Is it time to bid farewell to an American-as-Apple-Pie tax deduction?

Maybe.

After 75 years of supporting it against all assaults, the National Association of Home Builders (NAHB) has abandoned its defense of the mortgage interest deduction (MID) one of the more sacred cows in the U.S. tax code. The National Association of Realtors (NAR) however is standing tough.

The rift between the two influential lobbying groups comes even as the existence of the MID does not seem at risk in what little is known about the expansively promoted but thinly explained Trump administration and Republican congressional "tax reform" plans.

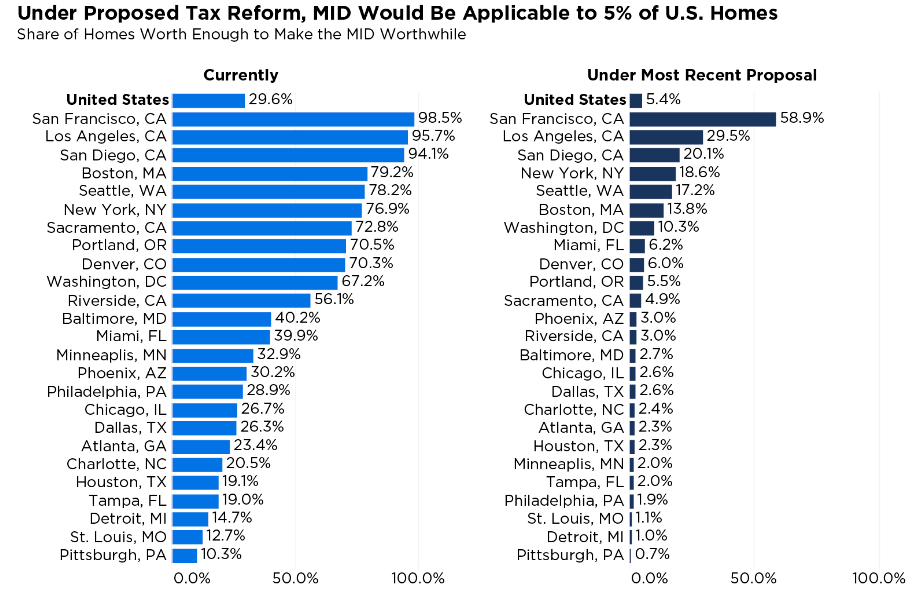

Under the current version, the MID would not go away, but its utility would be considerably reduced. The standard deduction would double and other deductions, such as those for state and local taxes including real estate (property) taxes, would no longer be available. These changes would lessen the benefits of itemizing deductions for many, but certainly not all, taxpayers. At present, estimates of the number of homeowners who employ the MID in their tax returns range from 22 percent (Internal Revenue Service) to 29 percent (Zillow.)

According to Zillow, under present IRS rules, a homebuyer needs to purchase a property for at least $305,000 to make the deduction worthwhile. If the standard deduction is doubled and the property tax deduction eliminated, that home price would rise to $801,000 or more. Use of the MID would fall from the Zillow estimate of a 29 percent to 5 percent.

Zillow looked at some major metropolitan areas and estimated the minimum home price necessary for the aggregate of MID and state and local property taxes to exceed the standard deduction, both now and under the proposed changes, and how many homeowners could benefit under each set of rules.

The split between NAHB and NAR over the proposed changes comes down of course to the constituency of each. NAHB is more vested in protecting the low-income tax credit, which the proposed changes would not affect. Its chairman, Granger MacDonald said in part, "By lowering the pass-through rate, the plan will reduce the tax bill of thousands of small businesses and help to spur job and economic growth. More importantly, the blueprint maintains the Low-Income Housing Tax Credit, the most indispensable tool to help produce affordable rental housing. The plan also retains a business interest deduction for small businesses, which would ensure that our future tax code is truly pro-growth."

Granger goes on to acknowledge the tradeoffs and that the effectiveness of the MID "could be diminished as more families elect to take a higher standard deduction." He pledged the involvement of NAHB to help mitigate any detrimental effects the changes could have on the housing market."

In an interview with Politico, another NAHB executive, CEO Jerry Howard, raised the prospect of a mortgage tax credit, a benefit that wouldn't require taxpayers to itemize.

For its part, NAR is standing behind the deduction, and has started running ads defending it. Those ads claim the proposed changes could drive home prices down as much as 10 percent while raising taxes for most middle-income homeowners.

William E. Brown, current NAR president, calls the proposed changes "a backdoor elimination of the mortgage interest deduction for all but the top 5 percent who would still itemize their deductions." NAR, he said "believes the result would all but nullify the incentive to purchase a home for most, amounting to a de facto tax increase on homeowners, putting home values across the country at risk and ensuring that only the top 5 percent of Americans have the opportunity to benefit from the mortgage interest deduction."

"We have always said that tax reform - a worthy endeavor - should first do no harm to homeowners," he added. "This tax framework misses that goal."

The Politico piece referenced above, written by Lorraine Woellert, calls the rift a first for the industry. She says those involved in the homebuying pipeline "typically lock arms to defend the mortgage-interest tax deduction as a building block to homeownership and wealth creation." She noted that, "Just months ago, Howard was aligned with NAR, calling the tax plan an "assault." She said other provisions, including lower tax rates on his homebuilder members and the promise of faster economic growth, have swayed him into thinking the framework a good one,

NAR Vice President Jamie Gregory told Woellert that his group was trying not to overreact to the NAHB defection, saying that association had merely thrown out a press release at the beginning of a very long process. "They're making a strategic play here to be on the positive side of the table, whereas I think we're going to make a strategic decision that it's time to start speaking out."