Most of the major proposals for reforming the housing finance system rely on two steps to minimize the risk that any one or two institutions, and in today's environment that would mean the GSEs Fannie Mae and Freddie Mac, can pose to the mortgage market. Current proposals require that any institution that issues mortgage-backed securities guaranteed by the government share most of the related credit risk with others in the private market, and that there be a government or government-like utility to manage the infrastructure used in issuing these securities.

In a research paper written for the Urban Institute's Housing Finance Policy Center, Jim Parrott, a non-resident fellow at the Urban Institute (UI) and owner of Falling Creek Advisors, says that the GSE's and their conservator/regulator the Federal Housing Finance Agency (FHFA) have already made significant progress on both fronts. They have developed a process by which both GSEs are sharing increasing amounts of risk, and as a joint venture, have begun to build a platform to take over the securitization functions they currently manage. Parrott says the risk sharing has received a lot of attention, but little has been said about building the platform.

Putting the management of the securitization process in the hands of two privately owned institutions has been problematic for several reasons, the author says, but two stand out. The first is that having a duopoly in control of such a critical component of the secondary market constrains competition. The GSEs have dominated the guarantee market and have been able to set the terms for a wide range of markets that depend on infrastructure they control. Any duopoly will invariably set those terms in a way that benefits them and will usually present an uneven playing field to others. An example is the lower guarantee fees the pre-conservatorship GSEs provided to larger lenders.

A second problem with vesting such control in a privately-owned duopoly is the too-big-to-fail risk that it creates. That neither player can be allowed to fail creates an incentive for them to take excessive risk, exposing the broader financial system that depends on them to excessive risk as well. Parrott says putting the key secondary market infrastructure into a government or government-like utility, reduces both market distortions.

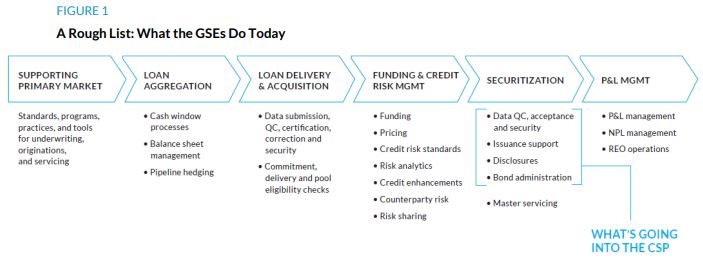

FHFA outlined plans for a common securitization platform in 2013 and since then the GSEs have established a joint venture called Common Securitization Solutions to design a Common Securitization Platform (CSP) to manage the data, issuance, settlement, bond administration, and disclosures associated with the single mortgage-backed security that will be issued by both Fannie Mae and Freddie Mac. When it is finished the GSEs will continue to maintain loan-level control of the loans they purchase and to set the terms for those loans. However, they will pass on to the CSP management of the mortgage-backed securities (MBS) that are issued on mortgage pools during the securitization process.

The CSP will collect and verify data, manage the offering documentation, form and register the MBS and handle all relevant disclosures to investors. Post securitization, CSP will handle all ongoing data security and requests, manage the payment files and disclosures required for payments to be made to investors, and make ongoing disclosures to investors. And as loans in the underlying pools become delinquent, it will manage the related data and disclosures, including related changes to payment schedules.

CSP is designed to modernize the securitization infrastructure, lowering costs and increasing efficiency and make the system less reliant on the GSEs. But Parrott says, as long as the CSP is owned by and accessible only to Fannie and Freddie, it will fall short of its potential for reform. The benefits of the improved infrastructure will naturally serve to further entrench the dominance of the only two guarantors able to use it.

He suggests that the CSP should be converted to a government or government-like utility, open to use by other guarantors. An open platform would meaningfully reduce the barriers for entry by other guarantors who might want to compete with the GSEs but without needing to develop their own infrastructure to do so. This would help end the dominance of the duopoly and aid transition to a more competitive system.

Parrott offers three objectives for developing an efficient utility. The CSP would need to provide enough of the critical securitization infrastructure to continue functioning if any single guarantor fails, provide a platform that allows other guarantors to compete "forcefully" with the GSEs, and provide a level playing field for all who use it.

If functions are left with Freddie and Fannie that others cannot easily replicate, it leaves the system vulnerable if either should fail. Decisions regarding the functions to include in the CSP should consider which ones require such expertise or capital that new entrants are unlikely to be able to provide them and be competitive. "Those that others are unlikely to be able to provide should go into the platform. Those that others are likely to be able to provide should not," Parrott says.

Providing a level playing field is probably the most straightforward of the objectives. The platform shouldn't allow any participants to leverage their access to the secondary market to disadvantage other participants. Volume-based pricing, as one example, should not be permitted.

Parrot says we need to think through those the tasks in Figure 1 with the above objectives of determining which of Fannie and Freddie's functions should be moved to the CSP. He cites as one possible example, the addition of master servicing. Having CSP oversee the servicing of a pool of loans would standardize the norms of servicing generally, and remove a complex and costly function, as well as a barrier to entry, from the issuers' responsibilities.

Expanding the CSP to play the role of an effective market utility will not come easily. Parrott says, as a general rule, adding functions to the CSP would be less complex than adding institutions because the latter would mean syncing up the many processes that the institution will need to interact with the platform. How difficult it will be to open the CSP to new issuers will depend on how many need to be added. A few "would not be a heavy lift, particularly if they are newly formed and thus can develop the relevant processes with this interface in mind," he says, but adding hundreds would be a challenge, particularly if many are established institutions with their own processes in place.

Parrott says we might ask why the existing Ginnie Mae platform that securitizes FHA, USDA, and VA loan pools couldn't be used for the market utility. It already has widespread market adoption, with hundreds of issuers and a third of new MBS issued off the platform. There is a key difference however. The CSP is being built to support a business model with the goal of managing and distributing credit risk, while Ginnie Mae's purpose is to support issuers with little credit risk because their loans are government guaranteed. Thus, where the CSP is set up to collect information on credit risk, i.e. credit scores and debt levels, Ginnie has neither the need nor the capacity to provide this kind of support.

While Ginnie could develop the needed infrastructure, it would be a significant endeavor. Just to match what the CSP is already being developed to handle would require them to collect and process roughly 10 times the number of data fields that they currently collect. Still more infrastructure would be required to further reduce barriers to competition with the GSEs. This is considerably more challenging than simply drawing from an infrastructure that already exists in Fannie and Freddie, as the CSP is doing today. Further, an expansion of the Ginnie Mae platform would also require the use of the HUD procurement process and the rules and regulations of the Administrative Procedures Act.

Parrott concludes by noting that the work the GSEs and FHFA are doing on the new platform is vastly unappreciated, both for the meaningful impact it promises to have on today's system and the much greater one it will have on a reformed system if its course is adjusted with that role in mind.