Stocks completed their fourth consecutive week of rallies last Friday while interest rates continued to chop around an originator friendly range. The last trading week of the 3rd quarter doesn't offer a great deal of new data but Federal Reserve Bank Presidents will be out and about sharing their perspective with the market after the FOMC hinted at another Quantitative Easing program. Besides upcoming Fedspeak, bond traders are focused on pending government and corporate debt supply issuance.

Key Events in the Week Ahead...

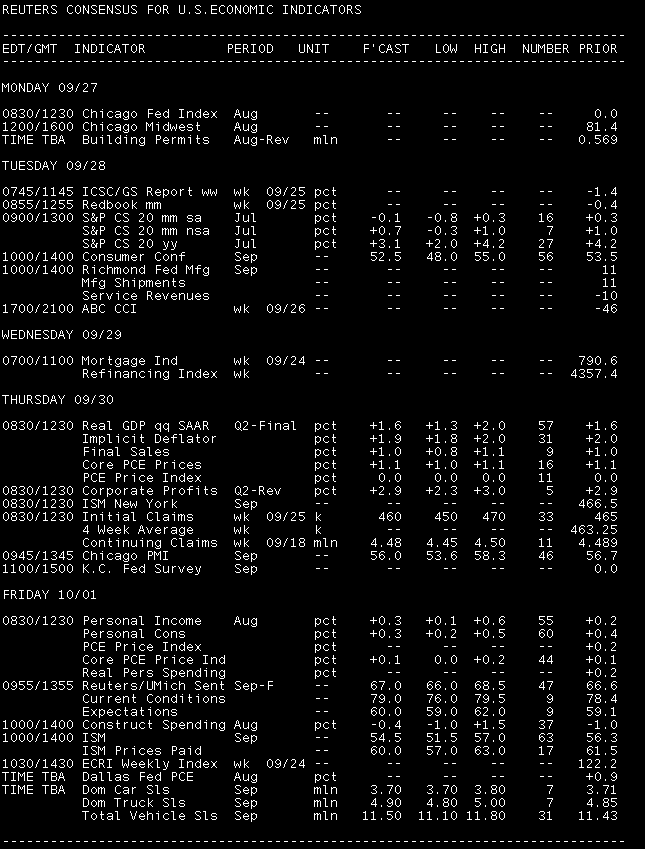

Monday:

No significant data.

Treasury Auctions:

- 11:30 ― 3-Month Bills

- 11:30 ― 6-Month Bills

- 1:00 ― 2-Year Notes

Tuesday:

9:00 ― The S&P Case-Shiller Home Price Index is expected to show that prices are up 3.2% in July compared to the prior year, according to Thomson Reuters, which notes that home prices fell 32% between 2006 and 2009. Prices have risen in each of the previous three months, pushing the index up 4.4% in the second quarter. But the increase is set to decelerate given recent weakness in the housing market.

“Already-available house price data for the month point to a significant downshift,” said economists at Nomura, who look for a +2.5% year-over-year change. “The Loan Performance index fell by 0.6% m-o-m, the FHFA index by 0.7% and the existing home median price index by 0.1%.”

10:00 ― Economists believe Consumer Confidence will take a dip in September, falling to 52.0 after the index increased 2.5 points to 53.5 in August. Consumers remains pessimistic about future business conditions and the unemployment rate remains near 10%.

Analysts at BBVA point out that this consumer confidence index decreased from 111.2 in February 2007 to its historical low of 25.3 in February 2009. They expect the index to be flat this month.

Economists at Deutsche Bank are more optimistic, citing recent gains in the stock market.

“The monthly change in consumer confidence has shown a significant correlation with the equity market (60%) over the past five years,” they said. “Thus we expect a slight increase in the index to 54.0 vs. 53.5 in August.”

4:30 ― Federal Reserve Board Governor Kevin Warsh participates in NYSE Panel on the Role of Capital Markets in Job Creation. Audience Q&A expected.

5:30 ― Federal Reserve Bank of Atlanta President Dennis Lockhart gives speech on the economy at Sewanee University. Audience Q&A expected, Media Q&A TBD.

Treasury Auctions:

- 11:30 ― 4-Week Bills

- 1:00 ― 5-Year Notes

Wednesday:

7:00 ― The weekly MBA Mortgage Applications index continues to point towards weak purchases despite extremely low mortgage rates. Refinancings remain strong although they have declined for the past three weeks.

“Mortgage purchase applications have been stable over the past month but remain at an extremely depressed level,” said economists at Nomura. “The lack of recovery in applications suggests home sales are likely to remain subdued over the near term.”

10:15 ― Federal Reserve Bank of Minneapolis President Narayana Kocherlakota speaks on "Economic Outlook and the Current Tools of Monetary Policy" at an European Economics & Financial Centre Distinguished Speakers Seminar. Audience Q&A expected. No media Q&A.

12:30 ― Charles Plosser, president of the Philadelphia Fed, speaks on unwinding monetary stimulus to the Greater Vineland Chamber of Commerce in Vineland, New Jersey. Audience and media Q&As expected

5:15 ― Federal Reserve Bank of Boston President Eric Rosengren speaks before the Forecasters Club of New York. Speech topic TBA. NOTE: Reporters permitted to attend speech portion of appearance only.

Treasury Auctions:

- 1:00 ― 7-Year Notes

Thursday:

8:30 ― The second or final revision to second-quarter GDP report is expected to remain unchanged at +1.6%, after being downgraded from +2.6% in the prior revision. Estimates from economists range from +1.3% to +1.7%. Construction spending is expected to be trimmed in the quarter, but inventory build-up and consumer spending on services was larger than earlier estimates. At this point, however, economists are more concerned with third-quarter growth, which is expected to be in a similar range.

“Based on the latest data, in 2Q10 personal consumption expenditure (PCE) increased by 2.0% which is the highest growth rate since 1Q07,” said economists at BBVA. “However, we keep our baseline scenario of low PCE growth due to ongoing household deleveraging process, increased uncertainty in the economy and high unemployment rates. The market will be waiting for the BEA’s preliminary estimate for 3Q10 which will be released on October 29.”

8:30 ― Initial Jobless Claims continue to come in higher than predictions. Weekly claims have averaged 458k so far in September, or 8k above the level indicating labor growth in the economy. In August, weekly claims averaged 487k. Last weeks survey saw claims rise 12k, and for the week ending Sept. 25 economists only expect a slight dtip to 459k.

“We expect claims to remain around the 460,000 level for the next few weeks,” said economists at Nomura.

9:45 ― The Chicago PMI, or Business Barometer, is an index covering services and manufacturing activity in the Midwest. The index has been reporting well above the break-even 50-point in recent months, though in August it fell to 56.7 from 62.3. This month the index is anticipated to continue decelerating to 56.0.

“With overwhelming evidence that the economy has slowed, we believe this indicator will also be moving lower,” said economists at Nomura. “However, the Chicago NAPM saw a sizable decline in August, and we therefore think the move lower in the September report will be more modest. We forecast the index will fall to 56.0 from 56.7 previously.”

10:00 ― The Senate Banking Committee holds a hearing to discuss the Implementation of the Dodd-Frank Wall Street Reform and Consumer Protection Act. Witnesses include: The Honorable Neal S. Wolin, Deputy Secretary, U.S. Department of the Treasury; The Honorable Ben S. Bernanke, Chairman, Board of Governors of the Federal Reserve System; The Honorable Sheila Bair, Chairman, Federal Deposit Insurance Corporation; The Honorable Mary Schapiro, Chairman, U.S. Securities and Exchange Commission; The Honorable Gary Gensler, Chairman, Commodity Futures Trading Commission; and Mr. John Walsh, Acting Comptroller of the Currency, Office of the Comptroller of the Currency.

6:00 ― Federal Reserve Bank of Cleveland President Sandra Pianalto participates in "Vital Economic Issues Confronting the New Congress" panel discussion of the Women's Economic Round Table of the Knight-Bagehot Program in Economics Business Journalism. Q&A from panel moderator.

Friday:

8:30 ― Personal Income & Outlays report for August is expected to show income rise 0.3% following 0.2% in July and a flat reading in June. Spending is expected to advance 0.4% for the second month in a row after a flat reading in June. Inflation is set to remain tame with a 0.1% uptick, compared with a 0.2% increase a month before and a 0.1% decline in June.

“Personal income has rebounded steadily since last year and is now up 3.0% annualized year-to-date,” said economists at Deutsche Bank. “This trend should continue as long as the labor market continues to improve. … Particular attention should be paid to the core PCE deflator, which is up 1.4% over the past 12 months and which will hold steady at 1.4% if our August forecast is correct. Still, the Fed is likely to worry about further disinflation.”

8:30 ― William Dudley, president of the New York Fed, speaks to the Society of American Business Editors and Writers in New York.

9:55 ― The preliminary Consumer Sentiment report surprised some by shedding 2.1 points to 66.6 earlier this month. The decline was mostly related to a downfall in the expectations component. The fuller reading is expected to produce similar results with the median estimate at 67.0.

“The various sentiment indices have been roughly stable for the past few months. We expect this trend to continue for the time being,” said economists at Nomura. “Important to watch in this report will be the two measures of inflation expectations, given concerns about possible deflation.”

10:00 ― The ISM Manufacturing Index beat expectations in August by improving nearly a point to 56.3, reversing three months of slowdown and producing a score well above the 50-level indicating growth. The index has remained above 50 for the previous 12 months and September should be no exception, although some pullback is expected with the median estimate at 54.5. Predictions ranging from 53.0 to 55.5. This would indicate that manufacturing continues to expand but the pace is decelerating.

“In light of the ongoing moderation of ISM new orders over the past three months, we anticipate an additional decline in the headline (54.0 vs. 56.3),” said economists at Deutsche Bank. “We will also focus on the employment series which hit a 27-year high last month. The August ISM survey was one of the catalysts for the recent recovery in equities.”

10:00 ― Construction Spending is anticipated to decline 0.4% in August, a smaller drop than the 1% fall in July or the 0.8% decrease in June. Economists say the decrease will be led by weakness in private residential building, as indicated by recent housing starts data.

“Single-family construction will be a big negative, dropping as much as 4%, based on recent declines in single-family housing starts,” said economists at IHS Global Insight. “We are projecting a 1% drop in nonresidential construction. The bigger question about this category is whether we will see another sizable downward revision for the prior three months. Although public construction dropped in July, we are expecting, at worst, a flat reading for August, since infrastructure spending is still holding up the numbers.”

4:00 ―Federal Reserve Bank of Dallas President Richard Fisher speaks on "Globalization, Economic Recovery and Monetary Policy" before the Vancouver Board of Trade Distinguished Speaker Series. Audience Q&A expected. Media Q&A TBD.

The Full Economics Calendar...