The National Association of Realtors today released Existing Home Sales data for April 2011

Existing Home Sales report on the number of completed real estate sales transactions on single-family homes, townhomes, condominiums and co-ops. The methodology in calculating existing-home sales statistics is really quite simple. Each month the National Association of Realtor® receives data on existing-home sales from local associations/boards and multiple listing services (MLS) nationwide. The monthly EHS economic indicator is based on a representative sample of 160 Boards/MLSs. NAR captures 30-40% of all existing-home sale transactions with its monthly survey.

HERE is the methodology for the data collection

Quick Recap from Reuters...

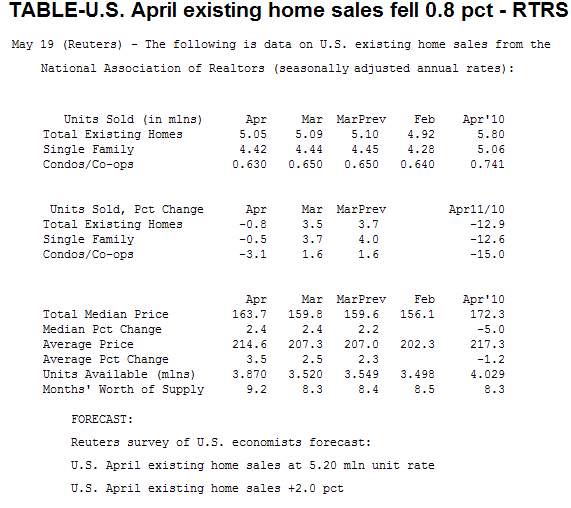

RTRS - US APRIL EXISTING HOME SALES 5.05 MLN UNIT ANNUAL RATE (CONS 5.20 MLN) VS MARCH 5.09 MLN (PRV 5.10 MLN)-NAR

RTRS - US APRIL EXISTING HOME SALES -0.8 PCT (CONS +2.0 PCT) VS MARCH +3.5 PCT (PREV +3.7 PCT)-NAR

RTRS - US APRIL INVENTORY OF HOMES FOR SALE +9.9 PCT TO 3.87 MLN UNITS, 9.2 MONTHS' SUPPLY-NAR

RTRS - US APRIL NATIONAL MEDIAN PRICE FOR EXISTING HOMES $163,700, -5.0 PCT FROM APRIL 2010-NAR

RTRS - US NAR SAYS 37 PCT OF U.S. APRIL EXISTING HOME SALES WERE DISTRESSED SALES VERSUS 40 PCT IN MARCH

Excerpts from the Release...

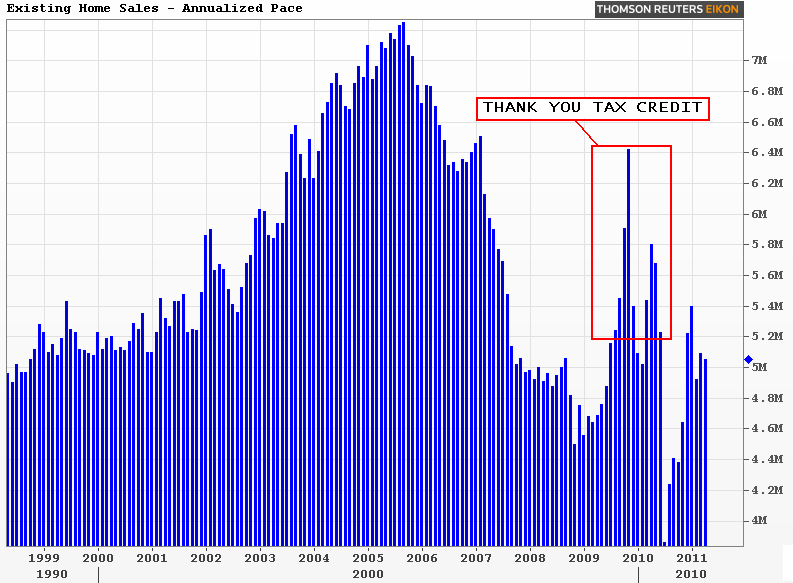

Existing-home sales slipped in April, although the market has managed six gains in the past nine months, according to the National Association of Realtors®.

Existing-home sales, which are completed transactions that include single-family, townhomes, condominiums and co-ops, eased 0.8 percent to a seasonally adjusted annual rate of 5.05 million in April from a downwardly revised 5.09 million in March, and are 12.9 percent below a 5.80 million pace in April 2010; sales surged in April and May of 2010 in response to the home buyer tax credit.

Single-family home sales slipped 0.5 percent to a seasonally adjusted annual rate of 4.42 million in April from 4.44 million in March, and are 12.6 percent below the 5.06 million pace in April 2010. Existing condominium and co-op sales fell 3.1 percent to a seasonally adjusted annual rate of 630,000 in April from 650,000 in March, and are 15.0 percent below the 741,000-unit level one year ago.

Regionally, existing-home sales in the Northeast fell 7.5 percent to an annual pace of 740,000 in April and are 32.1 percent below a year-ago surge. Existing-home sales in the Midwest rose 5.7 percent in April to a level of 1.12 million but are 16.4 percent below a cyclical peak in April 2010. In the South, existing-home sales declined 4.1 percent to an annual pace of 1.95 million in April and are 9.3 percent below a year ago. Existing-home sales in the West slipped 1.6 percent to an annual level of 1.24 million in April and are 0.8 percent below April 2010.

Lawrence Yun, NAR chief economist, said the market is underperforming. “Given the great affordability conditions, job creation and pent-up demand, home sales should be stronger,” he said. “Although existing-home sales are expected to trend up unevenly through next year, unnecessarily tight credit is continuing to restrain the market, along with a steady level of low appraisals that result in contract cancellations.

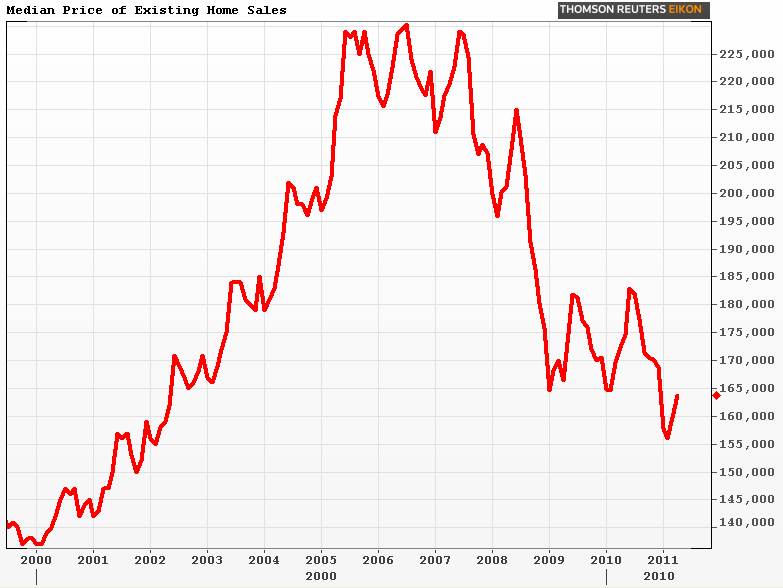

The national median existing-home price for all housing types was $163,700 in April, which is 5.0 percent below April 2010. The median existing single-family home price was $163,200 in April, which is 5.4 percent below a year ago. The median existing condo price was $167,300 in April, down 2.3 percent from April 2010.

“Home values, despite month-to-month volatility, have been remarkably stable in the range of $160,000 to $170,000 for the past three years,” Yun said. “Stable home prices in turn will steadily lower loan default rates, including strategic defaults.”

The median price in the Northeast was $225,400, which is 7.3 percent below April 2010. The median price in the Midwest was $133,200, down 5.1 percent from a year ago. The median price in the South was $142,800, which is 4.1 percent lower than April 2010. The median price in the West was $203,400, down 6.1 percent from a year ago.

Distressed homes – typically sold at a discount of about 20 percent – accounted for 37 percent of sales in April, down from 40 percent in March; they were 33 percent in April 2010.

A parallel NAR practitioner survey shows 11 percent of Realtors® report a contract was cancelled in April from an appraisal coming in below the price negotiated between a buyer and seller, 10 percent had a contract delayed, and 14 percent said a contract was renegotiated to a lower sales price as a result of a low appraisal.

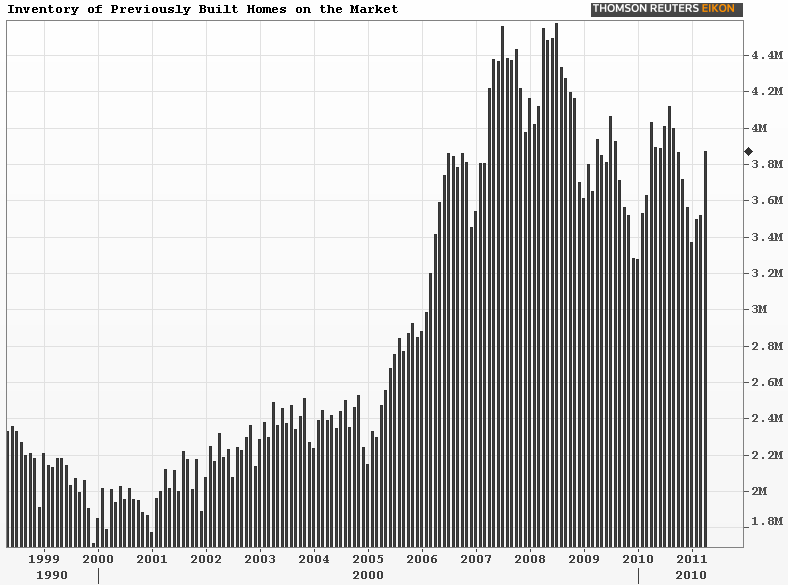

Total housing inventory at the end of April increased 9.9 percent to 3.87 million existing homes available for sale, which represents a 9.2-month supply at the current sales pace, up from an 8.3-month supply in March.

“Although sales are clearly up from the cyclical lows of last summer, home sales are being held back 15 to 20 percent due to the very restrictive loan underwriting standards,” Yun said.

NAR President Ron Phipps, broker-president of Phipps Realty in Warwick, R.I., said the lending community needs to return to sensible standards. “We want to ensure that qualified buyers will be able to own their property on a sustained basis from a sound credit evaluation, but banks needn’t be so stingy as to only lend to those with the highest credit scores,” he said.

All-cash transactions stood at 31 percent in April, down from a record level of 35 percent in March; they were 26 percent in March 2010; investors account for the bulk of cash purchases.

“Very high shares of cash purchases, and high credit score requirements, have led to historically low default rates among home buyers over the past two years. This trend implies a gulf is opening between those who can and cannot have access to the American dream of home ownership,” Phipps said. “At the same time, existing guidelines from Freddie Mac and Fannie Mae must be fully implemented so all appraisals are done by valuators with local expertise.”

Phipps added that proposals and regulations are being considered in Washington that could further constrain the housing market. “One of the most damaging proposals would effectively raise downpayment requirements to 20 percent, which would slam the brakes on the housing market,” he said. “What we need to do is simply return to the sound standards that were in place before the introduction of risky mortgage products.”

First-time buyers purchased 36 percent of homes in April, up from 33

percent in March; they were 49 percent in April 2010 when the tax credit

was in place. Investors slipped to 20 percent in April from 22 percent

of purchase activity in March; they were 15 percent in April 2010. The

balance of sales was to repeat buyers, which were 44 percent in April..

“Our data shows only one out of five first-time buyers needing a mortgage could afford a 20 percent downpayment, and without first-time buyers the trade-up market would stall with very negative consequences for housing and the overall economy,” Phipps said. “Ironically, low downpayment FHA and VA loans, which are so critical to this segment, have performed well and never needed a taxpayer bailout because those borrowers stayed well within their budgets.” NAR consumer survey data shows 56 percent of entry level buyers in the past year financed with an FHA loan.

READ MORE: Existing Home Sales Still Hindered by Uber Tight Lending Regs

READ MORE: Tight Credit Limits Home Buyer Demand. Cash is King