Increasing home prices are at the heart of a decision by the major federal regulatory agencies to raise the threshold for requiring a residential real estate appraisal for mortgages originated by their regulated institutions. When the rule become effective, mortgages on 1 to 4 family homes sold for $400,000 or less may be exempt from an appraisal; the current level is $250,000. It will be the first change in the threshold in a quarter century.

The new rule, declared by the Federal Deposit Insurance Corporation (FDIC), Office of Comptroller of the Currency (OCC), and the Federal Reserve (Fed), has been published in final form but apparently has not yet received the requisite signatures from the Fed. The agencies say the Consumer Financial Protection Bureau was involved in developing the proposal and agreed that it offers reasonable protection for consumers. The proposal will become effective the day following its publication in the Federal Register which could be as early as this week

The change applies to mortgages governed by Title XI of the Financial Institutions Reform, Recovery, and Enforcement Act (FIRREA) of 1989 and does not affect mortgages originated for sale to or guaranteed by FHA, VA, or the GSEs Fannie Mae and Freddie Mac. Even though the change applies to only those institutions regulated by FDIC, OCC, and the Fed it will still raise the number of mortgage originations for which appraisals are not required by about 40 percent. Agencies may still require real estate evaluations in their own regulations.

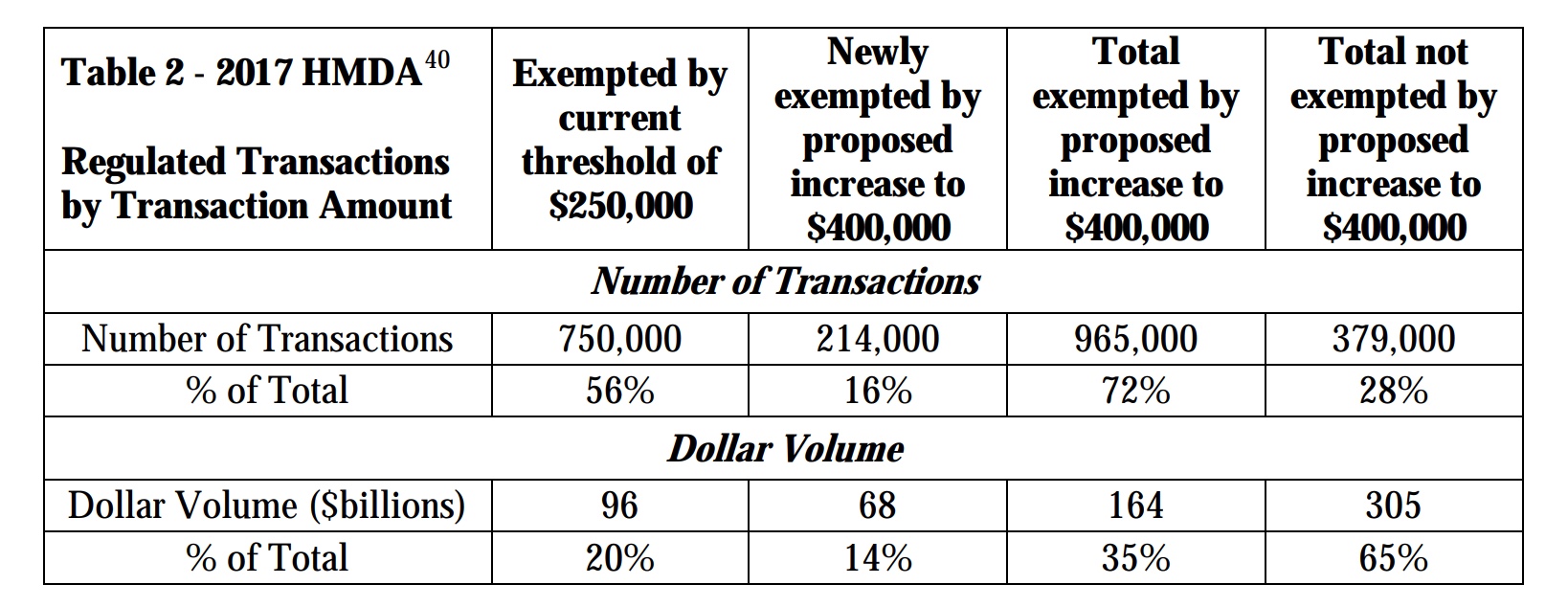

The FDIC estimates that, had the $400,000 threshold been in effect in 2017 it would have increased the number of loans exempted from the appraisal requirement from 750,000 to 991,000, an increase of 214,000 loans. In percentage terms, rather than 56 percent of Title XI mortgages that do not require an appraisal under the current rule, there will be 72 percent with the new threshold. It would also raise the share of all Home Mortgage Disclosure Act (HMDA) covered originations exempted from appraisals by 3 percent.

The new threshold was established after a review of home price increases since the $250,000 level was established in 1994. The agencies analyzed the Standard & Poor's Case-Shiller Home Price Index (Case-Shiller Index) and the Federal Housing Finance Agency (FHFA) Housing Price Index (HPI) to determine changes in house prices since then. The agencies also analyzed general measures of inflation by reviewing the Consumer Price Index (CPI).

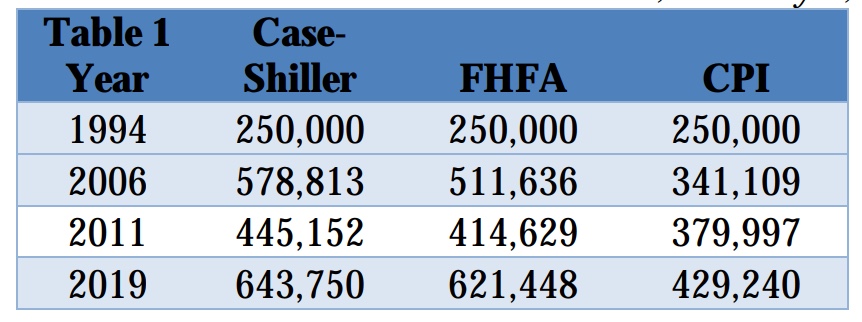

A residential property that sold for $250,000 in June 1994 would be expected to have sold in March of this year for $643,750 according to the Case-Shiller Index and $621,448 according to the FHFA Index. The agencies also considered housing prices over the most recent financial cycle which were generally at a low point in 2011. During the low point of the cycle, in December 2011, a house that sold for $250,000 in 1994 would have been expected to sell for $445,152 in December 2011, according to the Case-Shiller Index and $414,629 according to FHFA's HPI.

The agencies adopted a conservative approach and proposed a threshold of $400,000 to approximate housing prices based on the low point during the most recent cycle. The proposed threshold level is also consistent with general measures of inflation across the economy reflected in the CPI since 1994.

The three agencies first proposed the threshold change last November, publishing it and requesting public comment. They received over 560 comments. Those from financial institutions, their trade associations and state banking regulators generally supported the change while comments from appraisers, appraiser trade organizations, individuals, and consumer advocate groups generally commented in opposition to increasing the threshold.

Favorable comments asserted that an increase would be appropriate given the gains in real estate values over the last 25 years as well as the cost and time savings to lenders and borrowers that the higher threshold would provide. Other commenters said that evaluations were appropriate substitutes for appraisals and that the change would benefit consumers by reducing costs and delays due to appraisals.

The opposition asserted the proposal would elevate risks to borrowers, the financial system and individual institutions and system and taxpayers. The comments also called appraisals a necessary function in real estate lending and expressed concerns that bypassing them could lead to fraud and another real estate crisis. Many commenters said that the increased risk would not be justified by burden relief resulting from a threshold increase.