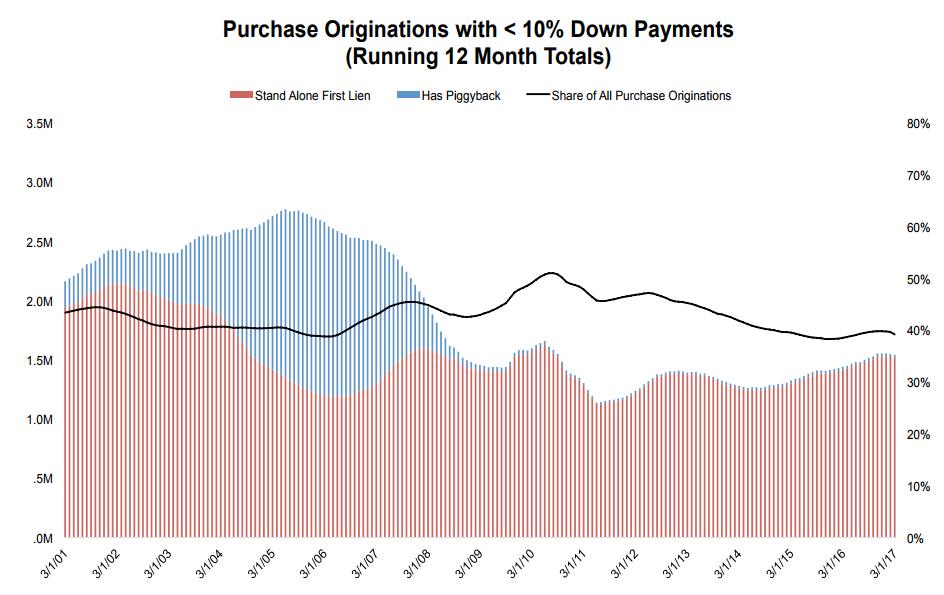

Fannie Mae and Freddie Mac's (the GSE's) low downpayment loans are apparently beginning to cause some pain for FHA lending. Black Knight's Mortgage Monitor report, its monthly summary of mortgage performance data, notes that low-down-payment originations, which they define as loans with downpayments below 10 percent, currently account for nearly 40 percent of all purchase originations and 1.5 million borrowers have closed on such loans in the last 12 months, a seven-year high.

Low down-payment loans have historically been the purview of FHA and VA. FHA will loan 97 percent of the purchase price with mortgage insurance, while VA will guarantee up to a loan-to-value (LTV) ratio of 100 percent for an eligible borrower. The GSE's announced reintroduced a program in late 2014 that would allow as little as 3 percent down, but borrowers must also carry private mortgage insurance.

Black Knight says the increase in low-downpayment loans is primarily a function of the overall growth in purchase loan originations, but such loans declined as a percentage of originations for four straight years. They have now seen their share increase for the last 18 months.

High LTV ratios during the housing boom were more a function of the piggyback second mortgages that boomed during that era rather than low-downpayment first mortgages. Then the low-downpayment share rose through 2010 as FHA lending increased to a 50 percent share, taking up the slack in funding after private money disappeared. As FHA lending returned to more normal levels, the share of low-downpayment lending declined.

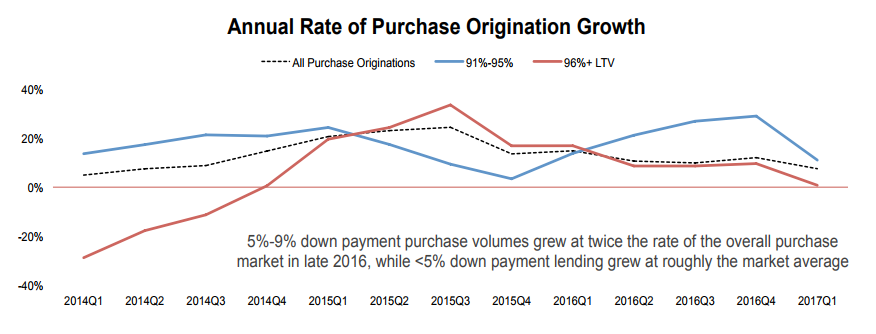

Black Knight says the FHA/VA share has declined as the GSEs have expanded their low-downpayment lending. While very low down-payment lending is growing at about the market average, loans with 5 to 9 percent down have been growing at twice the rate of the purchase mortgage market.

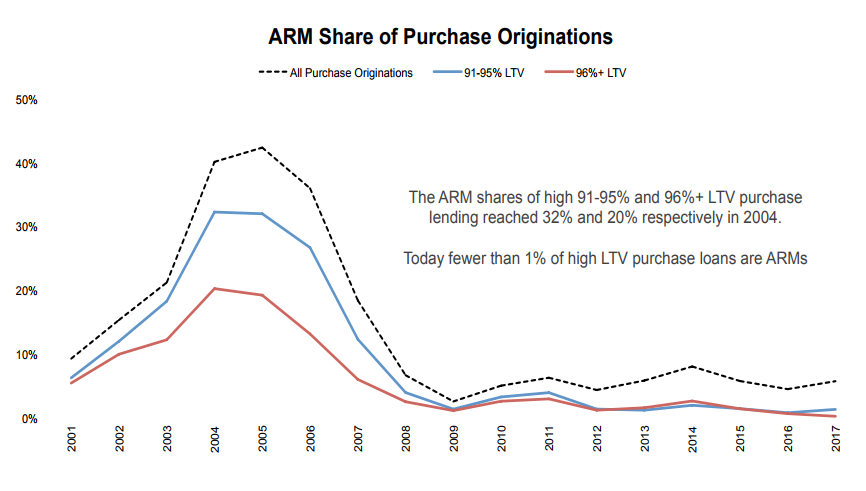

The Monitor points out that today's high LTV loans are quite different from a risk perspective than those originated before the housing crisis. For example, in 2004 nearly a third of 91 to 95 percent LTV loans were adjustable rate mortgages (ARMs) and that share remained elevated through 2007. In 2004 ARMs accounted for one in five of the very high LTV (over 96 percent) loans.

Today, ARMs themselves are rare. The Mortgage Bankers Association consistently reports they make up less than 7 percent of loan applications, and are virtually non-existent in the high LTV purchase space.

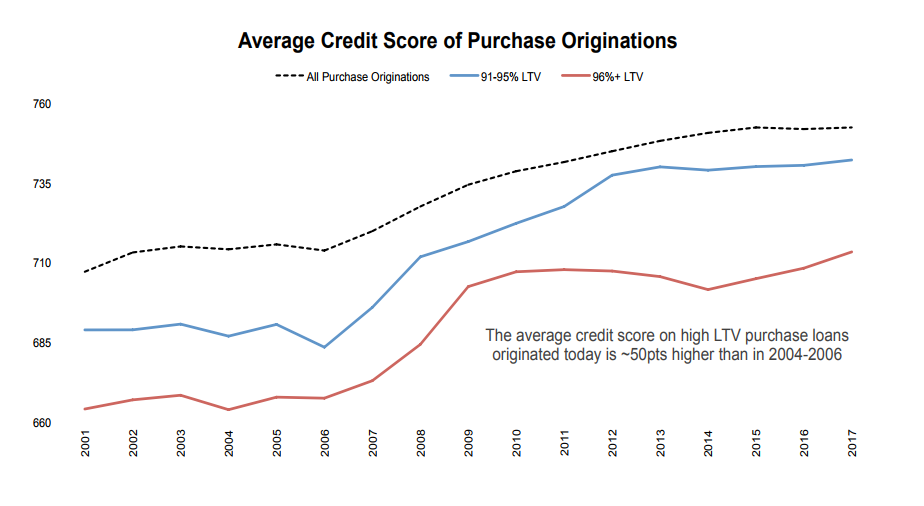

Another difference in risk factors is the high degree of credit-worthiness of the borrowers. The average credit score of those taking these loans, even though many are first-time buyers, is about 50 points higher than those approved for such loans from 2004 to 2007.

Despite the GSEs' reintroduction of the 3 percent down mortgage, FHA and VA still have the lion's share of the over 95 percent LTV market. Still, the GSEs share has grown to 10 percent, the highest level since early 2008. Again, these are credit-worthy borrowers. The average FICO score is now just under 715, up 7 points over the last year and nearly 60 points higher than in the GSEs' pre-recession originations.

The GSEs also have about three-quarters of 5 to 9 percent downpayment loans while FHA has dropped to 16 percent. Overall, less than 60 percent of GSE purchase loans involve a 20 percent or higher downpayment, the lowest share since 2000.

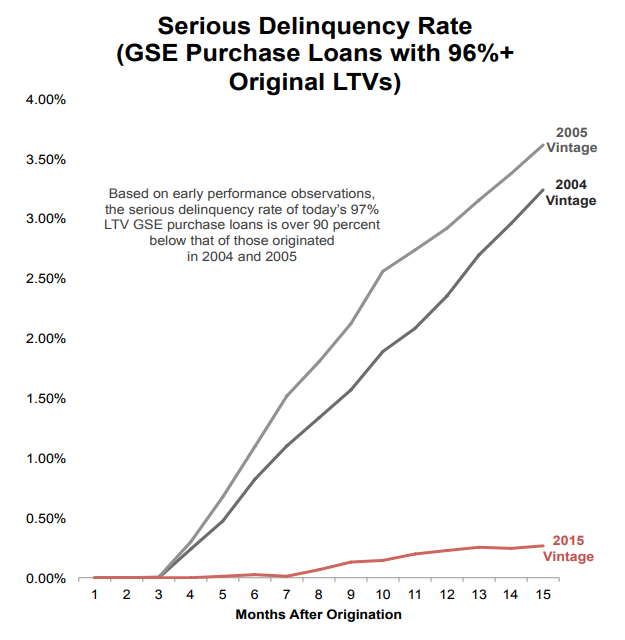

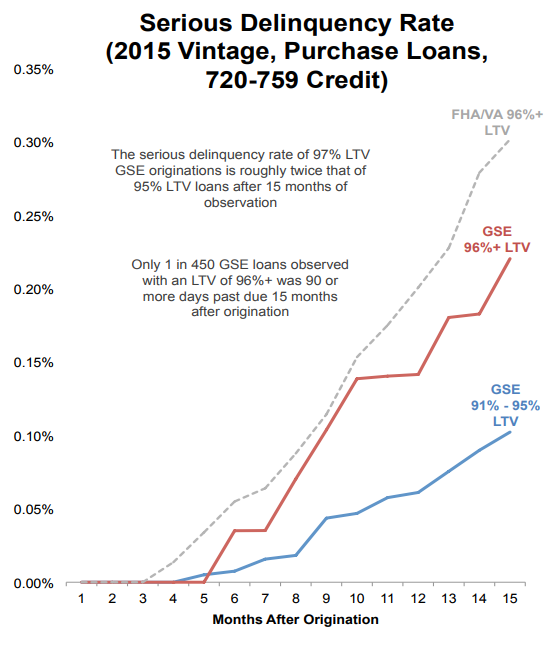

As Black Knight Data & Analytics Executive Vice President Ben Graboske explained, in general, low-down-payment purchases are on the rise, but this does not necessarily mean a return to the practices - and risks - of the past. Overall, defaults among current high-LTV mortgages remain low and performance has been much better than among similar loans in 2005-2006, he says, likely due to the improved borrower risk profile referenced above. After 15 months of observation, the serious delinquency rate of 97 percent LTV GSE originations is markedly higher than that of 95 percent LTV loans. However, in looking at the 2015 vintage, only one in approximately 450 GSE loans with an LTV of 96 percent or higher observed within the study was 90 or more days past due 15 months after origination. Based on early performance observations, today's 96+ percent LTV GSE purchase loans have a serious delinquency rate over 90 percent below that of those originated in 2004 and 2005.

GSE mortgages with less than 5 percent down typically have FICO scores 10 points lower than those with 5 to 9 percent down. However, even looking within credit score buckets, there is a noticeably higher early delinquency rate in the under-5 percent group than with the 5 to 9 percent loans. This is not unexpected, Black Knight says, as the higher LTV loans are specifically geared toward first-time homebuyers and may carry income restrictions in some cases. Still, these loans have lower default rates than FHA loans with similar LTVs

And speaking of delinquencies, the Monitor also expanded on some of the information about loan performance covered in its First Look for June.

There were 266,000 mortgage defaults in the second quarter of 2017, one out of every 573 mortgages each month, the lowest rate since 2005. Over 60 percent of new defaults are coming from the pre-2009 vintage of loan originations; these loans continue to default at more than 2.5 times the national average. The 2014 vintage is also showing higher than average default rates than other post-recession vintages which Black Knight attributes to an above average share of both purchase originations and the ARMs than other years because of higher interest rates.

The rate of improvement in defaults is declining as the market normalizes. The rate of reduction has declined from 11 percent in June 2016 to 1 percent this June. Private label security (PLS) loans however continue to default at three times the market average even though the majority of them have seen 10 years of seasoning.

Foreclosure starts have also reached recent lows. There have been 354,000 foreclosures initiated thus far in 2017, the lowest rate since 2001. Forty-five percent (158,000) were first time starts, as opposed to loans that are re-defaulting, the lowest volume in Black Knight's records and 40 percent below long-term, pre-crisis norms.

The foreclosure inventory, loans in process of foreclosure, still is 44 percent higher than normal levels. The inventory now stands at 410,000 properties, but as Black Knight notes, there are approximately 170,000 active foreclosures that are over two years delinquent and 85,000 haven't had a payment in more than five years. This aged inventory accounts for 40 percent of active foreclosures. When those are taken out of the equation, early stage foreclosures are 25,000 below historic norms. The inventory has marked 29 consecutive monthly declines and has seen only one monthly increase in the last five years.

Completed foreclosures are also down, there were 132,400 in the first six months of the year, a 23 percent decline from the same period in 2016, and the lowest volume for the first half of any year since 2005. At the current rate of improvement, the foreclosure sale rate will be below pre-crisis levels by next summer, and will hit the lowest level this century by mid-2019.

However, even when foreclosure volumes normalize there will still be of 70,000 excess aged foreclosures and it will be those that will keep foreclosure volumes near historic norms. Black Knight estimates it will take another three years for the backlog to normalize on a national basis.