Fannie Mae said it is maintaining its forecast for 2016's GDP at the same 1.8 percent it forecasted in July despite the fact second quarter growth came in a 1.2 percent, more than 1.0 point lower than the company's forecast last month. The company's Economic and Housing Outlook report for August calls reports of most of the components of the GDP in the second quarter "disappointing." The exception was strong real consumer spending.

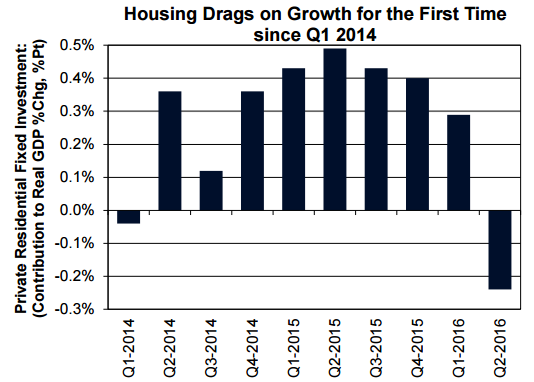

Residential, non-residential, government, and inventory investment spending all slowed growth, Residential investment fell due largely to weakness in single-family home building which subtracted 0.2 percentage points from growth. This was the first time housing has subtracted from growth since the first quarter of 2014.

The average annualized rate of growth in the first half of the year came in at what the company's economists, headed by Senior Economist Doug Duncan, call an "underwhelming" 1.0 percent, however the team did not revise its projection for growth for the year down from their earlier one of 1.8 percent. They expect that the surprise drawdown of inventory in the second quarter will probably reverse and that growth in the second half will rebound to a rate about 0.5 percentage points greater than anticipated earlier, leaving the final year's number unchanged from earlier estimates.

Any concerns over some of the weak indictors were mitigated by the strong July jobs report which, coupled with revisions to the two previous reports, puts the average monthly job growth over the three-month period at 190,000 compared to the trend of only 118,000 in May. The jobs report also indicates improving income prospects with annual average increases in hourly earnings at a seven-year high of 2.6 percent and an increase in the index of aggregate hours, which reflects increases in both hours worked and the number of payrolls, up 0.5 percent for the month, the largest gain in a year.

The jobs report also gives ammunition to those members of the Federal Open Market Committee who wish to hike rates in September. Most members however appear to wish to proceed more cautiously and inflation figures tend to support them. The Personal Consumption Expenditures (PCE) price index is still running below the Fed's 2.0 percent target. Fannie Mae believes the Global uncertainties and anemic output growth also suggest the committee will not make a rate move at its next meeting.

While some of the impacts of Brexit have eased, the downward pressure on long-term Treasury yields has not. The Bank of England cut its key policy rate, expanded its quantitative easing program and moved to provide £100 billion of additional funding to banks to help ease the strain of lower short-term rates. With a continued search on the part of investors for positive yields, those for the long-term Treasury notes should remain low. There is a concern that a rise in the fed rate while other central banks are easing their monetary policy could cause the dollar to appreciate significantly which could slow growth and delay inflation from hitting that Fed target. Fannie Mae has not changed its prediction that the Fed will hold rates steady this year.

Like Freddie Mac's August forecast issued earlier this week Fannie Mae's sees mortgage rates staying at near record lows for the rest of the year, averaging just 3.4 percent during the fourth quarter, down a bit from its July forecast. This should support the housing market through the year coupled with gradually loosening of lending standards such as reported by was lenders in the Fed's second quarter Senior Loan Officer Opinion Survey.

Sales of both new and existing homes performed better during the first six months of the year, with new sales up 11 percent and existing homes rising 5.0 percent from the first half of 2015. Leading indicators however do signal a near-term slowdown; pending sales were flat in June and purchase mortgage applications were also unremarkable in June and July

While home sales rose quarter-over-quarter single family starts were down for the first time since the first quarter of 2015. It is expected that demand for homes will be strengthened by solid job and wage growth but weak single family home building and soft construction hiring are worrisome for the supply side. Without some relief from new construction, home inventories will remain tight and put upward pressure on prices especially at the lower end of the market.

Given the strong home sales and the weak homebuilding activity in the second quarter Fannie Mae revised its forecast for both home sales for the rest of the year and single family starts for the next four quarters. It now projects 2016 sales to be 4.0 percent higher than last year at 6.22 million and housing starts to be at an annual rate of 936,000 by the third quarter of 2017 compared to a projection of 785,000 for this current quarter.

Mortgage originations are expected to rise from 2015 by 3.0 percent to 1.76 trillion next year, with an increase in purchase originations more than offsetting a decline in refinancing. The refinancing share will drop 4.0 percentage points to 42 percent.

Household growth continues to recover from the severe downturn it took with the recession and as a result the rental vacancy rate is at its lowest level in decades. Still, homeownership continues to decline and fell to 62.9 percent in Q2, its lowest level in the second quarter since the Census Bureau began tracking it in 1965. However, there are finally some indications that older Millennials are becoming homeowners.