Mortgage delinquency rates continued to fall in October, with the national rate ticking down 0.1 percent and the percentage of non-current loans declining in all but three states. While perennial trouble spots Louisiana, Mississippi, New York, and New Jersey all saw loans that were 30 or more days past due decline by one-half percentage point or more, delinquencies were up year over year in Texas and Florida, the states hardest hit by Hurricanes Harvey and Irma, and in Alaska.

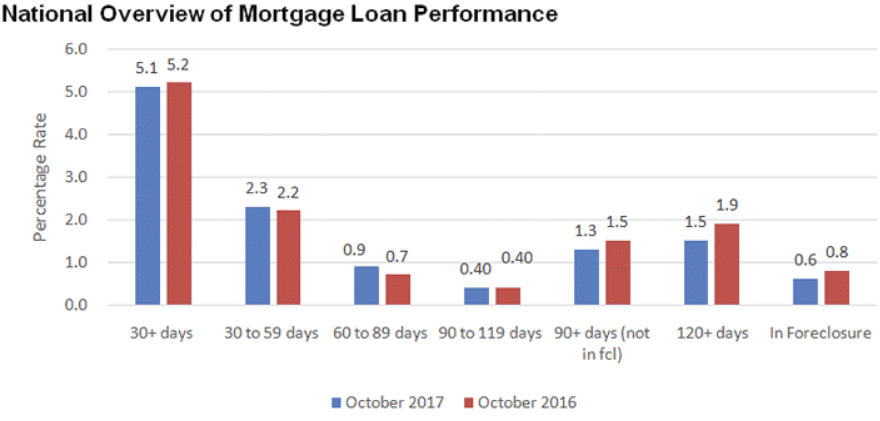

CoreLogic reports the national delinquency rate, which was 5.2 percent in October 2016 was down to 5.1 percent a year later. However, the company's monthly Loan Performance Insights Report indicates that the decrease came exclusively from the pool of serious delinquencies; early delinquencies increased. The percentage of loans 30 to 60 days past due ticked up 0.1 percent year-over-year to 2.3 percent, although they were down 0.1 percent from September. The share of mortgages that were 60-89 days past due in October 2017 was 0.9 percent, up 0.2 percentage points from 0.7 percent in both September 2017 and October 2016.

The serious delinquency rate, reflecting loans 90 days or more past due, was 1.9 percent in October, unchanged from the previous four months, and down 0.4 percentage points from October 2016. The percent rate in June, July, August, September and October of this year marks the lowest level for any month since it was also 1.9 percent in October 2007.

The year-over-year delinquency rate in the two hurricane stricken states increased substantially even as their serious delinquency rate declined. In Florida overall delinquencies rose from 6.4 percent in October 2016 to 9.7 percent but serious delinquencies fell to 2.7 percent from 3.3 percent. In Texas the overall rate rose from 5.5 percent to 6.8 percent while serious delinquencies were unchanged at 1.9 percent.

In Alaska, the third state where loan performance deteriorated, both overall and serious rates were up, from 2.5 percent to 2.9 percent and 1.0 to 1.1 percent, indicating longer term problems.

"After rising in September, early-stage delinquencies declined by 0.1 percentage points month over month in October. The temporary rise in September's early-stage delinquencies reflected the impact of the hurricanes in Texas, Florida and Puerto Rico, but now the impact from the hurricanes is fading from a national perspective," said Dr. Frank Nothaft, chief economist for CoreLogic. "While the national impact is waning, the local impact remains. Some Florida markets continue to see increases in early-stage delinquency transition rates in October, reaching 5 percent, on average, in Miami, Orlando, Tampa, Naples and Cape Coral. Texas markets such as Houston, Beaumont, Victoria and Corpus Christie peaked at over 7 percent in September, but are on the mend and improving in October."

As of October 2017, the foreclosure inventory rate, which measures the share of mortgages in some stage of the foreclosure process, was 0.6 percent, down from 0.8 percent in October 2016. The foreclosure inventory rate has held steady at 0.6 percent since August and is the lowest since June 2007 when it was also at 0.6 percent.

In addition to looking at delinquency buckets, CoreLogic also examines transition rates, which indicate the percentage of mortgages moving from one stage of delinquency to the next. The share of mortgages that transitioned from current to 30 days past due was 1.1 percent in October, down from 1.3 percent the previous month, and up from 1 percent year-over-year. By comparison, in January 2007, just before the start of the financial crisis, the current-to-30-day transition rate was 1.2 percent and it peaked in November 2008 at 2 percent.

"While the national impact of the recent hurricanes will soon fade, the human impact will remain for years. For example, the displacement and rebuilding in New Orleans after Hurricane Katrina extended for several years and altered the character of the city, an impact that still remains today," said Frank Martell, president and CEO of CoreLogic. "The reconstruction of the housing stock and infrastructure impacted by the storms should provide a small stimulus to local economies. This rebuilding will occur against a backdrop of wage growth, consumer confidence and spending in the national economy which should continue to provide a solid foundation for real estate demand in the storm-impacted areas and beyond."