Like all large financial institutions, the government sponsored enterprises (GSEs) Fannie Mae and Freddie Mac are required by the Dodd-Frank Act to submit to periodic stress tests. These tests, known as DFASTs, are designed to determine whether companies have the capital necessary to absorb losses when they encounter adverse economic conditions. The GSEs are subject to the tests because they meet the criteria of being regulated by a primary federal financial regulator, in this case the Federal Housing Finance Agency (FHFA) and have consolidated assets exceeding more than $10 million. FHFA has just released results of the fourth implementation of DFASTs for the GSEs.

The Severely Adverse scenario was identical for both GSEs. It sets forth a situation where there is a severe global recession accompanied by elevated stress in both corporate financial and commercial real estate markets. Asset prices are significantly reduced, there is significant widening of corporate bond spreads, and liquidity conditions are strained. The planning horizon for the implementation of the DFAST is nine quarters, beginning January 1, 2016 and ending March 31, 2019.

The scenario portrays a real GDP decline that begins immediately in 2017 and reaches a trough, after a decline of 6.50 percent from the pre-recession peak, in the second quarter of 2018. The unemployment rate increases from 4.7 percent to a peak of 10.0 percent in the third quarter of 2018, and annualized consumer price index inflation declines to 1.26 percent by the second quarter of 2017 then rises to 1.75 percent by the middle of 2018.

This decline in economic activity leads to a near zero short term treasury note rate virtually throughout the planning horizon while the 10-year Treasury rate drops to about 0.75 percent almost immediately then gradually rises to about 1.50 percent in early 2019. Asset prices decline sharply and credit losses mount. Spreads on investment-grade corporate bonds versus long term Treasury notes increase to 5.5 percent in the first year of the test and equity prices fall by about 50 percent. Equity volatility increases to near the levels seen in 2008. Home prices decline by about 25 percent and commercial real estate prices by 35 percent through the first quarter of 2019.

The GSEs' retained portfolios are affected, with large and immediate changes in asset prices, interest rates and spreads. Option-adjusted spreads on mortgage-backed securities widen significantly. In addition, the scenario assumes failure of each of the GSEs' largest counterparty. There is an instantaneous loss and reduction of capital in the first quarter and no recovery by the GSEs in future quarters. FHFA directed them to report the greater of either the global market shock losses or the losses attributable to the macroeconomic scenario for the identical positions.

FHFA provided the GSEs a year of scenario assumptions beyond the nine-quarter planning horizon for their use as needed and historical data on scenario variables. The GSEs were told to comply with the terms of their amended Senior Preferred Stock Purchase Agreement. (PSPAs) to determine the level of dividends to be paid to Treasury over the planning horizon.

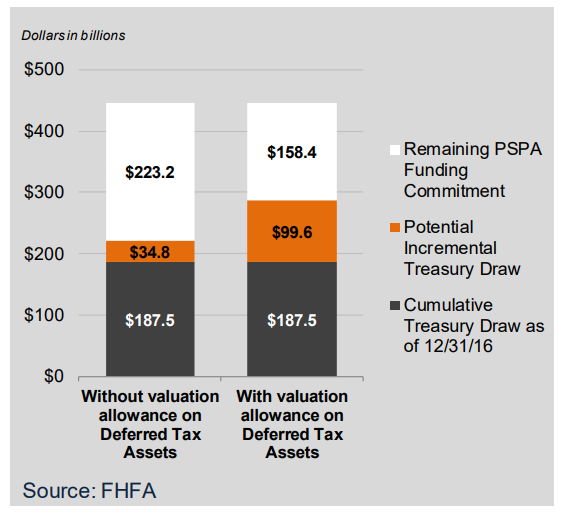

The results were given for the GSEs both as separate entities and cumulative. Each report was presented as "Results without establishing valuation allowance (VA) on deferred tax assets", the impact of establishing such allowances, and the result of doing so. The most important figures for the combined GSE results with the VA established were as follows.

- As of December 31, 2016, the GSEs had drawn a combined $187.5B from the Treasury under the terms of the PSPAs, and the combined remaining funding commitment was $258.1B at the end of 2016.

- Pre-provision net revenue was $33.3B and provision for credit losses ($55.9B)

- Mark-to-market losses were ($5.8B)

- There would be a global market impact on trading securities and counterparty, including held-for-sale loans of ($8.2B)

- Provision for taxes would be ($51B) after the impact of ($64.4B) from establishing the VA.

- Total comprehensive loss would be ($99.5B), again after the ($64.4B) VA.

- There would be no dividends paid by Fannie Mae over the nine-quarter period. Freddie Mac projected total dividends of $1.3B after the VA. The two GSEs would require draws of $99.6B over the planning horizon, 57.0B from Fannie (post the $42.7B allowance) and $42.6B for Freddie Mac (after the $22.1 allowance.) This would leave a remaining funding commitment of $60.6 billion and $97.8B respectively.

- Credit losses (charge-offs, net plus foreclosed property expenses) would total $7.3B, .36 percent of the combined portfolios.

FHFA stresses that the DFAST results are not expected outcomes but model projections to "what if" exercises. They do not define the full range of possible outcomes which might be different. Also, while there is a degree of comparability between the GSEs, it does not eliminate differences in their respective accounting, internal models, or management.