In the company's loan performance report for January, Frank Martell, CoreLogic's president and CEO said, "Except for the metropolitan areas affected by natural disasters, most of the country has seen delinquency and foreclosure rates move lower over the past year. Declines in the unemployment rate have supported a rise in income and home-price growth has built home equity. These two economic forces coupled with high-quality underwriting have lowered overall delinquency rates."

The national rate for loans that were 30 or more days past due declined from 5.1 percent of active loans in January 2017 to 4.9 percent 12 months later, but that improvement would have been greater absent the push higher from two states. Besides being among the nation's most populous, Texas and Florida bore the brunt of last fall's twin hurricanes and were the only two states where delinquencies increased year-over-year. The delinquency rate in Florida, which was 6.0 percent in January 2017 had risen to 8.4 percent by this January's report. In Texas the year-over-year increase of 0.7 percentage point brought the rate to 6.3 percent.

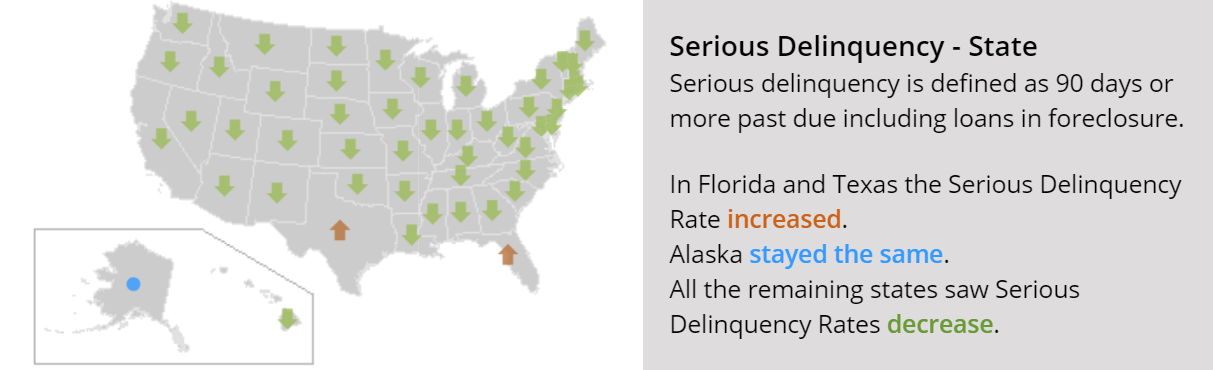

The higher rates in those states are increasingly due to serious delinquencies. While the national rate for loans more than 90 days past due but not in foreclosure was 2.1 percent, down from 2.3 percent the prior January, the rate in Texas was up 0.8 percent to 2.7 percent while in Florida it grew 1.9 point to 5.1 percent. However, in both states the foreclosure inventory rate declined as it did nationally as well, moving from 0.8 percent in January 2017 to 0.6 percent in January 2018. Many lenders have or had put foreclosure moratoria in effect after the storms.

CoreLogic's chief economist Frank Nothaft said, "The areas hit by last year's hurricanes and wildfires are experiencing the "pig in a python" effect on their local delinquency rates, a bulge in an otherwise level trend. This means that although early-stage delinquencies have largely dropped back to normal, serious delinquency remains elevated. In hard-hit markets, like the Houston and Naples metro areas, serous delinquency is triple what it was before the hurricanes." Nothaft noted that, in the San Juan area of Puerto Rico, not included in national statistics, serious delinquency has quadrupled.

The effects of natural disasters are even more clearly seen on the metro level. CoreLogic identifies 31 Core Based Statistical Areas (CBSAs) where the serious delinquency rate increased. All but two are in either Texas or Florida. The outliers were Fairbanks, which has been suffering from the decline in oil prices, and Santa Rosa, California where a wildfire last fall leveled much of the town. There the 30-day rate jumped a half-point to 2.4 percent while serious delinquencies rose from 0.7 percent to 1.0 percent for the 12 months ended in January. In 11 other CBSA's the serious delinquency rate was unchanged.

CoreLogic also looks at transition rates that indicate the percent of mortgages moving from one stage of delinquency to the next. The rate for those that transitioned from current to 30-days past due was 0.8 percent in January 2018, down from 1.1 percent in December 2017 and down from 0.9 percent in January 2017. By comparison, in January 2007, just before the start of the financial crisis, the current-to-30-day transition rate was 1.2 percent and peaked in November 2008 at 2 percent.