Fannie Mae's economists used their May economic and strategic summary to downgrade expectations for 2015 growth but at the same time painted a slightly brighter picture for housing. Based on the poor growth of GDP in the first quarter, only 0.2 percent, they downgraded expectations for the year by 0.5 percentage point to 2.3 percent growth. The portion of the report dealing with housing was obviously written both before Tuesday's encouraging news about residential construction or Thursday's disappointing existing home sales report.

That said, Fannie Mae's economic team led by Senior Vice President and Chief Economist Doug Duncan called home sales for the quarter "mixed" with March existing home sales at their highest level in two years, preceding the "Taper Tantrum" over Fed Chair Ben Bernanke's comments about the Federal Reserve tapering bond purchases that choked off recovering sales. Even though March sales were up, the first quarter fell short of fourth quarter 2014 numbers. New home sales retreated in March but the first quarter overall was the best for that sector since 2008 and pending home sales and purchase mortgage applications both portend a strong spring buying season.

The soft spot singled out in the report is single-family homebuilding which contracted sharply in February and rebounded only slightly in March (but was up significantly in April with starts jumping more than 20 percent and permits up by nearly 11 percent). After nearly six years of recovery Fannie Mae says spending on private single-family construction remains stuck near 1998 levels. Poor performance for homebuilding and existing home sales led to a relatively flat contribution of residential investment to GDP in the first quarter. However, builder confidence picked up in April and new home inventories are tight which, along with decreased distressed sales has helped boost prices. The tight inventories and increased prices are projected to lead to increased residential construction in coming months.

Increases in home values have helped to improve both equity and single-family mortgage loan performance. The Mortgage Bankers Association's National Delinquency Survey showed both delinquency and foreclosure rates continuing to improve and some measures approaching pre-recession levels. Early stage delinquency edged down to the lowest level since 1972, reflecting tightening labor market conditions and the overall current quality of mortgage debt outstanding.

Recent Federal Housing Administration and Federal Housing Finance Agency policy changes have helped ease lending standards and this was reflected in the Federal Reserve's Senior Loan Officer Opinion Survey in which a large majority of banks indicated loosening lending standards for GSE and government mortgages. Likewise the first quarter Lender Sentiment Survey from Fannie Mae showed that the majority of lenders surveyed believed that the GSEs' 97 percent LTV products and the reduction in FHA's mortgage insurance premiums will benefit consumers and lenders. Roughly two out of three lenders surveyed expect that these changes will somewhat increase mortgage originations.

Real disposable income growth picked up during the first quarter, and Fannie Mae expects ongoing improvement to help boost household formation and lift housing activity. Household formation rose by 1.7 million in the fourth quarter compared to a year earlier and another 1.5 million in the first quarter of 2015, still homeownership declined 1.1 percentage points over the past year to the lowest reading since the early 1990s, as new households turned to renting.

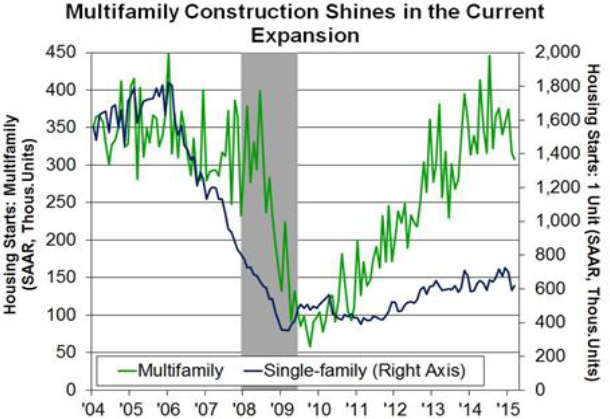

Construction activity responded to the strong demand for rental properties and multifamily starts rebounded sharply after the recession ended, rising to prerecession levels during last summer but pulling back this year. This drop should be temporary as rents continue to rise and help to support the sector.

Despite the popularity of renting Fannie Mae says the recent faster pace of household formation is encouraging. If income growth continues to improve many households should, at some point, switch from renting to owning, especially considering that mortgage rates remain historically low and underwriting standards are becoming more favorable for first-time homebuyers.

Despite some disappointment during the first quarter Fannie Mae says housing activity so far is in line with its forecast of a moderate but broad-based improvement in 2015 and while its forecast of total home sales is little changed it is more upbeat about mortgage originations. Both refinancing and purchase originations appear stronger than expected and the company has upgraded mortgage originations by 14 percent for earlier forecasts. Originations should total $1.46 trillion this year, up 23 percent from 2014. The refinance share is projected at 46 percent an increase of 3 percentage points over 2014.