Black Knight's Mortgage Monitor for November notes that the equation for tapping the growing pool of homeowner equity could shift because of the new rules governing the mortgage interest deduction (MID) in the newly passed tax law.

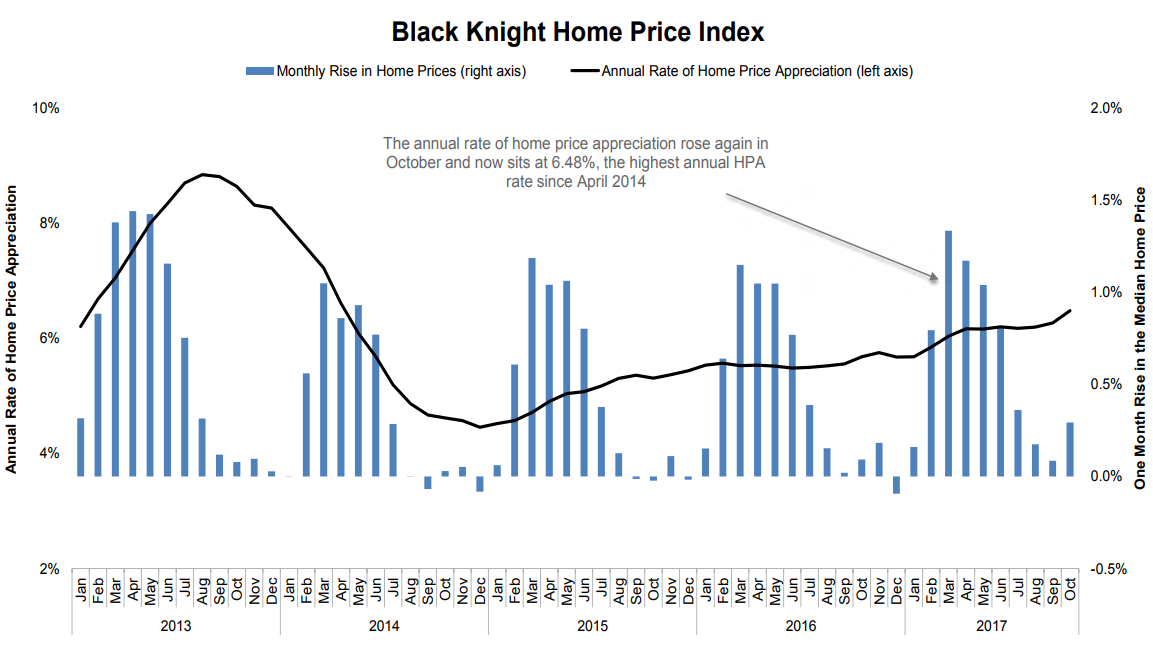

That equity continues to grow as home prices rise, with Black Knight's Home Price Index posting another increase, 0.29 percent increase in November, the strongest appreciation for any November since 2005, and an annual increase of 6.48 percent, the largest since early 2014. Black Knight's reported gain, incidentally, was the smallest of the four reported by indexes tracked by MortgageNewsDaily. The other three posted monthly gains for November ranging from 0.5 to 2.0 percent.

Black Knight said the growth rate in its annual index increased by more than 30 basis points over the three months ended in November and by more than 80 basis points from the appreciation rate (5.57 percent) at the beginning of the year. The accelerating rate has been widespread; affecting 70 percent of states in two of the last three months.

Rising prices have now pushed the number of underwater borrowers down by 800,000 or 37 percent since January of 2017. Only 2.7 percent of mortgaged homeowners, 1.36 million, are now in negative equity, the lowest since 2006. The rate of homeowners who owe more on their mortgages than their homes are worth is still elevated compared to pre-housing boom levels. This is primarily because, while 36 states and 70 percent of major metro areas have now surpassed their pre-recession home prices, 43 of the 100 largest metros are still lagging those peaks.

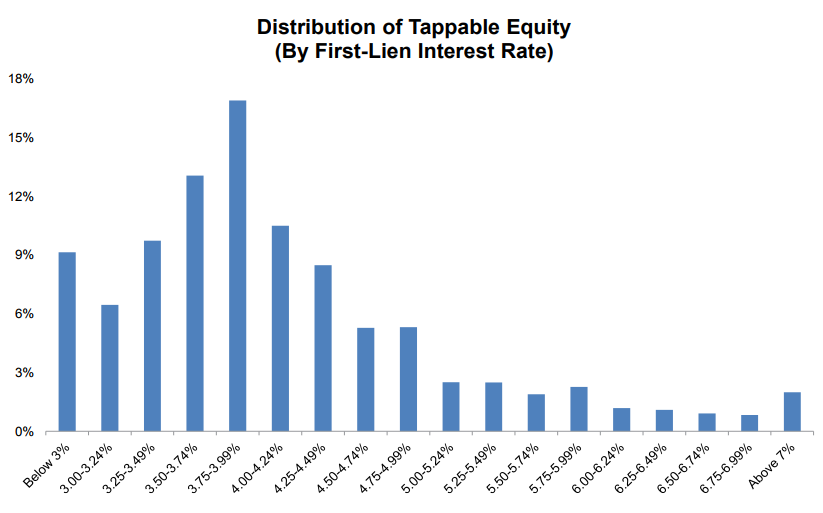

Not only do most of the nation's homeowners now have positive equity, approximately 42 million of those with a mortgage have loan-to-value ratios below 80 percent, giving them nearly $5.4 trillion in "tappable" equity. This is an increase of more than $3 trillion from the bottom of the market in early 2012.

Over half of the equity that could be cashed out by homeowner refinancing is in homes where the first lien mortgage has an interest rate below 4.0 percent, making a home equity line of credit (HELOC) an attractive option. However, as Black Knight Data & Analytics Executive Vice President Ben Graboske explained, recent changes to the U.S. tax code may have implications for homeowner decisions about using that equity.

"We've noted in the past that as interest rates rise from historic lows, HELOCs

represented an increasingly attractive option for these homeowners to access

their available equity without relinquishing interest rates below today's

prevailing rate on their first-lien mortgages," Graboske said. "However, with the recently passed tax reform

package, interest on these lines of credit will no longer be deductible, which

increases the post-tax expense of HELOCs for those who itemize. While there are

obviously multiple factors to consider when identifying which method of equity

extraction makes more financial sense for a given borrower, in many cases, for

those with high unpaid principal balances who are taking out lower line

amounts, the math still favors HELOCs. However - assuming interest on cash-out

refinances remains deductible - for low-to-moderate UPB borrowers taking out

larger amounts of equity, the post-tax math for those who will still itemize

under the increased standard deduction may now favor cash-out refinances

instead, even if the result is a slight increase to first-lien interest rates.

"As rates continue to rise and the cost associated with increasing the rate on

an entire first-lien balance rises as well, the benefit pendulum will likely

swing back toward HELOCs. Even so, the change could certainly impact HELOC

lending volumes and loan amounts in the coming months and years. To a certain

degree, the same question holds true for cash-out refinances, since tax debt

for homeowners who will no longer itemize becomes generally more expensive

without mortgage interest deduction in the equation. These refinances will

likely be an attractive source of secured debt in the future, but increased

post-tax costs may have a negative impact on originations. That said, it still

remains to be seen whether and to what extent tax costs will impact borrower

decisions in terms of either HELOCs or cash-out refinances. At this point, only

time will tell."

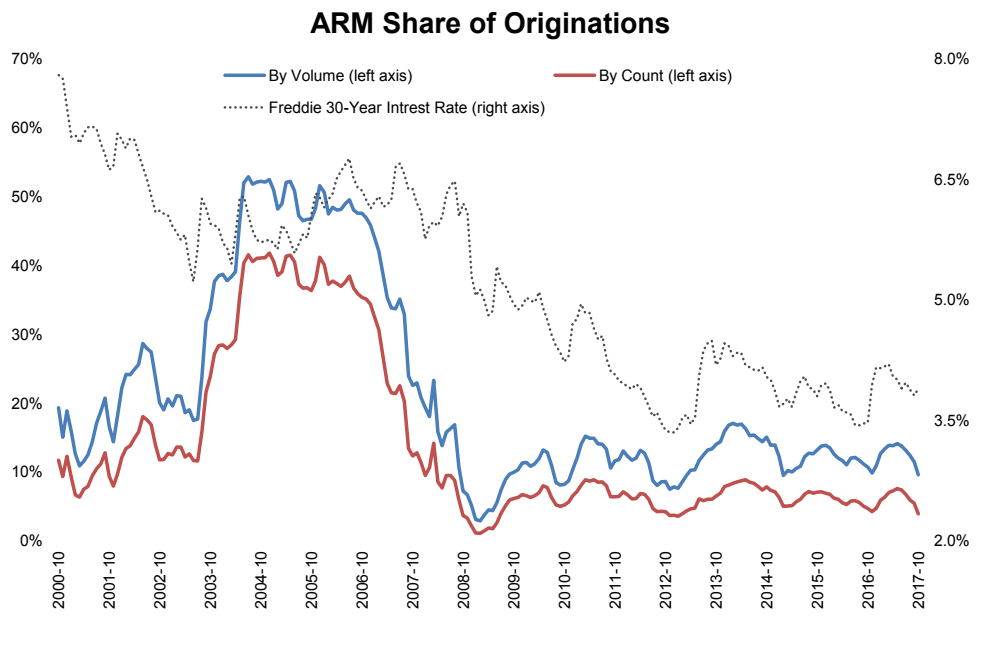

Another topic getting some scrutiny in this month's Monitor is the shrinking profile of the adjustable rate mortgage, the ARM. As interest rates dropped to historic lows, this loan product, which helped fuel the housing boom of the last decade, shrank to a low single digit share of loan originations. However, they are neither gone nor forgotten.

Black Knight points to the obvious, that there has, post-recession, been a strong correlation between interest rate movement and the ARM market share. As rates have risen in recent months, and the delta between interest rates for a 30-year fixed-rate mortgages (FRM) and a hybrid ARM increased, ARMs became more desirable; their share has risen, both for purchase and refinance loans. As rates softened in mid-to-late 2017, the ARM share declined. As of November, roughly 4 percent by count of new originations were ARMs, the lowest in nearly six years.

Not only are the numbers fewer, but ARMs being originated today are very different than those written pre-recession. The loan standards are much tighter, and the initial fixed-rate periods average a longer term as well.

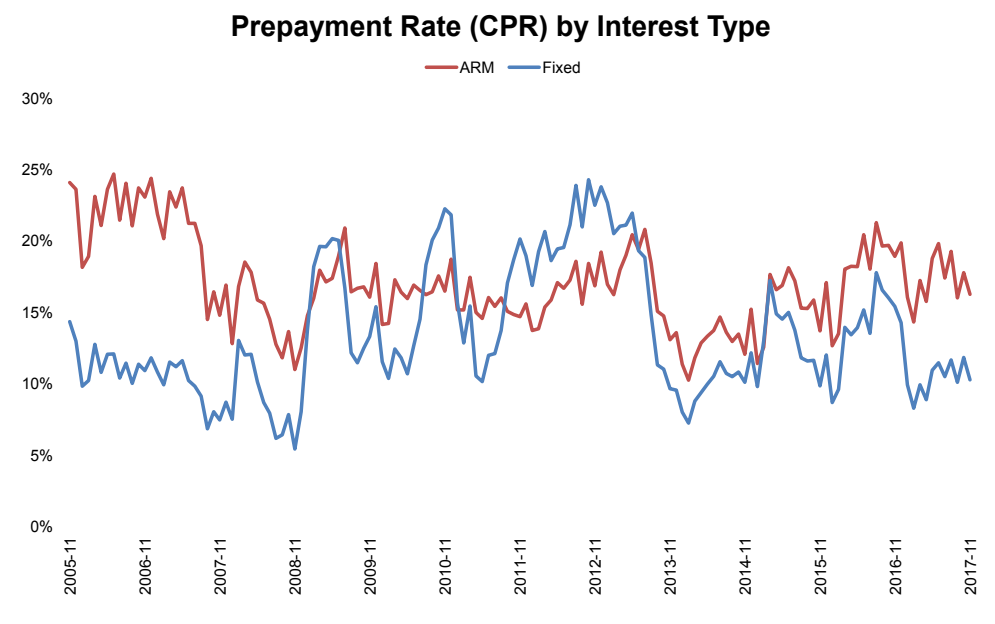

These loans are also being prepaid at a much faster rate on average than are FRM. The conditional prepayment rate has been 6.7 percentage points higher for ARMs than for FRMs. In addition, 70 percent of borrowers refinancing their ARMs are doing so with fixed rate mortgages.

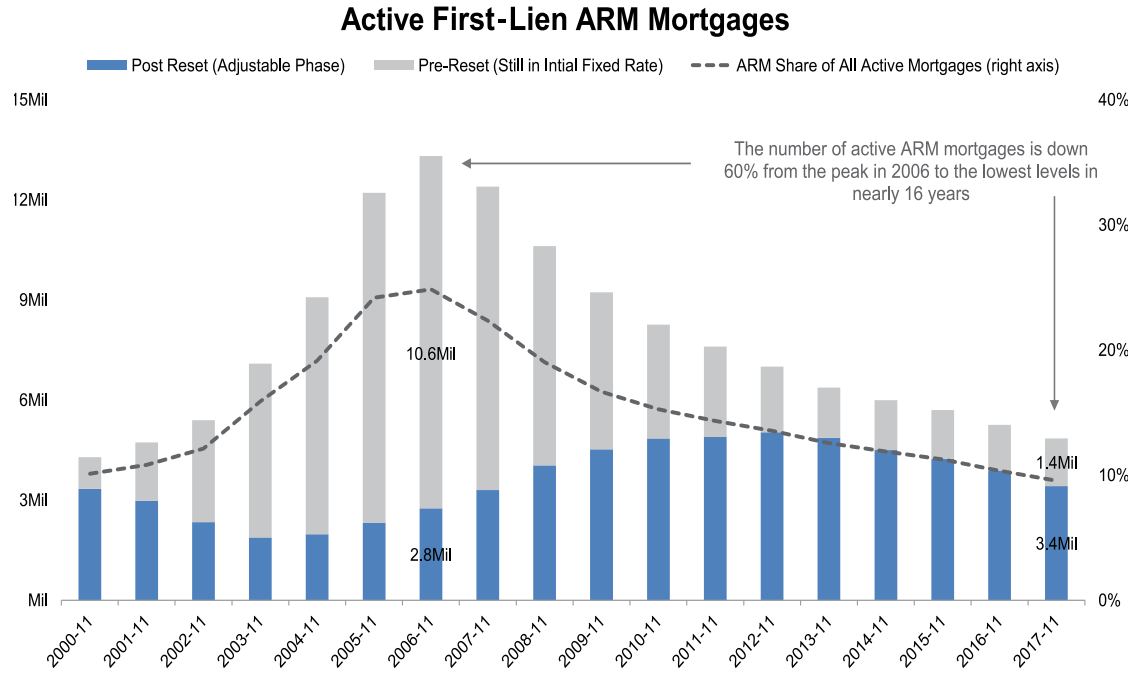

Fewer originations, faster prepays, and refinances into FRM have combined to steadily decrease the number of outstanding ARMS by 8.4 million from their 2006 peak. They now make up less than 10 percent of active loans compared to about a quarter of all loans at their peak. Today fewer than five million ARMS remain active, the fewest since 2002.

Of those loans, just 1.4 million are in their initial fixed rate period, up slightly from a year ago but way down from the 10.5 million that were in their initial stage at the pre-recession peak. Such loans are typically viewed as high risk because of the potential for large payment increases when they reset for the first time. The 3.4 million operating in their adjustable rate phase, which usually calls for annual resets, are also subject to payment shock if the indexes to which their rates are linked rise by significant amounts. Borrowers in the adjustable phase make up nearly 7 percent all homeowners with a mortgage.

Over 85 percent of ARMs are indexed to some form of the LIBOR or Treasury index, both of which have seen increases for most of the last three years with additional increases expected this year. Still, the two, both of which peaked at over 5 percent in 2005 and 2006, were below 2.5 percent at the end of 2017. An estimated 65 percent of loans in their post initial reset phase have already seen their interest rate and payments rise an average of 32 basis points over the past 12 months and nearly a half percent over the past two years. However, earlier downward adjustments have resulted in the average borrower in this group still having an interest rate well below what they received at origination. The average rate for those resetting today is 4.12 percent compared to an average original rate of 4.86 percent.

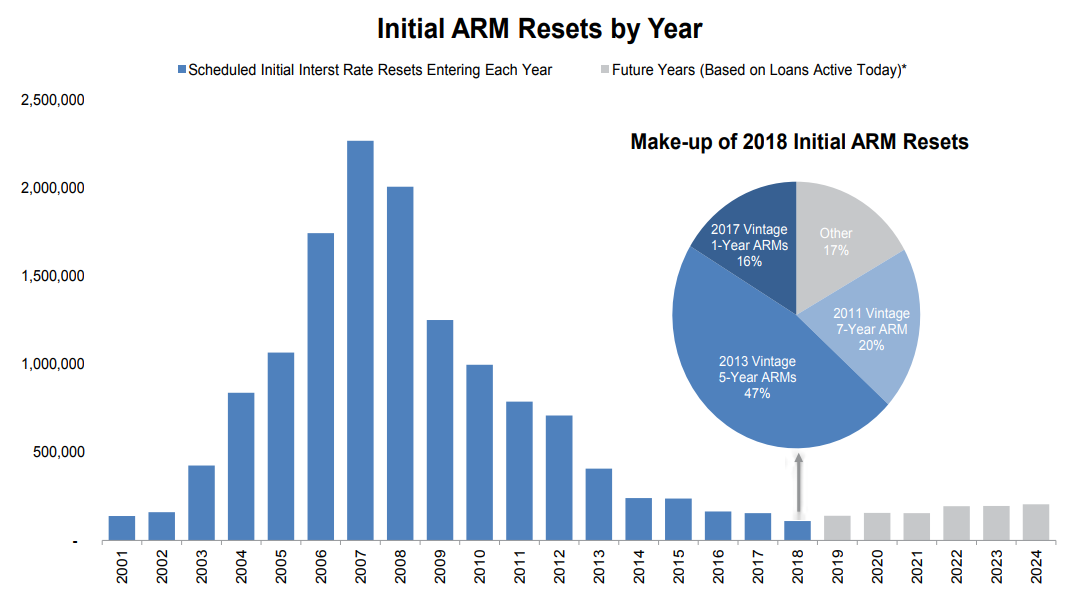

Fewer than 110,000 borrowers face initial ARM resets this year, 95 percent fewer than at the peak of reset risk in 2007. In addition, more than 90 percent of the loans resetting this year were originated in 2011, when lending standards were quite strict. In 2007 the resets came in the face of rising interest rates for over 2.2 million homeowners one of the triggers of the financial crisis.

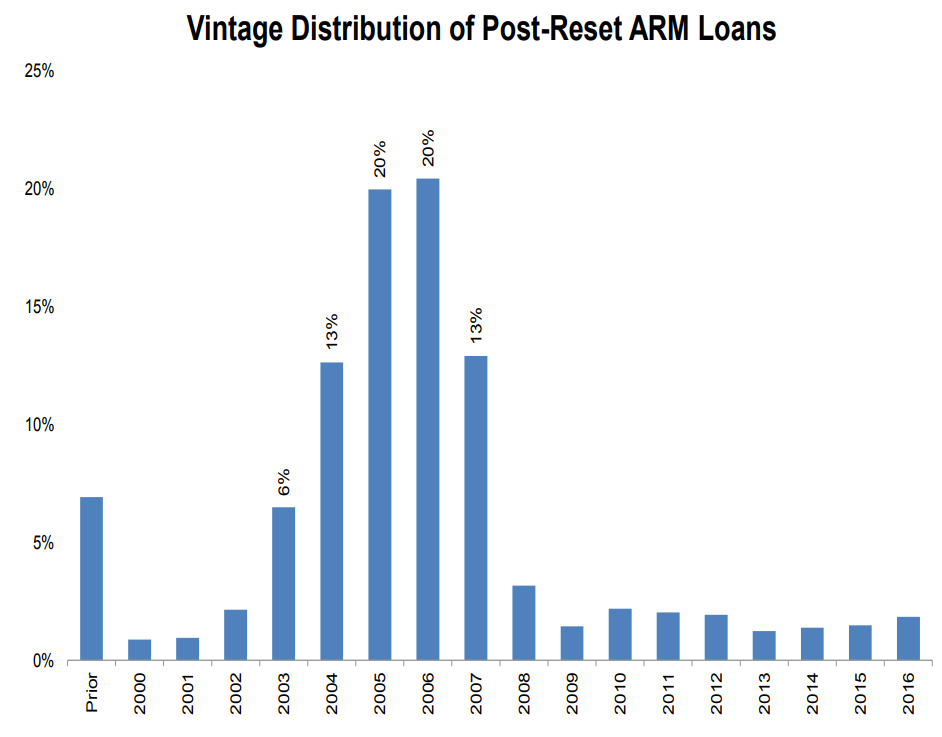

On the other hand, nearly three-quarters of active ARMS that are in their adjustable phase are of the 2003-2007 vintages, when loan standards were notoriously lax. Forty percent of active loans in their adjustable phase were originated in 2005 and 2006 alone.

Black Knight says it has found little evidence of the rising interest rates and payments in recent years "manifesting themselves in a resurgence of delinquencies; however, continued increases will result in greater payment shock pressure on these borrowers.

"While not an imminent risk to the mortgage market, this certainly bears watching given the expectation of multiple interest rate hikes by the Federal Reserve in 2018."

The Monitor also notes that mortgage delinquencies have skyrocketed in Puerto Rico in the aftermath of Hurricanes Irma and Maria. Nearly one in four mortgages on the Island has become non-current as a result of the storms, bringing the non-current rate to 37.2 percent with over 95,000 mortgages affected. Given the delinquency rate trajectories following Katrina and Harvey, Puerto Rico's may be nearing its peak. Black Knight says the territory's long-term mortgage performance will likely hinge on the speed and magnitude of investment in its recovery.