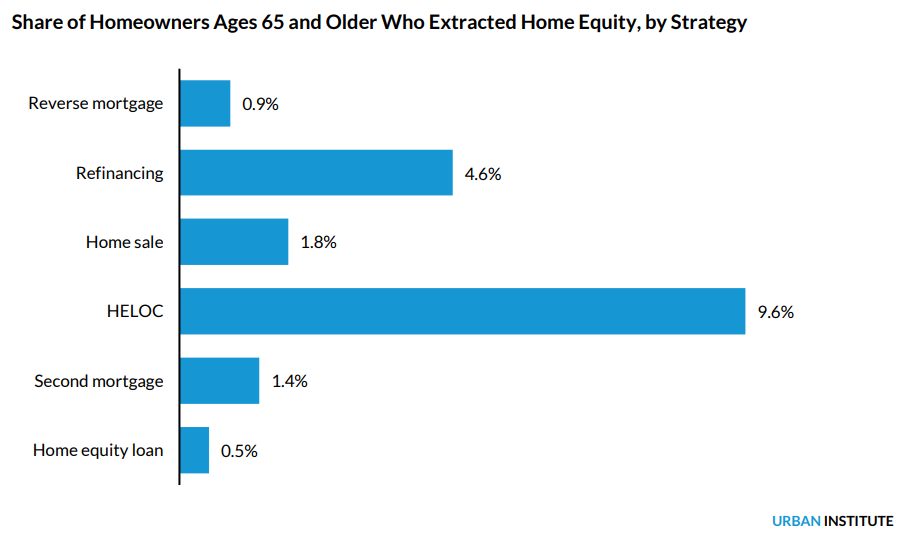

Additional usage information is available from the Health and Retirement Study (HRS) conducted by the University of Michigan. The latest data, from 2014, shows 11.4 percent of older homeowners had an active equity loan, HELOC, or second mortgage and, during the two years preceding the survey only 1.4 percent took a cash-out refinance, 1.8 percent sold their home, and 0.9 percent used a reverse mortgage.

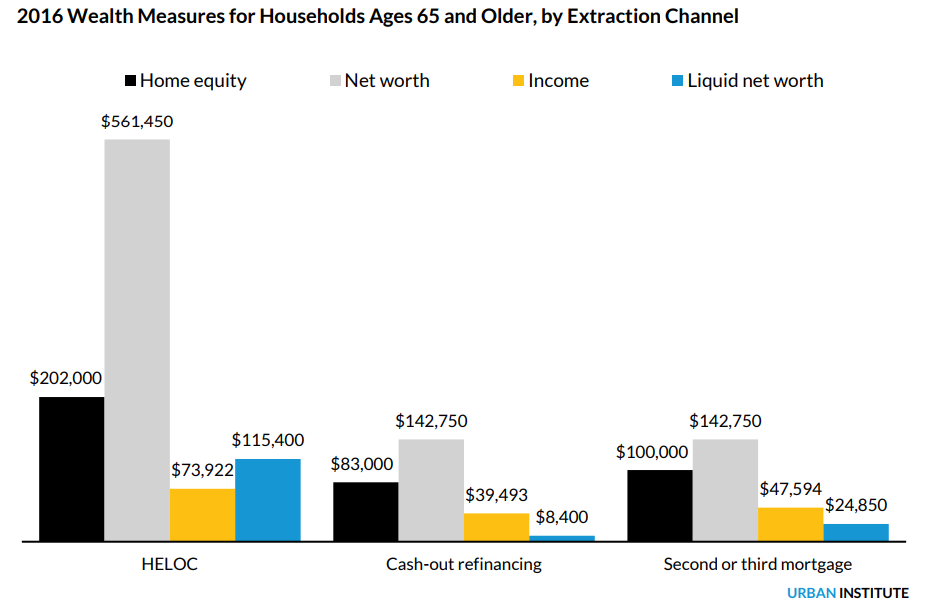

The SCF data indicates that HELOC borrowers are more affluent than those who extract equity through a cash-out refinance or a second mortgage and other research shows reverse mortgages borrowers are less wealthy than HELOC borrowers.

UI says impediments to equity extraction include an aversion to debt and a general desire to stay financially conservative, wanting to leave a bequest or save for emergencies, fear of losing the home, product complexity, high costs, and fear of misinformation and fraud. However, there are reasons to assume lending volumes could grow; the sheer size of the potential market is the largest.

That market is destined to grow as the population ages. Twenty-five percent of Americans were over 65 in 2007, 32 percent today. The share of older black homeowners has nearly doubled, from 19 to 36 percent, white homeowners from 28 to 34 percent, and Hispanic homeowners from 9 to 15 percent. Even if extraction rates remain constant, the aging of the population will expand the market. The share of seniors carrying a mortgage and the outstanding balance have also increased, from 21 percent with a median debt of $16,793 in 1989 to 41 percent with a balance of $72,000 today. "Many households carrying mortgage debt into retirement will likely not be able to afford monthly payments and could access liquidity and smoothen consumption with a reverse mortgage," the authors say.

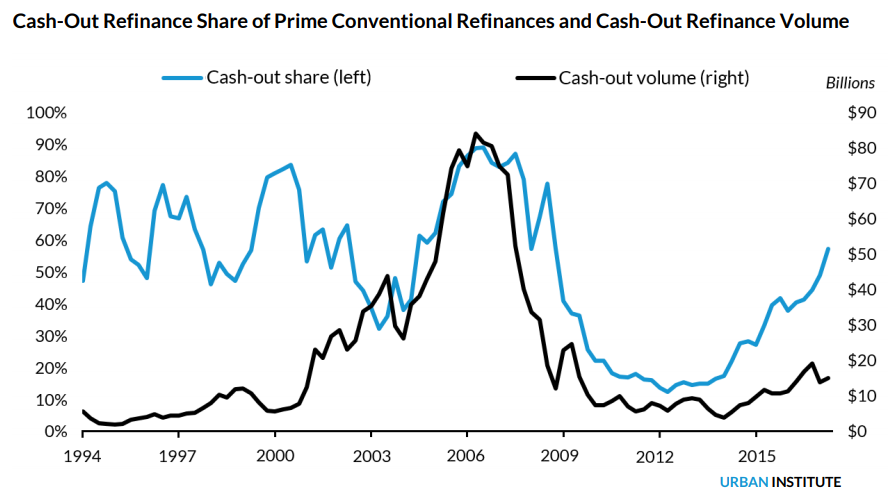

In addition, equity extraction is often associated with home price growth and current date regarding cash-out refinances indicate this is happening. Freddie Mac's quarterly refinance statistics show cash-out refinances increased to 57 percent of all refis in the second quarter of 2017. In 2006, at the peak of the housing bubble, the share was nearly 90 percent, falling to 10 percent by 2012. The money cashed out, however, remains low, reflected that, in a low rate environment, rate-term refinances rather than equity extraction remains the primary driver.

Similarly, after contracting significantly during the housing crisis, HECM lending volume has stabilized. These endorsements began increasing substantially in the early- to mid-2000s as house prices rose rapidly, peaking at 114,700 HECMs in 2009, then retreating during the bust to about 55,000 by 2012. Since then, HECM endorsements have consistently remained between 50,000 and 60,000 a year.

The UI analysts conclude that millions of households lack adequate income and savings to live comfortably during retirement but possess a significant amount of home equity wealth. If these households were to liquify some of that equity they could live more comfortably but existing data shows few seniors are doing so.

There are reasons to expect senior equity extraction volumes to increase as more Americans retire and as more of them carry first-mortgage debt into requirement and may have a stronger need to tap their home equity than prior generations. How much it will expand will depend, to some extent, on the industry and policymakers' ability to ease barriers to equity extraction.