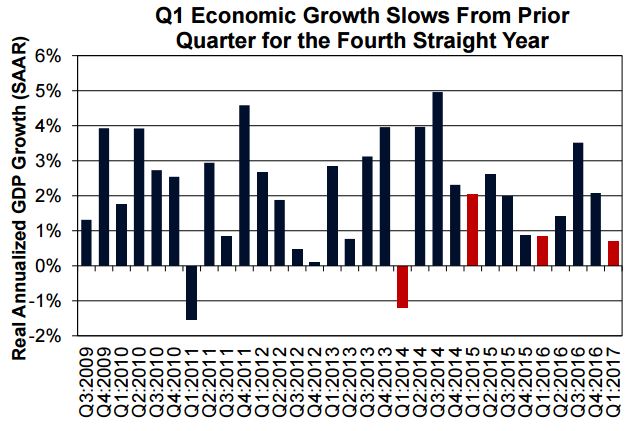

Fannie Mae's Economic and Strategic Research Team had as a headline for its May forecast, It's Déjà Vu All Over (and Over) Again. Déjà vu indeed, as for the fourth straight year first quarter economic growth slowed from the preceding quarter. Annualized real gross domestic product (GDP) came in at an anemic 0.7 percent, down from 2.1 percent in the fourth quarter of 2016. Fannie Mae's economists say that, based on these results, they are keeping their full-year 2017 growth projection at 2.0 percent. This presumes that history will also repeat itself with a rebound of growth in the second quarter, which has happened in the last three years.

The Fannie Mae report blames the Q1 slowdown principally on consumer spending, formerly the biggest driver of growth during the expansion. It grew at only 0.3 percent annualized and added only 0.2 point to the GDP, its smallest contribution since the end of 2009.

The biggest factor in the sparse growth came from nonresidential investment in structures, which added 0.6 point, but housing was another bright spot. Real residential investment posted the first double-digit gain since the end of 2015, and added a half point to growth. The outsized contributions from both nonresidential and residential investment are expected to moderate in the second quarter.

The Federal Reserve appeared to downplay the modest first quarter growth at the May Open Market Committee meeting. The Fed appears determined to stick to its guns, and Fannie holds to its earlier expectations for rate hikes in June and September and for the Fed to start shrinking reinvestments in December.

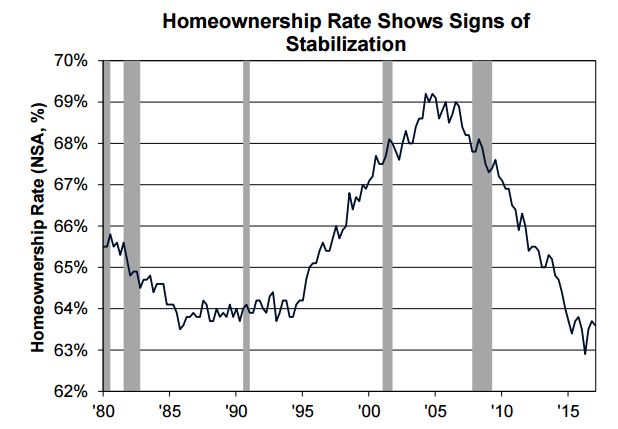

Household formation has gradually improved since the recession, with the number of households increasing by 1.2 million in the first quarter from a year ago, and homeownership may be stabilizing. While it ticked down slightly from the fourth quarter to 63.6 percent, that is 0.1 point higher than it was in the first quarter of 2016.

Fannie Mae says young adults are likely part of the reason homeownership trending higher, appearing to finally be entering homeownership as their employment situation improves. During the early part of their recovery the unemployment rate for those 25 to 34, typically a pool of first-time home buyers, was substantially higher than the overall unemployment rate. Over the last year their rate has fallen into line with that of other workers. The employment-to-population ratio for that age group has also improved significantly, coming close to that of all prime working-age adults so far this year for the first time since the early 2000s.

Single-family construction starts declined from the post-crisis high reached during an unseasonably warm February and permits also fell in March from the previous month's expansion high. Through the first quarter of the year, single-family starts are 6.0 percent higher than during the same period last year but single-family construction remains at historic lows for an expansion. Home builders report labor constraints as a top issue and government surveys such as the Job Openings and Labor Turnover Survey (JOLTS) suggest a competitive market for construction workers. JOLTS showed that the quits rate, a gauge of workers' confidence in the jobs market, has been trending up over the past year for construction workers, compared with a relatively stable rate for the workforce over all.

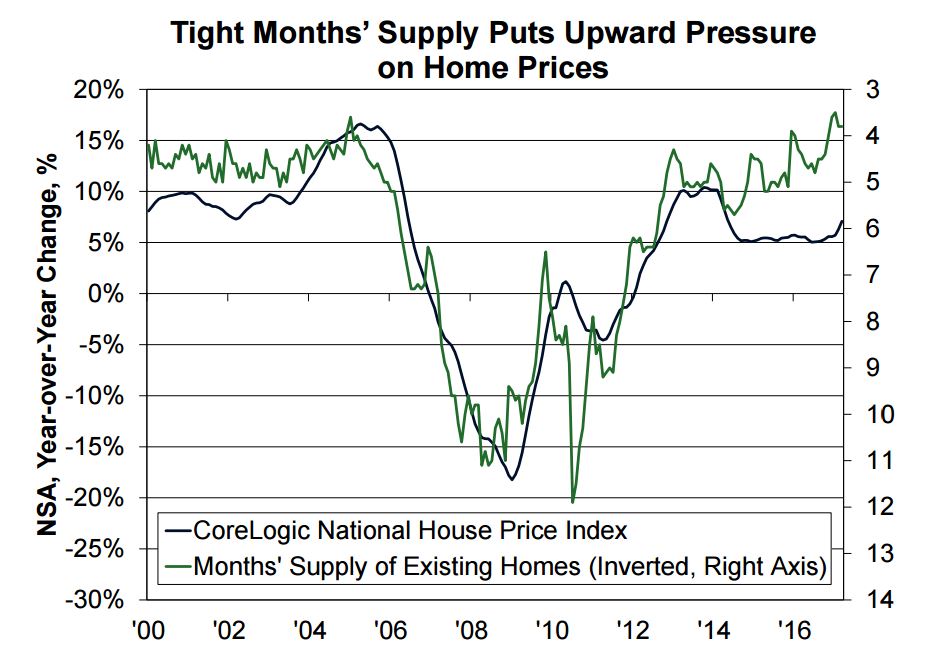

Home sales had a good month in March with new home activity up for the third straight month, falling just shy of an expansion best, while existing home sales did set a post crisis record. Inventories are still a problem; the supply of existing homes has remained below four months since December. This provides a "tailwind" for housing prices and the FHFA, Case-Shiller, and CoreLogic price indices showed annual price increases accelerating in either February or March.

The company has revised its forecast for mortgage originations in 2016 by about $90 billion to $2.05 trillion. For this year, they have revised their earlier 2017 estimate up slightly to $1.59 trillion, a 22 percent decline from 2016, as the drop in refinancing will more than offset increases in purchase originations. The refinance share is expected to be 32 percent this year, compared to 48 percent in 2016.