The Urban Institute releases a regular report, Housing Finance at a Glance, a "chartbook" loaded with charts and commentary on mortgage activity. The current edition is primarily for the period ending with the third quarter of 2016. Much of the material, credit access, residential construction data, home prices indices, etc., has been covered by MND from original sources, but we have cherry-picked a few items that may have otherwise escaped notice.

Overview of Housing and Mortgage Market Value

The total value of the housing market, as reported by the Federal Reserve's Flow of Funds report has been steadily increasing since 2012, driven by growing household equity. In the third quarter of 2016 total debt and mortgages rose to 10.2 trillion and household equity grew to 13.7 trillion, a total of $23.9 trillion.

Agency MBS account for 58.2 percent of the total mortgage market, first liens held by Freddie Mac, Fannie Mae (the GSEs) and depository institutions make up 29.8 percent, and private-label securities (PLS) 5.8 percent. The remaining 6.2 percent are second mortgage liens. The dollar value of those shares is shown in the table below.

The market share of debt in the PLS market (as of November, 2016) equated to $556 billion and was split among prime ($110 billion or 18.9 percent), Alt-A ($230 billion or 41.2 percent), and subprime ($220 billion or 40.0 percent) loans. In December 2016, outstanding securities in the agency market totaled $6.07 trillion and were 44.4 percent Fannie Mae, 27.5 percent Freddie Mac, and 28.1 percent Ginnie Mae. Ginnie Mae has had more outstanding securities than Freddie since May 2016.

First Lien

Originations

Total first lien originations in the first three quarters of 2016 amounted to approximately $1.49 trillion. The share of portfolio originations was 33.7 percent, up from 30.8 percent for the first three quarters of 2015. The GSE share dropped to 44.4 percent, from 45.7 percent for the same period in 2015. The FHA/VA share was roughly flat: 21.3 percent in 2016 versus 22.7 percent in 2015. Origination of private label securities is well under 1% in both years. The dollar volumes of these shares are shown below.

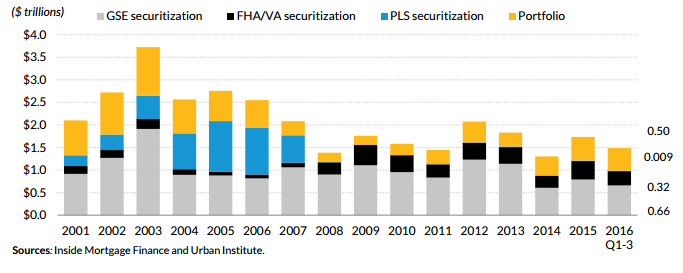

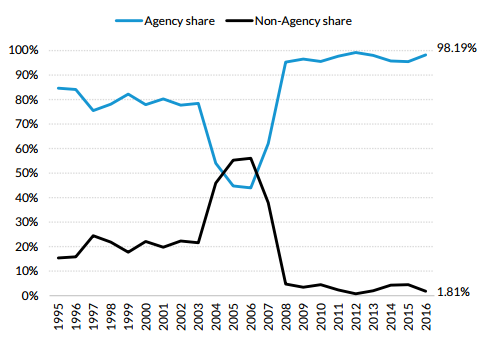

Securitization

The non-agency share of mortgage securitizations in 2016 shrunk even below the relatively small shares (compared to pre-crisis levels) in the two prior years, 1.81 percent. The share was 4.5 percent and 4.3 percent in 2015 and 2014 respectively. Of that small volume, much was in so-called scratch and dent deals, non-performing and reperforming loans. The volume of prime securitizations in 2016 totaled $9.35 billion, versus $12.08 billion in 2015. And fourth quarter 2016 prime securitizations were particularly light, totaling $1.6 billion, lower than either the preceding quarter or the fourth quarter of 2015.

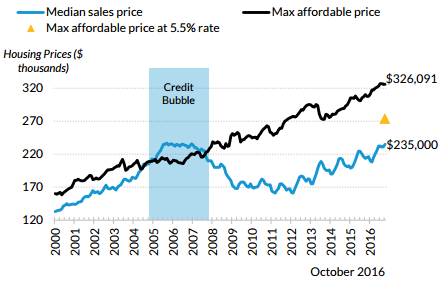

Housing Affordability

Commentary accompanying home sales data, especially from the National Association of Realtors® have reflected a lot of concern about falling levels of home affordability after four straight years of price increases. But the Chartbook says prices are still very affordable by historical standards. Even if interest rates rose to 5.5 percent, affordability would be at the long term historical average.

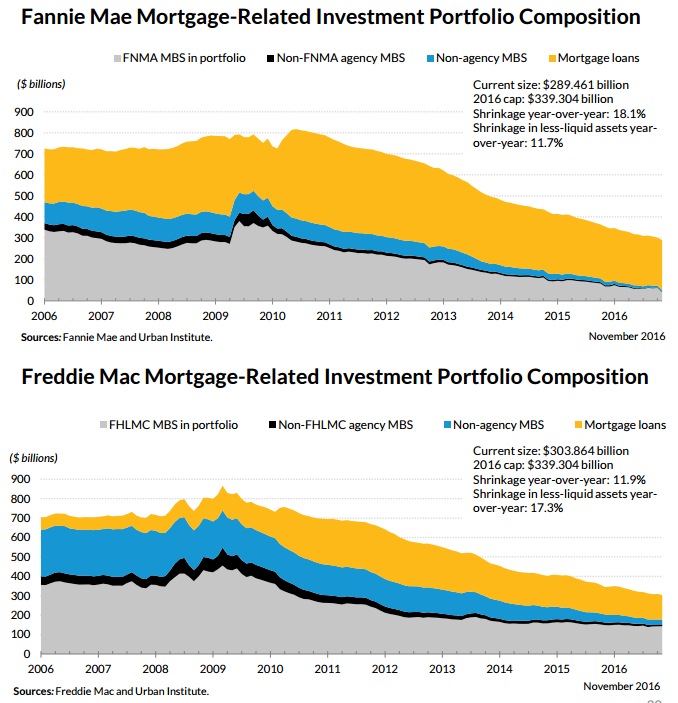

GSE Portfolio Runout

Both GSEs continue to contract their portfolios and have been under their mandated caps for 2016 since the first quarter of that year. Since November 2015, Fannie Mae contracted by 18.1 percent and Freddie Mac by 11.9 percent. They are shrinking their less liquid assets (mortgage loans and non-agency MBS) at close to the same pace that they are shrinking their total portfolios.

Looking Forward

Finally, the Urban Institute put together comparison tables from principal housing stakeholders showing their projections for home sales, mortgage originations and housing starts. Economists from both GSEs and the Mortgage Bankers Association (MBA) expect a substantial decline from the close to $2 trillion in originations in 2016, due mainly to a decline in refinancing as interest rates rise.

Fannie, Freddie, and MBA all forecast 2017 housing starts to total 1.26 to 1.31million units. Home sales forecasts for 2017 range from 5.75-6.37 million, with Freddie predicting a small drop from 2016 levels, while Fannie and MBA are expecting home sales to rise from 2016 levels, in the case of MBA, higher numbers for both new and existing homes.