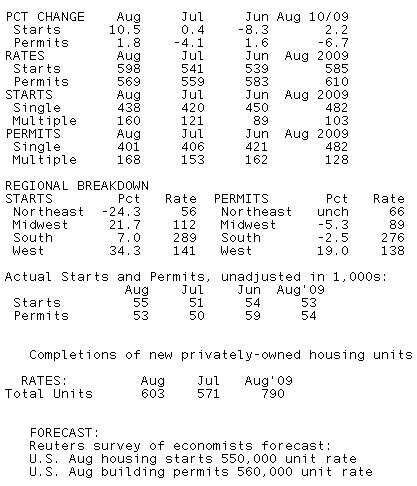

Housing Starts improved 10.5% in August, again on the back of the multi-family market, which rose by 39,000 annualized units or 32%. Single-family starts grew by 18,000 or 4.3% in August. Building Permits moved 5.6% higher with single-family permits actually declining by 5,000 units while mutlifamily permits rose by 15,000 annualized units.

Here is a recap of the better than expected data...

08:30 21Sep10 RTRS-US AUG HOUSING STARTS +10.5 PCT VS JULY +0.4 PCT (PREV +1.7 PCT)

08:30 21Sep10 RTRS-US AUG HOUSING STARTS 598,000 UNIT RATE (CONSENSUS 550,000) VS JULY 541,000 (PREV 546,000)

08:30 21Sep10 RTRS-US AUG HOUSING PERMITS +1.8 PCT VS JULY -4.1 PCT (PREV -4.1 PCT)

08:30 21Sep10 RTRS-US AUG PERMITS 569,000 UNIT RATE (CONSENSUS 560,000) VS JULY 559,000 (PREV 559,000)

08:30 21Sep10 RTRS-US AUG HOUSING COMPLETIONS +5.6 PCT TO 603,000 UNIT RATE VS JULY 571,000

08:30 21Sep10 RTRS-US AUG HOUSING STARTS RISE LARGEST SINCE NOV 2009 (+11.3 PCT)

08:30 21Sep10 RTRS-TABLE-U.S. Aug housing starts rose 10.5 pct

Market Reaction...

TSYs could care less as the potential for further quantitative easing looms over the bond market. If the FOMC does not announce/hint at more QE...expect bonds to sell, especially rate sheet influential TSYs. This implies 10s could retest the outer limits of our range at 2.85% sometime in the near future. The 10-year TSY note is currently bid +8/32 at 99-18 yielding 2.675%. The short base is clamoring for 2:15pm.

Our Fibonacci Fan continues to provide technical guidance...

MBS price levels are stable and yield spreads are nominally wider after the data as TSYs maintain overnight "progress", which occurred in very light trading volume. The November FNCL 4.0 is currently bid +0-06 at 102-12. I've got the production coupon marked at 3.645%.

Notice we've broken out of the downtrend. FNCL 4.0s are now testing the 102-10 pivot.

S&P futures went from 1134 to 1139. Equity futures seem ready to rally through 1140. If the Fed doesn't hint at further QE, the stock lever should reattach at 2:15 this afternoon, which would drive benchmark yields higher. Yes that means I feel the potential for QE has sheltered bonds from the recent stock market rally.

I expect the Fed to say something along the lines of "we remain at the ready to act just in case the poo hits the fan", which is essentially the same thing they've been saying all along.