A recent Freddie Mac Insights article looks back at earlier incidences of rising rate environments, and how the higher rates affected several populations including borrowers, mortgage lenders, homeowners, real estate agents, and home builders. MND summarized those findings in an earlier article and today we look at the second half of the analysis. Doug McManus, Freddie Mac Quantitative Analytics Director and Elias Yannopoulos, Quantitative Analytics Senior, consider the risk factors that drive movements in mortgage rates and the possibilities for rate changes in the near- to mid-term.

Lenders and guarantors have three main risks when issuing a mortgage: credit risk, prepayment risk, and inflation risk. Credit risk is the possibility that the borrower might not pay back the loan. Conversely, there is a risk that borrowers will pay back but do so early, cutting off future interest income for the lender. Inflation creates the risk that money in the future will have less purchasing power than today.

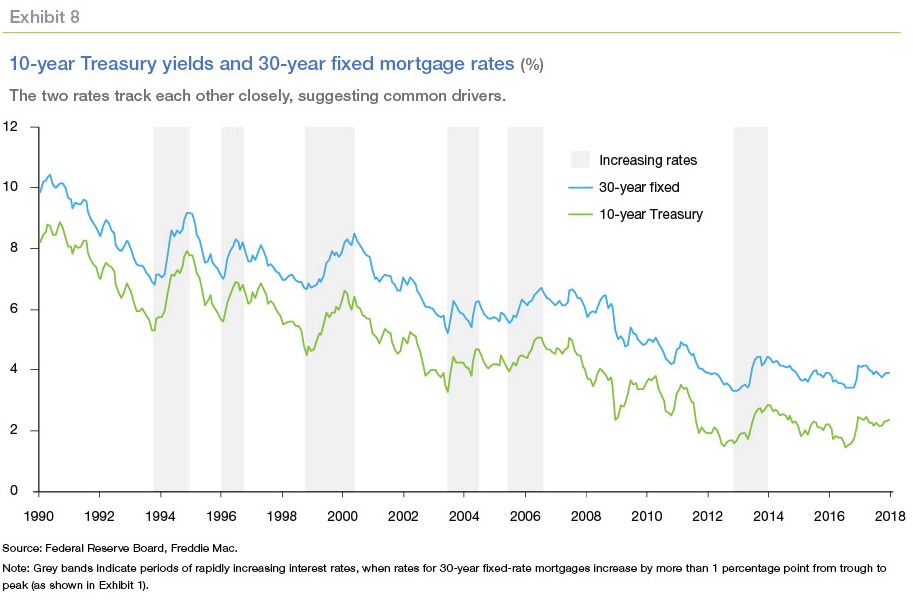

The authors say it is the expected inflation risk that drives movements in mortgage rates and this is also the primary risk associated with Treasury securities. Exhibit 8 compares movements in the yield of the 10-year U. S. Treasury bond with mortgage rates showing the drivers of the 10-year T-note are also the dominant drivers of mortgage rates. Even knowing rates are driven primarily by inflation risk, predicting future changes is challenging because it involves predicting changes in the inflation expectations and effects of those expectations on supply of and demand for credit.

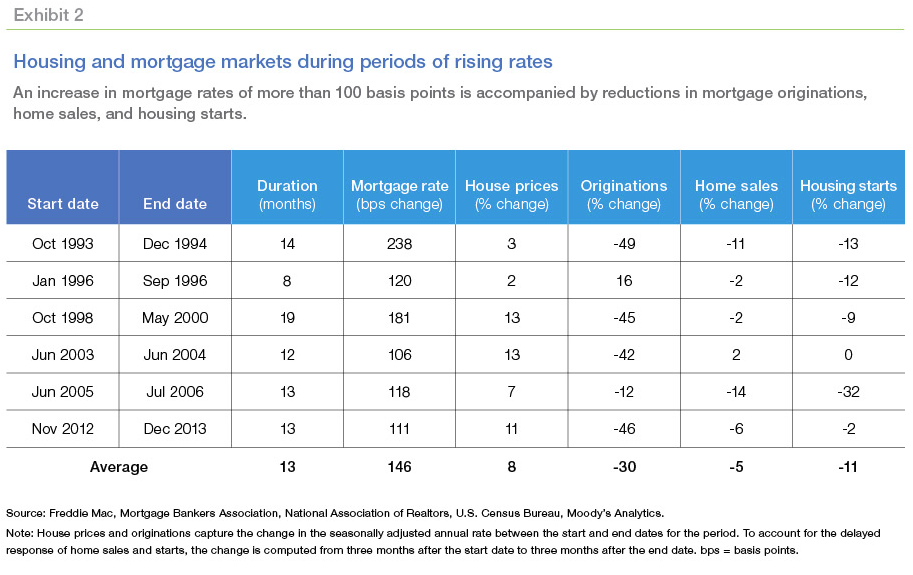

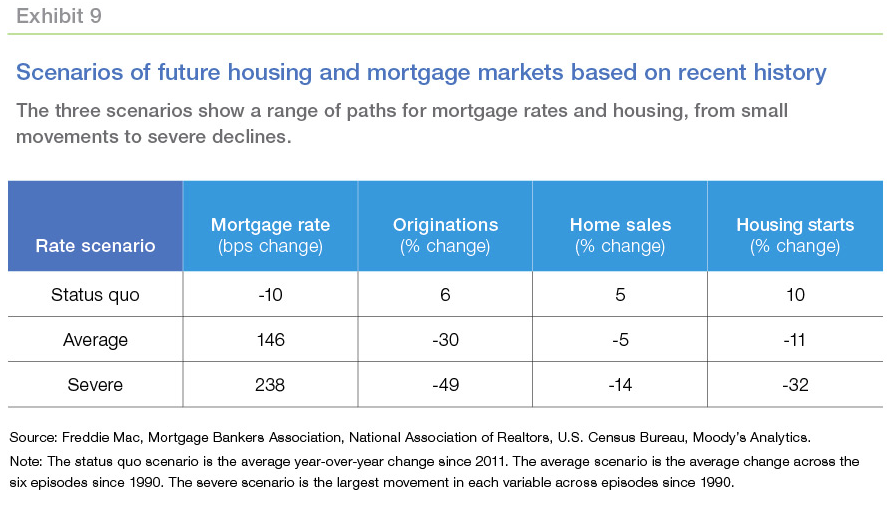

The authors put forth scenarios that capture three possible outcomes of the next mortgage rate cycle. The first is a continuation of present conditions, with rates hovering between 3.5 and 4.5 percent. The second is an average of the market experience during the six prior rising rate environments outlined in the earlier article and shown in Exhibit 2. The third scenario is based on the most extreme movements in housing and mortgage markets during those six episodes.

The first scenario would produce movement in the housing markets at the average annual change since 2011. This scenario corresponds to continued expectations for low inflation, and possibly to what some economists refer to as "secular stagnation" which would result from a combination of increases in the supply of capital, continued weak aggregate demand for capital, slower productivity growth. Low rates would be accompanied by less than full employment and low growth.

The second and "average" scenario would see interest rates rising by 146 basis point from the trough to peak and implies expectation of a "meaningful" increase in inflation. Since the recent low in the 30-year fixed-rate was 3.81 percent (monthly average) in September 2016, that average increase would put the peak rate at 5.27 percent. Freddie Mac's Primary Mortgage Market Survey (PMMS) reached an average of 4.40 percent during the week ended February 22, putting the expected increase in this scenario more than one-third of the way after the increases began early this year. Under this rate scenario, mortgage originations are expected to fall by 30 percent, accompanied by more modest declines in home sales of 5 percent, and a decline in housing construction starts of 11 percent.

The final scenario calls for an increase over a longer period and rates remaining elevated for an extended period. The last time this happened was from 1977 to 1981, resulting in a peak mortgage rate at over 18.5 percent. The third scenario could happen if inflation and expectations of future inflation increase. The 1977-81 rates were accompanied by double-digit increases in consumer prices. Freddie Mac says this severe scenario is estimated by taking the maximum movements during periods of increased rates since 1990. Under this scenario, mortgage rates are expected to increase by 238 basis points, with a 49 percent drop in mortgage origination volume, a 14 percent decrease in home sales, and a 32 percent decline in housing starts.

Of course, these are speculations, but the authors say understanding the incentive of market participants and the historical context can help us understand what the response might be to given movements in rates. "The expected increase in mortgage rates would suppress growth in the mortgage and housing markets, and lead to declining markets if the increase is large enough or lasts for long enough. But for now, mortgage credit is still historically cheap if you get in while the getting is good."