Market sentiment isn’t looking good as a new week packed with data gets underway. Perhaps the most telling data point is the 10-year Treasury note, whose yield is back under 3.00% for the first time since June 28th.

“Financial markets remain on edge following Friday’s disappointing U.S. jobs report amid heightened concerns about Europe’s credit crisis, the U.S. budget deficit and deadline to raise the debt ceiling, and hard-landing fears in China (following data showing higher-than-expected inflation and slowing import growth),” said economists at BMO Capital Markets in a morning note.

There are two decidedly different tones between this week and last. Whereas markets seemed fixated on mostly jobs in in the holiday shortened work week behind, the one ahead not only offers many scheduled economic releases but also includes FOMC Minutes, the first auction cycle since the official end of QEII, and a major Ben Bernanke speech/Q&A session. Traders are especially interested in the auction cycle as it contains the 10yr benchmark itself, the first since QE2 ended, and follows a rather horrible previous auction cycle from two week's ago. The FOMC Minutes and Bernanke's scheduled speech will also play a big role in directional gyrations as market participants look to these updates for new guidance on the Fed's official economic outlook.

A flight to quality has the 10-year Treasury yield down eight basis points at 2.946% in early trading, while the two-year yield is three basis points firmer at 0.36% and the 30-year Treasury yield is five basis points firmer at 4.24%. The Fannie Mae 4.0 MBS coupon is starting the week +9/32 at 100-26.

European contagion remains the culprit, as Reuters reports three unnamed European Officials saying an emergency meeting will be held to discuss the sharp sell-off of Italian assets on Friday.

“Peripheral Europe’s credit spreads continue to widen to euro-era highs amid growing contagion from Greece and concerns about Italy,” added BMO. “A German newspaper said that European officials are considering doubling the size of their rescue fund to cover Italy in light of recent political uncertainty and weakness in its bank shares. As well, news reports say that European leaders are now considering some form of Greek default as part of a new bailout package.”

Equity futures are showing greater losses than in Friday’s session. The S&P 500 is ready to open 17.25 points lower at 1,324.50 and the Dow looks to drop 125 points at 12,490.

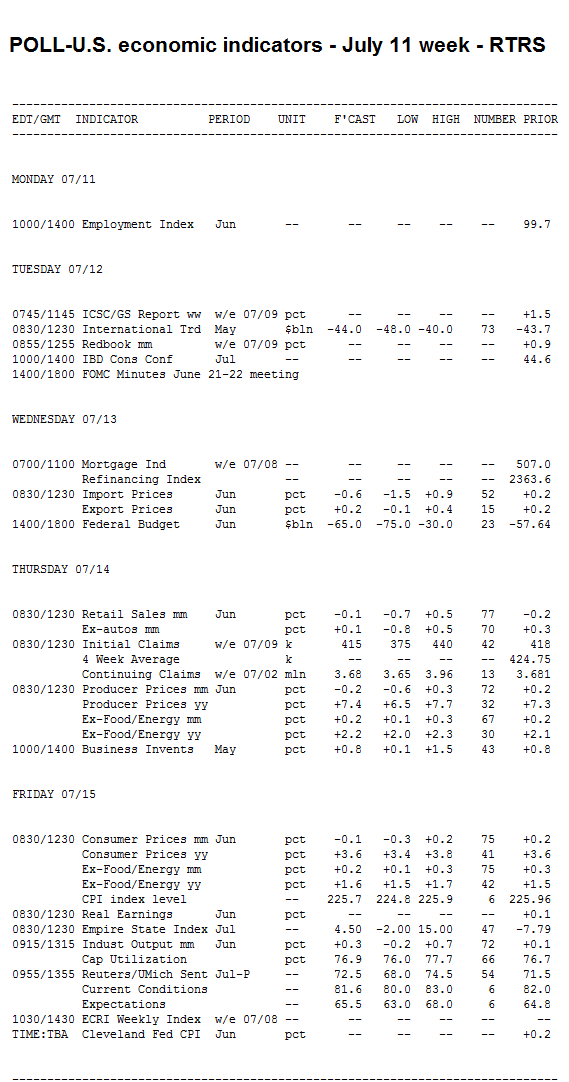

Key Events This Week:

Monday:

No significant events.

Tuesday:

8:30 ― Expect the Trade Balance to narrow once again in May. Economists are projecting a $42.7 billion deficit this month, versus a $43.7 billion gap between exports and imports in April and a $46.8 billion gap in March. Higher gas prices are thought to have limited imports in the month, while exports should recover following a temporary disruption from the March earthquake in Japan.

“The export demand, falling oil prices, and slightly higher dollar should serve to decrease the trade balance, though the movement is unlikely to be very large,” said economists at Janney Capital Markets. “At this point, however, foreign trade appears to be one of the stronger sources of economic growth for 2Q and is running roughly 8% ahead of 1Q results.”

Janney noted that US exports to the rest of the world hit a record high $175.6 billion in April, reflecting global demand for US-produced capital goods coupled with an earthquake-driven slowdown of exports out of Japan.”

1:00 ― Treasury auctions $32 billion 3-year notes

2:00 ― The FOMC Minutes from the June 21-22 meeting will be of more interest to historians than anyone toying with the markets. Comments in the monetary policy statement centered on the view that unemployment was improving and growth was picking up, observations that “will seem stale” now, according to economists at Nomura Global Economics.

“Chairman Bernanke expressed more anxiety in his press conference about ‘longer-lived factors,’ they noted. “The relatively weak economic data of late suggests that monetary policy will be on hold for even longer. We expect the minutes of the 21-22 June meeting to show the extent of policymakers' concerns about the recent weakness.”

Wednesday:

9:10 ― Eric Rosengren, president of the Boston Fed, speaks on the economic outlook.

10:00 ― Fed chairman Ben Bernanke testifies before the House Committee on Financial Services at the Semiannual Monetary Policy Report to the Congress in Washington.

Nomura notes this is Bernanke’s first appearance since his June 22 press conference.

“In the wake of the very weak June employment report, his testimony is likely to reflect heightened concerns about the ‘frustratingly slow’ labor market recovery,” they wrote “As in the last meeting in March, he will likely emphasize the importance of improving the long-term fiscal situation, and encourage the House to raise the debt ceiling. That being said, he may suggest withholding fiscal tightening in the near term.”

1:00 ― Treasury auctions $21 billion 10-year notes

1:20 ― Richard Fisher, president of the Dallas Fed, speaks on the economy.

2:00 ― June is a month that typically sees a surplus in the Treasury’s Budget Statement but this time economists look for a $60 billion deficit. According to Bloomberg, the 10-year June average is a $4.2 billion surplus, but over the last five years there’s been an average June deficit of $162 billion, including a $68.4 billion gap in June 2010.

“Treasury data show that receipts ran about flat in June compared with June 2010, while outlays were 11% higher,” said forecasters at Nomura. “Based on these data, we expect a June budget deficit of -$69.7 billion compared with -$68.4 billion in the same month last year.”

Thursday:

8:30 ― The Producer Price Index is expected to show its first negative monthly read in 12 months. June prices are expected to decline 0.3% due to falling energy prices, which are projected to fall 1.8%, led by a near-5% drop in gas prices. With food and energy prices stripped out, ‘core’ prices are anticipated to rise 0.2% in the month, the same pace as in May.

“Refined energy product prices fell sharply in June and we anticipate further declines in the next few months reflecting the drop in crude oil prices,” said economists at Citigroup. “This is likely to yield relatively low readings for headline producer prices starting in June. We expect that core PPI remained roughly on trend. However, the shortage of motor vehicles due to the supply chain disruptions should result in a temporary pickup in auto prices.”

8:30 ― Economists are predicting a flat month for Retail Sales in June, following a 0.2% cut in May and a 0.3% gain in April. After last week’s stunningly awful employment report, the risk is clearly to the downside, as reflected by the -0.3% to +0.2% range of forecasts.

“The decline mostly reflects lower vehicle sales and lower gasoline prices,” said economists at IHS Global Insight. “The autos decline reflects supply chain disruptions from Japan that have finally made their mark on American auto sales. Retail sales excluding autos are expected to decline for the first time since May 2010, thanks to lower gasoline prices which are helping consumers deal with a struggling labor market.”

“The consumer is the clear weak link in the US economic chain at present,” added economists at Janney Capital Markets. “While corporate investment continues to chug along and exports are growing, the personal consumption ― which makes up roughly 70% of all economic output ― is held hostage to weak labor market performance.”

8:30 ― Initial Jobless Claims fell 14k in the week ending July 2, beating forecasts and helping to mislead the market into an optimistic mood a day ahead of the June employment number. With 414k new claims in the report, weekly claims have now been above the 400k mark for 13 weeks. The four-week average was 424,750. For the period ending July 9, the consensus call is 405k, with a few predictions just under the 400k mark.

Economists at Citigroup aren’t in the optimistic camp, noting that as many as 20k public employees in Minnesota might have filed claims as the budget impasse persisted, while the seasonal ‘auto retooling’ period could add some volatility.

“Initial jobless claims probably rose by 12,000 during the week of Independence Day,” they wrote. “Beneficiaries likely rebounded after a quirky seasonal factor-related drop.”

10:00 ― Business Inventories are expected to grow 0.6% in May, based on the already reported figures from wholesalers and manufacturing inventories. The new data concerns retail inventories, which were likely flat or weaker due to a decline in retail and auto sales.

“Business sales will remain under pressure in May, weighed down by the 11 March Japanese earthquake and uncomfortably high input costs, which have whittled away at business sentiment,” said economists at Nomura.

10:00 ― Fed chairman Ben Bernanke testifies before the Senate Committee on Banking, Housing, and Urban Affairs at the Semiannual Monetary Policy Report to the Congress in Washington.

1:00 ― Treasury auctions $13 billion 30-year bonds

Friday:

8:30 ― Just like its cousin producer index, the Consumer Price Index is anticipated to show a monthly decline owing to falling energy prices in June. The consensus looks for a 0.2% decline, with forecasts ranging from -0.3% to flat. Core prices are forecast to rise 0.2%, which would keep the annual climb at 1.5%.

“Motorists cheered when gasoline pump prices ticked down in June, and gasoline prices in the CPI should drop around 7%,” said economists at IHS Global Insight.

“Although core CPI remains low,” Citi added, “this inflation measure has been accelerating all year. However, with the enormous slack in the economy, high profit margins, and resistant consumers, we think this bump up was mostly early-year residual seasonality. Inflation expectations remained anchored during the run-up in energy prices. And now that these prices are coming off, there is little chance that they will become unglued.”

8:30 ― The Empire State Manufacturing Index should give us an early look at how the sector is shaping up in July. Let’s hope it’s better than in June, when the report unexpectedly tumbled almost 20 points into negative territory at -7.8. The consensus this time around is +8.

“Since manufacturing activity appeared to have started to recover from supply-chain disruptions in mid-June, positive momentum will likely carries over to July's survey,” said economists at Nomura. “Therefore, we look for a 4.2 reading in July, a significant rebound from -7.79 previously.”

9:15 ― Industrial Production is anticipated to climb 0.4% in June, following a meagre 0.1% gain in May. The pickup in pace largely reflects a restoration in auto production and a rebound in utility output due to warmer weather, economists say.

“A modest, and partial, rebound in motor vehicle production is the best thing going for the industrial sector in June,” said economists at IHS Global Insight. “Industrial output has been almost flat on balance over the past two months, as motor vehicle and parts output dropped. June should see that negative go away and be replaced by a small positive, lifting both manufacturing and total production to 0.3% gains. Manufacturing outside motor vehicles looks soft based on a weak figure for hours worked in the employment report. Electricity output should be a small plus as June was a bit more unusually warm than May.”

9:55 ― Economists have resigned themselves to a weaker Consumer Sentiment report. The consensus estimate is a half-point down at 71, with forecasts ranging from 68 to 73. With so little job growth last month and a housing market scraping along the bottom, it’s difficult to see why this index would improve at all.

“Consumer news has not been very favorable,” said IHS Global Insight. “May and June payroll numbers were disappointing, household net worth is taking a beating from volatile stock markets and depressed home prices, and gasoline and food prices are still relatively high. The good news is that gasoline prices are off their peak, providing relief to strained household budgets. The fall in gasoline prices is pushing down inflationary expectations and should improve sentiment.”

CURRENT GUIDANCE: We have good news and bad news. The bad news is, the U.S. labor market isn't producing jobs quick enough to boost the broader economic recovery. This weighs on housing, especially the purchase market and home prices (possible downward spiral). The good news is, a slow economic recovery supports our outlook for lower interest rates by the end of the summer (if they could only spark a little more loan demand!). Still, while the case for our long-term outlook remains intact, until we see investors display a commitment to rally, we will be reluctant to advise floating in the short-term, especially with unfriendly volatility only a few days behind us.