Some people are never happy. For most of the ten years following the start of the Great Recession the experts have focused (can we say harped?) on the theme of a slow recovery. Now, after a couple of upticks in the inflation rate, Fannie Mae has headlined its February Economic Developments release "Strong Economic Activity Triggers Overheating Concerns."

The company's Economic and Strategic Research Team say economic activity gathered momentum over the last few months and "markets are beginning to appreciate the broader implications of the stronger growth. That realization, along with a change in the direction of monetary policy has introduced some volatility into the economic equation.

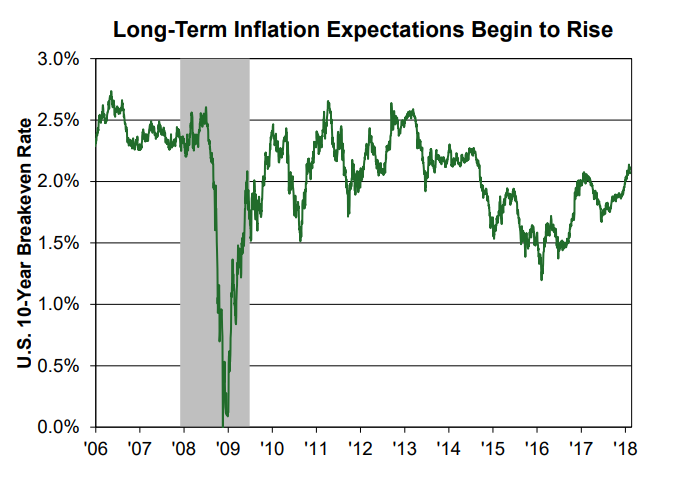

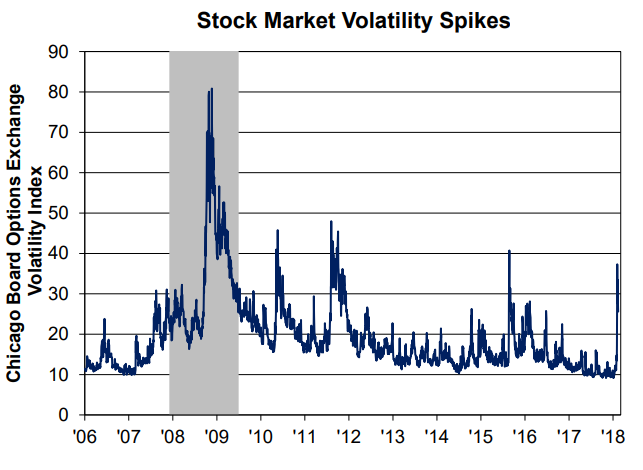

There were finally some signs that wages were increasing which pushed inflation measures such as 10-year Treasury rates higher and along with them, increases in the 30-year fixed rate mortgage rate. The latter, at the time the economists were compiling their report, had increased for five straight weeks and had reached its highest point since the end of 2016. They say it was long-term rate expectations that introduced volatility into what had been a persistently stable equity market and caused a wild week of market fluctuations, and an official correction in the Dow.

The company is holding fast to its earlier forecast for economic growth at 2.7 percent, but with the caveat that sustained declines in the stock market or a spread to other markets are downside risks. There are also upside risks from passage of the Budget Act of 2018. It will raise discretionary spending by nearly $300 billion over the next two years and extend the debt ceiling until March 1, 2019. Combined with the recently passed Tax Act, the 2018 budget will likely worsen the deficit outlook, implying a rising supply of Treasuries and higher yields.

The report states that "While we expect lower tax rates to induce increased investment and labor supply, the addition of deficit-financed stimulus at a time when the economy is already near full employment is likely to stoke more concerns over rising inflationary pressure and could require more aggressive monetary actions to offset the fiscal stimulus. Thus, Fiscal Policy and the Fed: Stimulus/Response-our theme for 2018-underpins the health of the economic expansion."

After its January meeting the Federal Open Market Committee (FOMC) said inflation still hadn't met the FOMC target and that its favored indicator, the PCE deflator, was down slightly in December. Fannie Mae says however that they still expect the Fed to raise its funds rate in March and that there will be two more increases this year, likely in June and December. Any March increase, they say, has already been fully priced in by the futures market.

The company sees three factors impacting mortgage interest rates this year, and all point to higher rates and wider spreads. As the Fed lets its MBS portfolio run off, more marginal investors will pick up the volume and they will require higher yields. This should start mid-year. Second, the higher rate environment is causing increased competition and reducing lender profit margins. The competition will cause some industry downsizing that will reduce capacity and ultimately lead to wider spreads and higher profits for those that survive. Third, the higher guaranty fee structure that was ushered in to reflect market risk will almost certainly survive the Fed departure from the MBS market.

Higher rates will result in a significant reduction in refinance volume, and that has already started to happen. The impact on the home purchase market will depend on how fast rates increase. "Recalling the evidence from the 'Taper Tantrum' of 2013, the home purchase market does not respond well to large, rapid moves in mortgage rates. However, if rates move up in reasonable alignment with household income growth, the home purchase market can do well in a rising rate environment," the report says.

Fannie Mae's forecasts for home sales and prices are unchanged from previous reports. They expect the Tax Act will provide enough of a boost to disposable income to offset higher rates and will likely hurt price appreciation at the higher end of the price scale but increase the incentive to buy moderately priced homes. However, they did revise their interest rate forecast because of a more rapid acceleration in long-term rates at the beginning of the year. They now expect 30-year fixed rate mortgages to average 4.4 percent during the fourth quarter, 30 basis points higher than their earlier forecast.