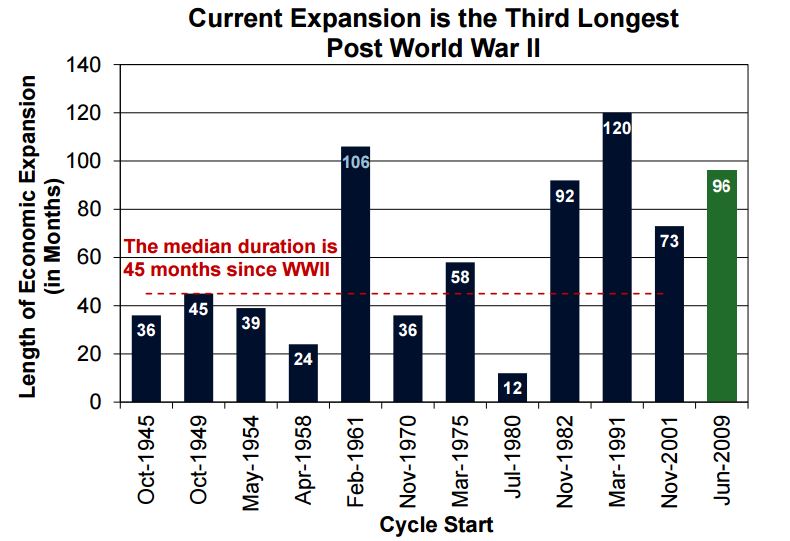

Fannie Mae's Economic and Strategic Research Team hedged a few bets in its June economic summary. It laid out some wild cards while predicting that the current expansion, which marks its eight-year anniversary this month and is the third longest of the post-World War II area, should continue its moderate growth next year.

One of those wild cards is the potential for fiscal stimulus. Fannie's team says the odds the Congress will enact major pieces of legislation, including health care, tax reforms, and infrastructure investment, by the end of this year have diminished, reducing the possibility of any meaningful impacts from fiscal stimulus before 2018. Another fiscal policy uncertainty this year is the need to raise the debt ceiling, probably in November, to avoid a government shutdown and a technical default. Tax revenue, according to the Congressional Budget Office, missed projections for the first eight months of Fiscal Year 2017 by as much as $70 billion, so the debt ceiling could be reached even earlier.

Meanwhile, the Fed continues to normalize monetary policy, raising the fed funds rate at its June Open Market Committee (FOMC) meeting by 25 basis points. In the Q&A session following her press conference, Chair Janet Yellen said balance sheet normalization could occur "relatively soon."

Following the FOMC meeting, long-term yields declined and the yield curve flattened further. The yield on 10-year Treasuries reached a three-year high of 2.63 percent on March 13, two days before the Fed raised the fed funds rate. The yield has trended down since then, reaching 2.13 percent on June 14. Mortgage rates have moved lower in tandem, with the average rate on 30-year fixed mortgages declining to below 4.0 percent during late May and early June. The spread between 10- and 2-year Treasury notes narrowed from a post-election high of 135.5 basis points in late December to below 80 basis points for the first time since early September.

The bottom line; Fannie Mae is holding to its prior forecast that economic growth will rebound to an annualized 2.9 percent in the second quarter, up from 1.2 percent in the first quarter. Real personal income and consumer spending both grew 0.2 percent in April.

They economists are also calling for one more Federal Reserve rate hike this year, even though the statement after the June Open Market Committee (FOMC) meeting in which the rate was raised 0.25 percent, said inflation has moderated from its earlier pace; the PCE is down to 1.7 percent and the Consumer Price Index slowed to 1.9 percent in May.

Turning to housing, the economic summary says the narrative has not changed over the past year. Labor shortages continue to constrain homebuilding and tight inventory to hold back sales and drive price increases. Year to date through April, single-family starts were up 7.0 percent, significantly greater than a 1.9 percent gain for multifamily starts. The latter's small gain reflects the maturity of multi-family housing's expansion which may have peaked last year. Single-family starts remain near levels witnessed in a typical recession prior to the last downturn.

The latest Job Openings and Labor Turnover Survey (JOLTS) confirms the lingering shortage of labor in the residential construction industry. In April, openings in the construction industry jumped to the highest reading since September, while the quits rate- a gauge of workers' confidence-remained at an expansion high for the third consecutive month.

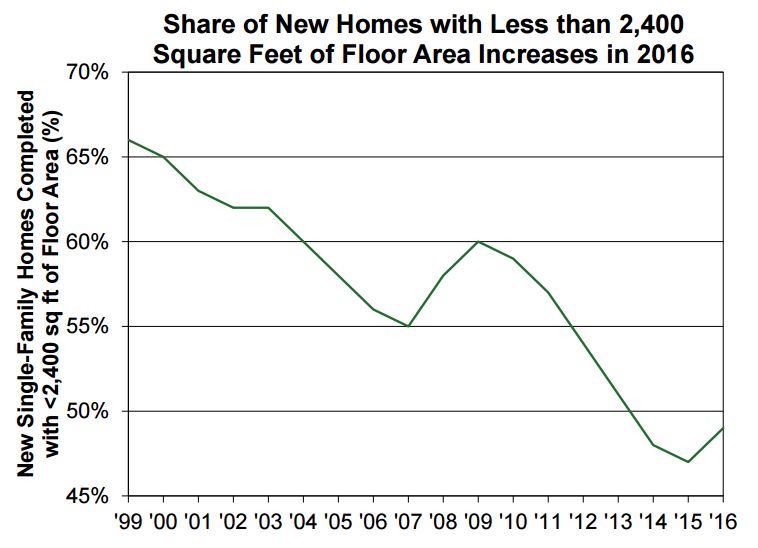

On a happier note, builders do appear to be responding to the demand for smaller new homes. The share of completed new single-family houses containing fewer than 2,400 square feet rose in 2016 for the first time in seven years. Fannie Mae says, if this trend continues, it could help alleviate the critically tight supply in the lower end of the market.

After hitting new post-crisis highs in March, both new and existing home sales pulled back in April. The report speculates that the unusually warm winter along with declining interest rates in January and February could have pulled some sales into the first quarter. The tight inventory of existing homes also contributes to decreased sales and the number of says on the market fell to a new record low. The months' supply of existing homes remained historically tight at 4.2 months, versus 4.6 months the previous April.

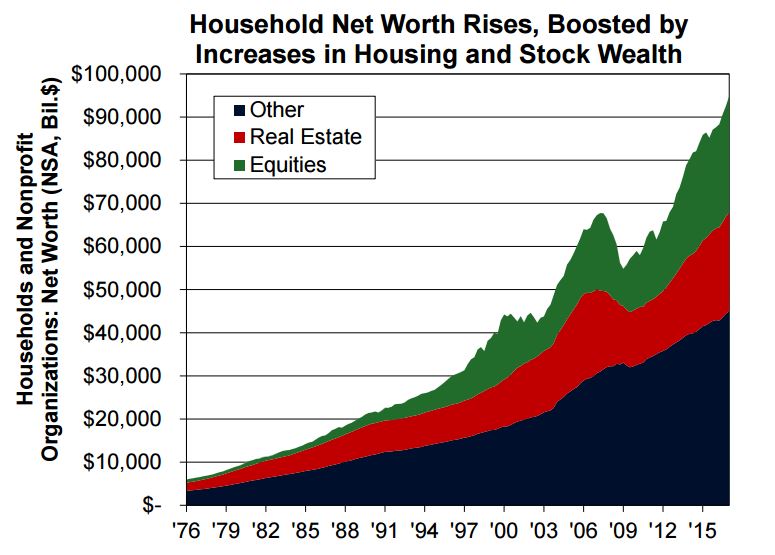

The lean inventory is a boon for homes prices and The CoreLogic House Price Index, the measure used by the Fed to estimate the value of real estate assets, gained 6.9 percent year-over-year in April-the strongest increase since May 2014. The continuing appreciation has continued to boost homeowners' equity which has now surpassed its previous peak recorded 11 years ago. Outstanding mortgage debt rose 1.9 percent on an annual basis, the weakest gain in a year.

This increase in household wealth must be balanced against the decreasing purchase affordability arising out of higher high prices. Fannie Mae's May National Housing Survey found the net share of respondents reporting it is a good time to buy a home dropped to a record low while the net share reporting it is a good time to sell surpassed the other measure for only the second time in the survey history dating back to 2011.

Fannie Mae calls the near-term outlook for existing home sales "bearish," although mortgage rates will remain supportive, staying near their current 4.0 percent levels. Total home sales will rise 3.2 percent this year and total single-family mortgage originations are projected to drop about 21 percent to $1.62 trillion, with a large drop in refinance originations outweighing a modest rise in those for purchases. The share of refinance originations is expected to fall from 48 percent in 2016 to 34 percent in 2017.