The continued high volume of refinancing kept mortgage lenders' outlook for profits relatively high during the second quarter, although it was down slightly from the first quarter of the year. Fannie Mae's Mortgage Lender Sentiment survey found that more than half (52 percent) of lenders who responded believed that their profit margins would be higher than the prior quarter, while the remainder were almost equally divided between those who expected lower profits or that they would remain unchanged. The survey of senior mortgage executives was conducted between May 5, 2020 and May 18, 2020.

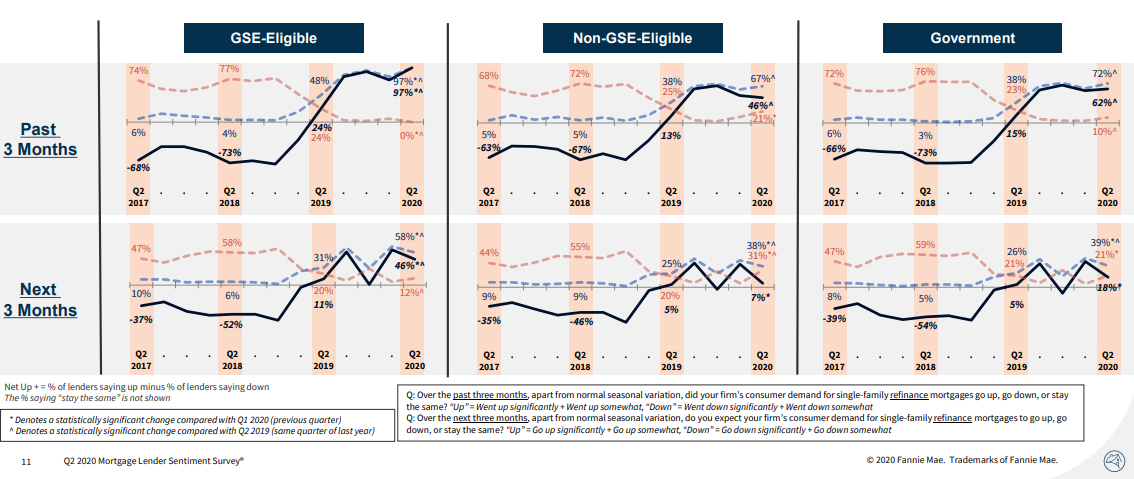

The lender optimism was based largely on the demand for refinancing, which outweighed a perceived decline in mortgage demand. The net share of lenders reporting demand growth for refis over the prior three months remained strong for all loans types (GSE-eligible, non-GSE-eligible, and government) and reached a survey high for GSE-eligible loans. Demand growth expectations on net for the next three months fell from last quarter but remained high across all loan types.

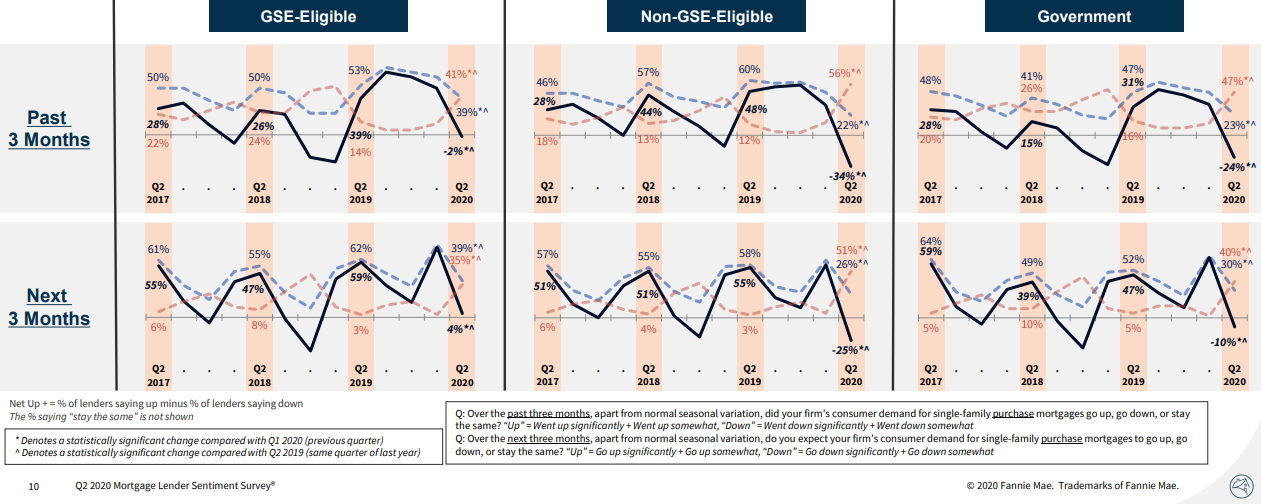

Purchase Demand

For purchase mortgages, the net share of lenders reporting demand growth for both the prior three months and the next three months fell significantly from last quarter across all loan types. For non-GSE-eligible mortgages, the net share reporting demand growth for both the prior three months and the next three months reached survey lows.

Refi Demand

The second most frequently cited reason lenders cited for the optimistic profit expectations was the pricing and policies of the GSEs Fannie Mae and Freddie Mac. Fannie Mae said mortgage spreads remain elevated; the average primary mortgage spreads (FRM 30 contract rate versus 10-year Treasury) came in at 256 basis points in May, above the long-run average of 168 basis points.

However, for the first time in the survey's history, more lenders responded that they believe the U.S. economy is on the wrong track, rather than on the right track. Also, after years of remaining largely unchanged, this quarter the majority of lenders reported tightening credit standards across all loan types.

"This quarter's results reflect the impact of COVID-19 on all fronts," said Fannie Mae Senior Vice President and Chief Economist Doug Duncan. "Lenders' reported purchase mortgage demand for the prior three months and expectations for the next three months declined significantly from last quarter across all loan types. Demand for non-GSE eligible loans showed a sharper drop, reaching the lowest reading since survey inception, indicating a shift toward the GSE-eligible lending market. Lenders attributed the purchase mortgage demand decline to COVID-19-related factors, including home price uncertainty, higher unemployment, policy changes, and lower inventory. Lenders pointed to the same reasons for credit tightening."

"There are, however, encouraging signs," continued Duncan. "For the agency lending market, the purchase demand outlook remains positive on net and is well above the Q4 2018 reading, a period of accelerated declines. If borrowers perceive the bottom of the economic downturn as having passed, there could be a pickup in purchase demand to take advantage of continued low mortgage rates. Additionally, this quarter, refinance demand expectations held relatively stable, demonstrating continued strength. Lenders' profitability outlook remains positive, likely because of stable refinance demand, lender capacity constraints, and still-wide mortgage spreads. Nevertheless, challenges remain as the uncertainty around COVID-19 persists, in particular for mortgage servicing."