The Mortgage Bankers Association (MBA) today released its Weekly Mortgage Applications Survey for the week ending October 1, 2010.

The MBA's loan application survey covers over 50% of all U.S. residential mortgage loan applications taken by retail mortgage bankers, commercial banks, and thrifts. The data gives economists a snapshot view of consumer demand for mortgage loans.

In a low mortgage rate environment, a trend of increasing refinance applications implies consumers are seeking out a lower monthly payment. If consumers are able to reduce their monthly mortgage payment and increase disposable income through refinancing, it can be a positive for the economy as a whole (creates more consumer spending or allows debtors to pay down personal liabilities like credit cards). A falling trend of purchase applications indicates a decline in home buying demand, a negative for the housing industry and the economy as a whole.

Excerpts from the Release...

The Market Composite Index, a measure of mortgage loan application volume, decreased 0.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 0.3 percent compared with the previous week. The four week moving average for the seasonally adjusted Market Index is down 3.0 percent.

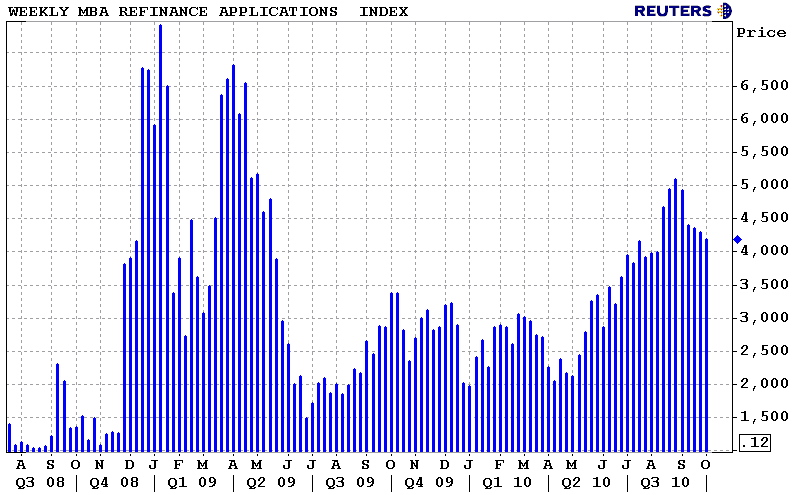

The Refinance Index decreased 2.5 percent from the previous week. The four week moving average is down 4.2 percent for the

Refinance Index. The refinance share of mortgage activity decreased to 78.9 percent of total applications from 80.7 percent the previous week.

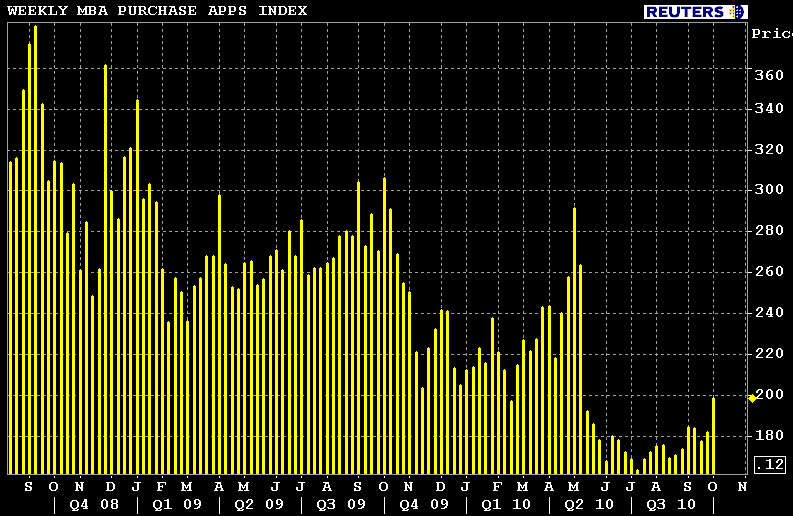

The seasonally adjusted Purchase Index increased 9.3 percent from one week earlier and is the highest Purchase Index observed in the survey since the week ending May 7, 2010. The unadjusted Purchase Index increased 9.1 percent compared with the previous week and was 34.7 percent lower than the same week one year ago. The four week moving average is up 2.0 percent for the seasonally

adjusted Purchase Index.

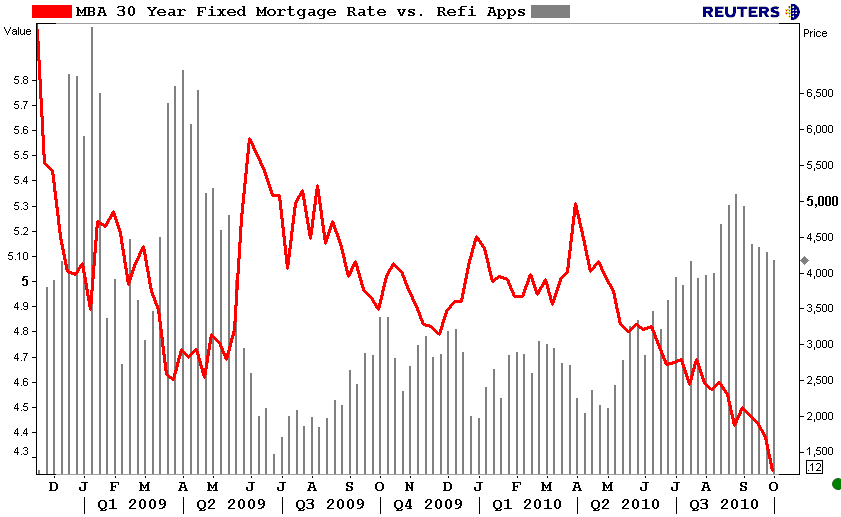

The average contract interest rate for 30-year fixed-rate mortgages decreased to 4.25 percent from 4.38 percent, with points decreasing to 1.00 from 1.01 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans. The 30-year contract rate is the lowest recorded in the survey, with the previous low being the rate observed last week. The effective rate also decreased from last week.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 3.73 percent from 3.77 percent, with points increasing to 1.14 from 1.13 (including the origination fee) for 80 percent LTV loans. The 15-year contract rate is the lowest recorded in the survey, while the previous low was observed last week. The effective rate also decreased from last week.

The average contract interest rate for one-year ARMs increased to 7.11 percent from 7.04 percent, with points increasing to 0.24 from 0.22 (including the origination fee) for 80 percent LTV loans.

The adjustable-rate mortgage (ARM) share of activity increased to 6.1

percent from 6.0 percent of total applications from the previous week.

THE MBA SAYS:

“The increase in purchase activity was led by a 17.2 percent increase in FHA applications, while conventional purchase applications also increased by 3.6 percent,” said Jay Brinkmann, MBA’s Chief Economist. “This is the second straight weekly increase in purchase applications and the highest Purchase Index level since the expiration of the homebuyer tax credit program. One possible driver of last week’s big increase in FHA applications was a desire by borrowers to get applications in before new FHA requirements took effect October 4th, which included somewhat higher credit score and down payment requirements.”

Jay hits the nail on the head. While new upfront MIP requirements lower the cost for borrowers at the closing table, the plain and simple truth is the increase in the annual premium (paid monthly) pushes monthly costs higher for homeowners. Hence the uptick in purchase demand, led by FHA loans, before the October 4 case number deadline .

HUD has decided to raise the annual premium and correspondingly lower the upfront premium, except for Home Equity Conversion Mortgages (HECM), so that FHA is in a better position to address the increased demands of the marketplace and return the Mutual Mortgage Insurance (MMI) fund to congressionally mandated levels without disruption to the housing market.

Based on the new authority, effective for FHA loans for which the case number is assigned on or after October 4, 2010, FHA will lower its upfront mortgage insurance premium (except for HECMs) simultaneously with an increase to the annual premium which is collected on a monthly basis. This policy change will decrease upfront premiums for purchase money and refinance transactions, including FHA-to-FHA credit-qualifying and non-credit qualifying streamlined refinance transactions.

Besides updated Mortgage Insurance Premiums, FHA also changed the following regs, as of October 4. Most of these were already covered by lender overlays though....

- Borrowers with a minimum decision credit score at or above 580 are eligible for maximum financing.

- Borrowers with a minimum decision credit score between 500 and 579 are limited to 90 percent LTV.

- Borrowers with a minimum decision credit score of less than 500 are not eligible for FHA-insured mortgage financing.

- Borrowers with a non-traditional credit history or insufficient credit are eligible for maximum financing but must meet the underwriting guidance in HUD 4155.1 4.C.3.

I CAN'T WAIT TO SEE HOW POTENTIAL HOME PURCHASERS REACT WHEN/IF THE FHA ACTUALLY DECIDES TO REDUCE SELLER CONCESSIONS FROM 6%TO 3%....

You read that right. IF/THEN was intended to imply the decision wasn't final. The FHA got a ton of negative feedback when they issued their request for comment back in July and I am now hearing the FHA is happy to keep pushing this reg change back, if they change it at all. If that reg were to go live though, we would see a big 'ol rush in purchase demand before the case number assignment deadline.

If you're looking to expand your knowledge base on the topic, the FHA provides a ton of background about updated risk management practices in their Federal Register Notice: "Federal Housing Administration Risk Management Initiatives: Reduction of Seller Concessions”