The Employment Situation Report has been released.

Excerpts from the Release....

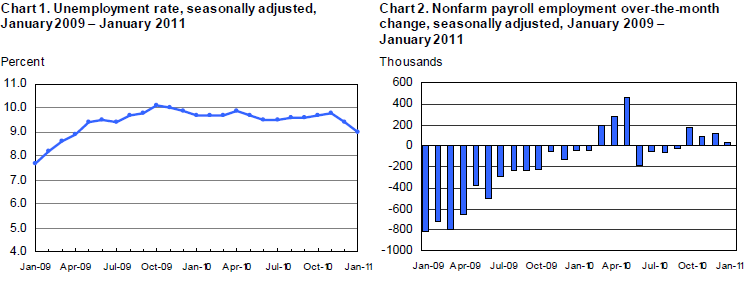

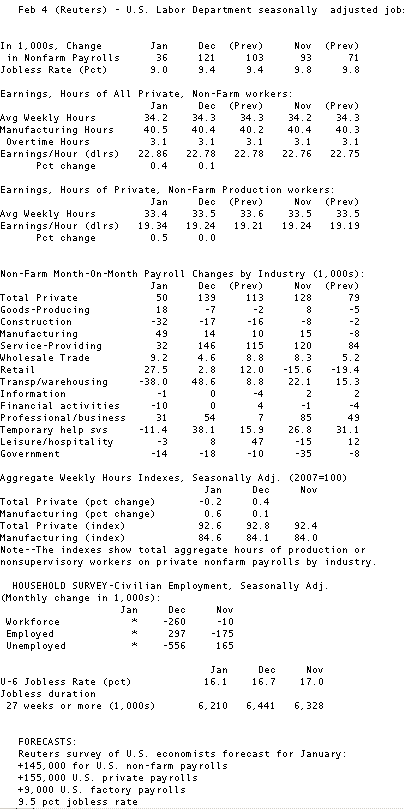

The unemployment rate fell by 0.4 percentage point to 9.0 percent in January, while nonfarm payroll employment changed little (+36,000), the U.S. Bureau of Labor Statistics reported today. Employment rose in manufacturing and in retail trade but was down in construction and in transportation and warehousing.Employment in most other major industries changed little over the month.

The average workweek for all employees on private nonfarm payrolls fell by 0.1 hour to 34.2 hours in January. The manufacturing workweek for all employees rose by 0.1 hour to 40.5 hours, while factory

overtime remained at 3.1 hours. The average workweek for production and nonsupervisory employees on private nonfarm payrolls declined by 0.1 hour to 33.4 hours; the workweek fell by 1.0 hour in

construction, likely reflecting severe winter weather.

In January, average hourly earnings for all employees on private nonfarm payrolls increased by 8 cents, or 0.4 percent, to $22.86. Over the past 12 months, average hourly earnings have increased by

1.9 percent. In January, average hourly earnings of private-sector production and nonsupervisory employees rose by 10 cents, or 0.5 percent, to $19.34.

The change in total nonfarm payroll employment for November was revised from +71,000 to +93,000, and the change for December was revised from +103,000 to +121,000. Monthly revisions result from

additional sample reports and the monthly recalculation of seasonal factors. The annual benchmark process also contributed to these revisions.

Reuters Quick Recap...

RTRS-U.S. JAN NONFARM PAYROLLS +36,000 (CONSENSUS +145,000) VS DEC +121,000 (PREV +103,000), NOV +93,000 (PREV +71,000)

RTRS-US JAN PRIVATE SECTOR JOBS +50,000 (CONS +155,000), DEC +139,000 (PREV +113,000)

RTRS-U.S. JAN GOVERNMENT JOBS -14,000 VS DEC -18,000 (PREV -10,000)

RTRS-U.S. JAN JOBLESS RATE 9.0 PCT (CONSENSUS 9.5 PCT) VS DEC 9.4 PCT (PREV 9.4 PCT)

RTRS-U.S. JAN AVERAGE HOURLY EARNINGS ALL PRIVATE WORKERS +0.4 PCT (CONS +0.2 PCT) VS DEC +0.1 PCT (PREV +0.1), TO $22.86 VS DEC $22.78; JAN YEAR-ON-YEAR EARNINGS +1.9 PCT

RTRS-U.S. JAN AVERAGE WORKWK ALL PRIVATE WORKERS 34.2 HRS (CONS 34.3 PCT) VS DEC 34.3 HRS (PREV 34.3), FACTORY 40.5 VS 40.4, FACTORY OVERTIME 3.1 VS 3.1

RTRS-U.S. JAN FACTORY JOBS +49,000 (CONS. +9,000) VS DEC +14,000 (PREV +10,000)

RTRS-U.S. JAN GOODS-PRODUCING JOBS +18,000, CONSTRUCTION -32,000, PRIVATE SERVICE-PROVIDING JOBS +32,000, RETAIL +28,000

RTRS-U.S. JAN AGGREGATE WEEKLY HOURS INDEX FOR ALL PRIVATE WORKERS -0.2 PCT VS DEC +0.4 PCT

RTRS-ANNUAL REVISION CUTS 378,000 JOBS FROM MARCH 2010 NON-SEASONALLY ADJUSTED LEVEL VS. EARLY OCT. ESTIMATE OF -366,000

RTRS-ANNUAL REVISION CUTS 411,000 JOBS FROM MARCH 2010 LEVEL ON A SEASONALLY ADJUSTED BASIS

RTRS-U.S. JOB GAINS FROM APRIL-DEC 2010 A CUMULATIVE 72,000 LESS THAN PREVIOUSLY ESTIMATED

RTRS-U.S. JAN JOBLESS RATE LOWEST SINCE APRIL 2009; GAIN IN FACTORY JOBS LARGEST SINCE AUG 1998

RTRS-U.S. JAN CONSTRUCTION JOBS DECLINE MAY HAVE BEEN CAUSED BY SEVERE WEATHER

RTRS-U.S. JAN COURIER/MESSENGER JOBS -45,000

RTRS-TABLE-U.S. Jan nonfarm payrolls rise by 36,000

The unemployment rate fell 0.4% to 9.0% vs. expectations for a read of 9.5%. This was almost entirely a factor of a shrinking labor force. Some will say the labor force is shrinking because workers are discouraged. Others will say the weather impacted the size of the labor force. The data was also distorted by a statistical adjustment in the Household Survey. The BLS implemented a population adjustment that decreased the estimated size of the civilian noninstitutional population in December by 347,000, the civilian labor force by 504,000, and employment by 472,000.

On top of that a Labor Department official says 886,000 people were unable to work because of the weather.

On top of that there is a statistical adjustment that account for the unavoidable lag between the time it takes for a new/dying business to appear/disappear from the sample frame of the Non-Farm Payrolls portion of the report. This month the birth/death adjustment reduced non-seasonlly adjusted payrolls by 339,000 in January. It should be noted that January generally has a relatively large negative adjustment factor. Birth/death factors are a component of the not seasonally adjusted estimate and therefore are not directly comparable to the seasonally adjusted monthly payroll changes. Instead, the birth/death factor should be assessed in the context of its effect on the not seasonally adjusted estimate.

Plain and Simple: NOISE NOISE NOISE. It's pretty hard to get a clear read on the health of the labor market with this much distortion in the data. There is a clear trend though, job creation isn't shooting the moon but payrolls are no longer contracting. This is a major positive. The worst case economic environment appears to have been avoided...now we deal with the long-slow-segmented-seasonal recovery process.

Last month I explained in great detail the difference between the Household Survey and the Establishment Survey and why it matters to the bond market. It's a must read: Two-Headed Labor Market Presents Problem for Bond Investors

UGH. WHAT A HEADACHE

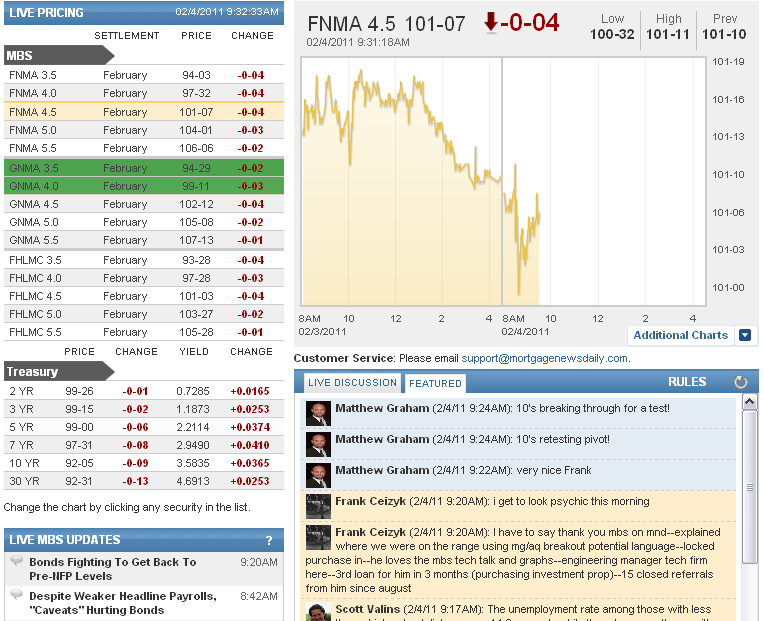

Market Reaction? Technicals win out. The BEAR FLAG is evolving as expected. Rates are higher. We explained the bear flag formation in this post...Potential Range Breakers: State of the Union Address & FOMC Meeting

Here are current levels...

The MBSonMND live discussion board is unhappy about asterisks, caveats, and "yeh but's".