Optimism is running high in Fannie Mae's first Economic and Housing Outlook of the year. The company's Economic and Strategic Research (ESR) team says expanding vaccination efforts, the potential of greater than previously expected fiscal stimulus, and the end of winter all "point to an economy ready to take off once COVID-19-related effects begin to subside."

The company says that economic growth probably flatlined in November and December and it revised its final GDP estimate for the year down to a negative 2.7 percent. The economy is now poised to expand, although probably not before late spring. The ESR team has raised its expectations for 2121 from 4.5 percent growth in last month's report to 5.3 percent and by 0.4 points for 2022 to 3.6 percent.

The Federal Reserve has stated it intends to let inflation exceed its long-term target for "some time" so Fannie may has increased its inflation forecast for the 4th quarter of 2021 and beyond. Core personal consumption expenditures (PCE) inflation should reach 2.4 percent annually by the end of 2022.

The future path of the pandemic is the biggest downside risk to the current forecast. Distribution of vaccines has been slower than anticipated, however, the economists continue to assume that warmer weather and widespread inoculations will allow removal of many economic behavioral restrictions by mid-spring.

The path of interest rates is also a major forecast risk. The 10-year Treasury yield is up over 20 basis points since the first of the year and market-based measures of inflation have trended up as well. While changes are still modest, any meaningful rise in rates would likely dampen economic, housing, and mortgage activity relative to the year-end baseline forecast. A sudden, sharp jump in rates could cause an equity market sell-off and restrain home sales and prices.

The company says the slim Democratic edge in the Senate increases the likelihood of additional fiscal stimulus. Since it remains unclear whether or when legislation would be passed or what might be included in it, the forecast doesn't incorporate any additional fiscal stimulus at this point.

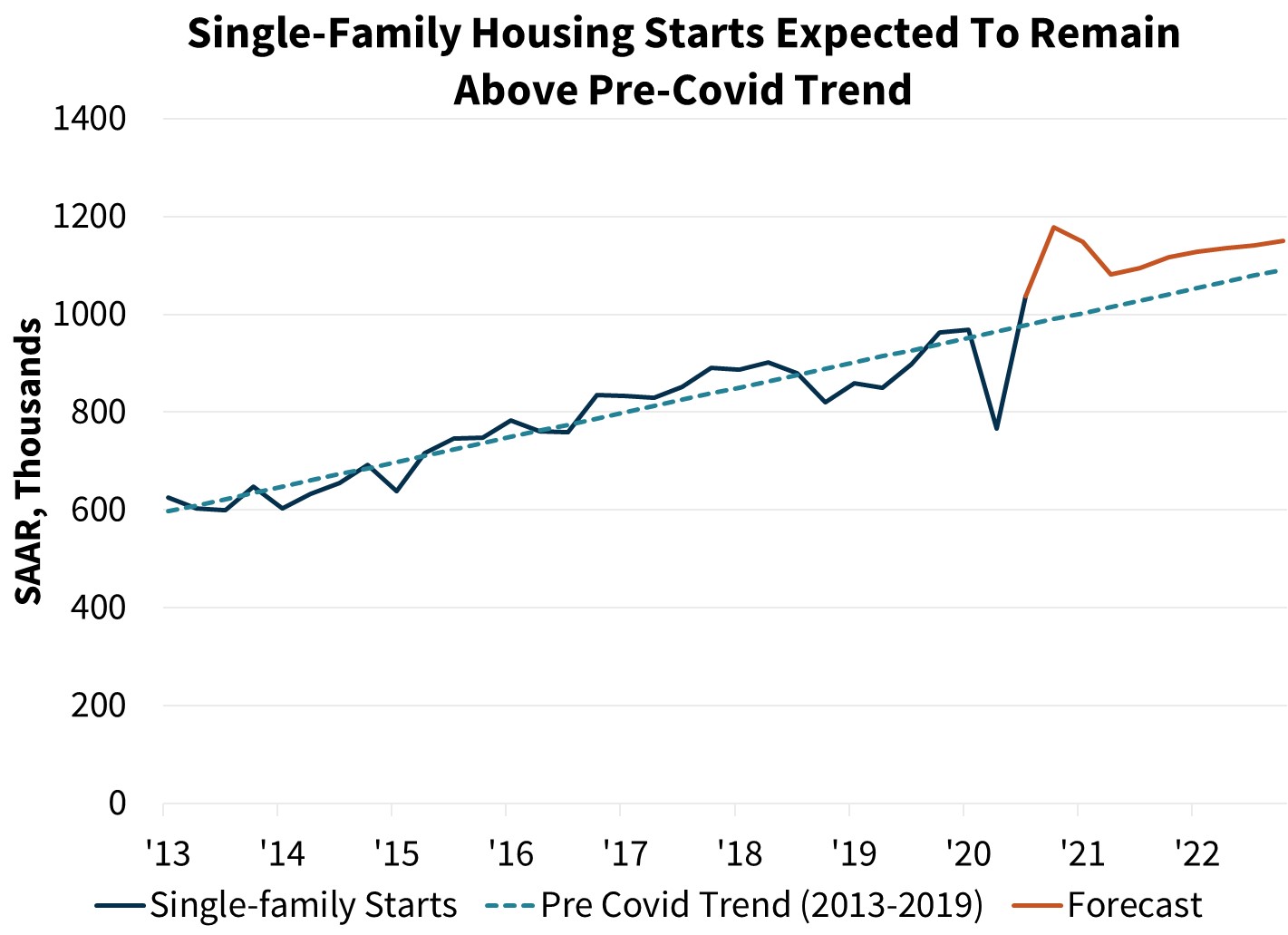

Fannie Mae expects housing to remain strong this year, however it is likely to "shift down a gear following its torrid pace during the second half of 2020." A near-term slowdown in home sales is likely but total home sales are expected to be 3.8 percent higher in 2021 than in 2020 and single-family housing starts will rise by 12.5 percent.

The 11.0 downturn in new home sales in November was at least partially due to an unsustainable relationship between housing starts and home sales over the past half-year. Sales had been bolstered by inventory drawdowns and sales contracts for homes not yet started so some combination of declining sales and accelerating starts was necessary for a sustainable balance. In addition, prior months' estimates were revised significantly downward, doing away with a lot of the starts/sales gap, and putting the sales pace on comparatively stronger footing going forward. There will be a modest near-term pullback, largely reflecting a rebalancing of the number of early- and late-stage homes under construction, after which single-family housing starts should exhibit comparable strength going forward, accounting for the 12.5 percent 2021 increase.

All of this points to an existing home sale forecast slightly above pre-pandemic trends and an even more positive outlook for single-family construction. If correct, this could be a decline in multifamily housing demand, especially in more expensive urban areas, holding those starts below their pre-COVID pace.

Despite the upbeat view on construction, housing is not expected to provide the contribution to GDP that it did over the last two quarters of 2020. Fannie Mae expects residential fixed investment will be down 3.8 percent from Q4 2020 to the same quarter this year. Some of this weakness will come from the slow deceleration in multifamily starts late last year, however the bulk of the decline will be due to heighted home improvement spending and broker commissions in Q4 which will not be sustained this year. Home improvement spending has historically been highly correlated with both home sales and rising home equity (which allows owners to borrow against their home's value). As sales and appreciation are expected to decelerate, home improvement spending is likely to follow suit.

The company upgraded its estimate for 2020 home price growth from 6.4 percent to 10.3 percent and doubled its forecast for this year to 4.2 percent. This, as well as upwardly revised sales expectations, led to another increased outlook for mortgage originations. Total originations in 2020 were $4.4 trillion ($125 billion higher than expected last month).while 2021 and 2022 originations are expected to decelerate to $3.9 trillion and $3.2 trillion ((up $440 billion and $378 billion from the prior forecasts), respectively.

Purchase volumes are now expected to total $1.6 trillion in 2020 and $1.8 trillion in 2021, upward revisions of $49 billion and $88 billion, respectively, from last month's forecast. Purchase growth is expected to decelerate in 2022, growing just 1.0 percent year-over-year, as a slower sales pace represents a drag on volumes.

Refinance origination volume in 2021 is expected to increase 20 percent over last month's forecast to $2.2 trillion, although this will still be lower than the record volume of $2.8 trillion in 2020. Fannie Mae says there is still capacity for strong refinancing volume this year, especially in the first quarter. At current interest rates, an estimated 67 percent of outstanding mortgage balances still have at least a half-percentage point refinance incentive. Volume is projected to decline further to $1.4 trillion in 2022, though remain elevated from an historical perspective, as interest rates stabilize and the share of mortgages with a rate incentive to refinance begins to wane.

Mortgage rates fell again in early January to 2.65 percent, another record low. However, the decline in rates may be nearing an end. The 10-year Treasury yield jumped in early January, narrowing mortgage spreads. The spread between the 30-year mortgage rate and the 10-year Treasury yield fell to approximately 160 basis points, the lowest since mid-2019. While the spread compression indicates falling lender margins, Fannie Mae says mortgage lenders may be willing to absorb some of this cost before passing it on to consumers through higher mortgage rates.

The ESR team says it remains a question how the unusual events of the past year will shape housing trends long-term. They speculate that the pandemic's lasting effects will include a modestly higher pace of home sales than otherwise would have occurred, as well as comparatively stronger support for new construction. They do not predict a major exodus from large urban areas but do see the expansion of remote working as enabling increased migration to the suburbs and less expensive metros even after the crisis passes. People rethinking their choices and continuing to relocate to new locations could mean a modest increase in home sales, and if those sales shift toward less expensive areas with more buildable land or less restrictive zoning, it would bode well for new single-family construction.