Freddie Mae's Outlook for January looks at the uncertainties facing the housing market heading into the second month of 2017. While acknowledging that the economy is now in its eighth year of expansion, that housing is coming off its best year in a decade, and the prospects remain good for future growth, the company's economists say any forecasts for the future must take into account "uncertainty about fiscal policy, foreign investments in U.S. real estate, and the size of the mortgage market."

Post-election, expectations about economic policy, especially fiscal policy, have shifted. The writers assume there will be an expansionary policy that will boost both growth and inflation this year and next and that corporate tax reform will increase long-term potential growth by about two-tenths of a percentage point.

Among the new president's tax proposals are those that will increase standard deductions and flatten marginal personal income tax rate. The former will reduce incentives to itemize deductions including the mortgage interest deduction; the latter will shift the attractiveness of homeownership for those who do continue to itemize. The Tax Policy Center estimates that increasing the standard deduction will reduce the number of filers who itemize from 45 million to 27 million, a 60 percent decline. The taxpayer who no longer itemizes and owns a $250,000 home with a 4.25 percent 30-year, fixed-rate mortgage will face an increase of $200 per month in taxes. Reducing the marginal tax rate also increases the cost of homeownership but by a smaller amount, perhaps $75 or less, depending on the tax bracket. The impact of tax policy changes on homeownership is difficult to predict; reducing taxes may boost income but shifting tax policy could reduce borrowing power.

Another area where economic policy could affect housing markets is foreign investment in real estate. It represents a significant share of the residential market and has seen recent increases, rising 3 percent over the four quarters ending in March 2016 compared to the year earlier period. During that period, there were over 200,000 residential properties purchased by foreign buyers. This is a market impacted by economic, political, and social factors including currency fluctuations.

A contraction in foreign demand would have little impact on many housing markets but there are others that are especially reliant on these buyers. Fifty-five percent of foreign residential purchases were concentrated in Florida (22 percent), California (15 percent) Texas (10 percent), and Arizona and New York (4 percent each.)

There is also uncertainty about the size of overall housing finance markets. Rates are already higher than in January 2016 and Freddie Mac forecasts they will continue to climb throughout the year, dampening housing and mortgage activity. However, both the size of the contraction and its character are unknown. The analysis reminds of repeated occurrences over the last few years, especially in 2012, when long-term interest rate increases were short-lived. Global actions including low or even negative long-term interest rates in much of the developed world and Brexit have helped to contain U.S. Treasury yields and, with them, mortgage rates. Upcoming elections scheduled in several European countries this spring could repeat the Brexit effect on the U.S. bond market and interest rates.

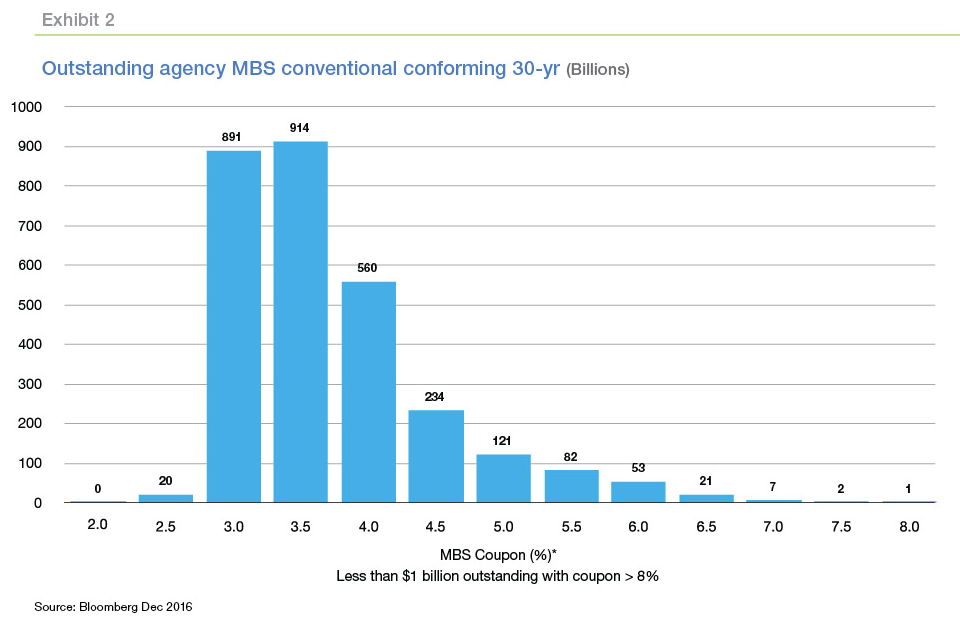

Even if rates head higher, there is no way of knowing how much refinancing will be affected although it is certain that rate driven refinances will decline significantly. Per data from Bloomberg there are $286 billion in outstanding conventional 30-year mortgage-backed securities (MBS) with a coupon greater than 4.5 percent. This provides a rough upper bound on the potential rate refinance volume in 2016 from conventional conforming 30-year loans, far less than the $655 billion Freddie Mac identified last January as refinanceable loans.

There is, however, a universe of potential refinancers who could seek to extend their loan terms or tap equity through a cash-out refinance. Rising home prices have increased homeowner equity to about 13.0 trillion through the end of the third quarter of 2016, up about $7 trillion since the second quarter of 2011. This equity could be tapped but Freddie Mac says not to expect the surge in cash-out refinancing that occurred before the housing crisis.

The writers cite a speech given last month by New York Federal Reserve Bank President William Dudley who pointed to the shift in borrower behavior as regards home equity and consumer consumption. Unlike in prior periods when house prices rose, much of the home equity of households today remains "locked in" their homes. Should homeowners decide to liberate some of this equity there could be an increase in origination activity.

It is still unlikely that cash-out refinance activity can offset the more than $500 billion decline in rate refinance activity Freddie Mac expects. In 2015, there were about $65 billion in total combined cash-out and second mortgage consolidations, up from a low of $42 billion in 2014, but far below the $348 billion in 2006. Even if cash-out refinance activity was to double from 2015 levels, it would only replace 11 percent of the reduction in rate refinance activity.

There could also be a resurgence in adjustable rate mortgage (ARM) originations. The recent low rates allowed many borrowers to refinance from ARMs into fixed rate products and Freddie Mac estimates that less than 1 percent of refinancing borrowers in the third quarter of 2016 opted for ARMs. But historically as rates have risen so has the ARM share of refis, and if long-term rates rise as expected more buyers may chose these products. Some borrowers may find they can save on payments despite higher rates by refinancing a fixed-rate loan into an ARM, others may choose another ARM when their existing ARM rate resets.

Freddie Mac's economists conclude that, while cash-outs and ARMs will provide some offsetting originations, overall mortgage refinance activity is set to decline significantly in 2017. Their forecast of $425 billion in refinance originations would be the lowest annual total since 2000, not adjusting for inflation. They admit they could be surprised with lower than expected rates in 2017, or "locked in" home equity could drive a surge in additional refinance activity. "However, among the many uncertainties we highlighted, a smaller mortgage market in 2017 than 2016 seems most certain."