Legality issues surrounding the foreclosure process are a hot topic. In no way is this good news for housing. Besides adding more uncertainty to an already uber uncertain marketplace (home prices specifically), these precedings are already affecting pending transactions of new homebuyers and originators.

We shared this feedback from an originator who has already experienced a delay in the closing of their purchase transaction because the property was a JP Morgan Chase foreclosure...

"I have a client in Florida that closed on his sale in Florida on Thursday, and was supposed to close on his purchase of a Fannie Mae owned home this Wednesday. Well, last Friday he received a notice from the title company that they have indefinitely suspended the sale, due to the previous owner & servicer being JPM Chase. However, the borrower was foreclosed on two years ago. So now, with a wife and two dogs, my client has nowhere to go. The auction company gave him until today to cancel and get a refund of his deposit, or to extend for 6 months, but with no direction on a closing date."

How long will this mess take to sort out? When can loan closings go on as usual? What about rate locks?

You can either wait it out or get a refund on/tear up your earnest money deposit and find another property. Obviously you should avoid foreclosed properties if you withdraw your application and restart your home search. If you decide to wait it out, you can get a lock extension, but at this point I would try and relock at lower rates. Don't blame your loan originator for these problems. Honestly, so far from what I can tell......

This is a procedural loophole. Lots of noise surrounding a technicality. But why does no one stop to consider the cascading consequences? Felix Salmon does that neatly below.

--------------------------------------------------------------

On Reuters, Felix Salmon writes Where is the Forclosure Mess Leading?

Yves Smith and 4closureFraud have doing an astonishingly good job of keeping on top of all of the legal matters surrounding mortgage foreclosure. There are lots of them — do you know what phony allonges are? — and they are all very complicated, and they vary from state to state and from bank to bank, with the result that it’s really hard to sum it all up in a simple overview. But it’s impossible to read those sites and not conclude that we’re at the early stages of an absolutely monster legal mess.

Any one of Smith’s posts is astonishing enough — try here for a good starter, although you could do worse than to start here or here if you’re in Florida — but put them all together, and it becomes clear that the mother of all legal messes has already emerged from the foreclosure crisis, and threatens not only a large chunk of the financial system but also venerable civic institutions, like the courts, which have thus far emerged from the crisis largely unscathed.

While there’s some evidence that Congress is willing to find a bank-friendly way out of this mess, I don’t think that’s going to fly, not when state AGs are already filing lawsuits against the likes of GMAC.

Argentina’s sovereign default has been called “the slowest trainwreck in history”, but this one might turn out to be slower, bigger, and much less fair. Millions of people have already lost their houses to lenders who didn’t have the proper paperwork, and it’s unlikely they will ever get any redress. For people who haven’t yet been foreclosed upon, however, it could now be a very long time before they lose their house.

The big-picture consequences here are by their nature unpredictable, as no one has a clue how this might all play out. But I can think of a few themes:

- Bond investors, who have seen the value of their mortgage-backed debt rise impressively over the past 18 months, could find themselves unable to find any kind of bid at all. The paper will still be cashflowing, but those cashflows will be surrounded by enormous uncertainty, and no one’s going to want to buy them except at extremely deep discounts until the mess is cleared up.

- Mortgage servicers will go from being assets to being liabilities, and banks which own mortgage servicers could find themselves on the hook for substantial losses.

- The time from default to foreclosure will become indefinite, and as a result there will be a significant uptick in strategic defaults, especially in states with judicial foreclosures.

- The “shadow inventory” of houses which aren’t on the market but will eventually be sold once the bank gets around to foreclosing will grow substantially from its already-enormous level.

All of this is going to be very costly and very unpleasant for all concerned; the only winners I see here are the lawyers. Add in possible securities-fraud charges against investment banks which underwrote a lot of these bonds, and the end result is a level of legal chaos I can barely imagine, in both the civil and criminal courts. And I see no easy way out at all.

--------------------------------------------------------------

Wait there is more!!!!

From CNBC: Bank foreclosure cover seen in bill at Obama's desk...

"A bill that homeowners advocates warn will make it more difficult to challenge improper foreclosure attempts by big mortgage processors is awaiting President Barack Obama's signature after it quietly zoomed through the Senate last week. The bill, passed without public debate in a way that even surprised its main sponsor, Republican Representative Robert Aderholt, requires courts to accept as valid document notarizations made out of state, making it harder to challenge the authenticity of foreclosure and other legal documents."

That bill is H.R. 3808, the Interstate Recognition of Notarizations Act of 2010, and President Obama refused to sign it today. These comments were just published on the White House blog:

"As the President has made clear, consumer financial protections are incredibly important, and he has made this one of his top priorities, including signing into law the strongest consumer protections in history in the Wall Street Reform and Consumer Protection Act. That is why we need to think through the intended and unintended consequences of this bill on consumer protections, especially in light of the recent developments with mortgage processors."

President Obama didn't have a choice, he had to axe the bill, if he didn't, he would've been committing political suicide.

So were stuck in the mud and the saga continues with no end in sight...so much for the two month uptick in Pending Home Sales!

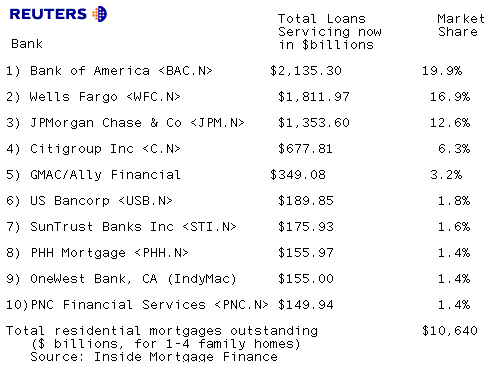

Here is a list of top lawsuit targets, ranked by loans in servicing.

Someone or somebody must put a stop to this mess or I might have to move to Canada...........