Both fixed income and equity markets are worse off to start the week.

The cause of uncertainty is a strange one - IMF chief Dominique Strauss-Kahn was arrested in New York over sexual assault charges on the weekend. "The IMF has been a key player in helping Europe manage the crisis, and while Strauss-Kahn is only one man, markets don't like uncertainty," said economists at BMO Capital Markets. "The euro weakened on the initial reports of the arrest, but has since rebounded, and is little changed from Friday's close."

Meanwhile, the U.S. government is expected to hit the $14.294 trillion debt ceiling Monday, according to the Wall Street Journal.

"The Treasury Department plans to announce Monday it will stop issuing and reinvesting government securities in certain government pension plans, part of a series of steps designed to delay a default until Aug. 2," the WSJ says, noting that hitting the limit could set in motion "an uncertain, 11-week political scramble to avoid a default."

In bonds the benchmark 10 year note is -4/32 at 99-16 yielding 3.182%. The 2s/10s yield curve is 2bps steeper at 265bps wide. The FNCL 4.5 MBS coupon is -3/32 at 103-06.

In stocks, S&P futures are -4.25 (-0.32%) at 1329.75 and Dow futures are -36 points (-0.29%) to 12,520.

Oil is -0.87% at $98.78 and gold is +0.03% at $1,494.10.

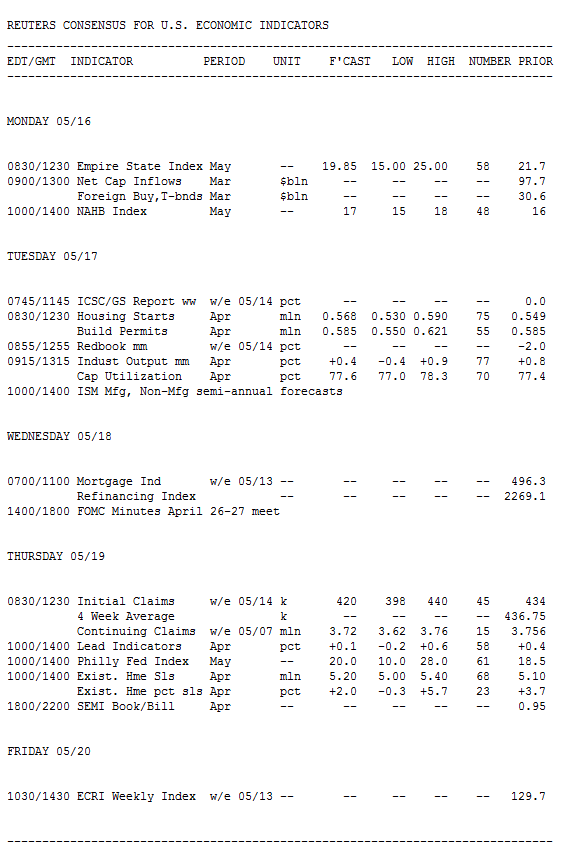

Key Events This Week:

Monday:

8:30 - The Empire State Manufacturing Index is anticipated to keep up robust levels of growth in May. Economists look for a score of 20, marking a slowdown from the 21.7 reported last month but in line with recent strength, regionally and nationally.

Economists at BBVA expect the index to report that more manufacturers consider business conditions to be improving.

"The index is one of the first regional indices to be released for May and will give valuable information about economic activity in the manufacturing sector," they wrote. "We expect that economic activity in 2Q11 will be stronger than in the first quarter."

Two components to watch closely are prices paid - which hit their highest since August 2008 last month - and employment, which rose to its highest since May 2004.

The forecasting team at Nomura Global Economics says higher commodity prices and supply chain effects from Japan "do not appear to be weighing too heavily on businesses outlooks." They note that manufacturing firms should indicate a better ability to pass on higher prices, while in the next few months they expect the recent slide in commodity prices to ease pressure.

9:00 - Federal Reserve Chairman Ben Bernanke speaks on "Innovation, Research and Development: The Government's Role" before the "New Building Blocks for Jobs and Economic Growth: Intangible Assets as Sources of Increased Productivity and Enterprise Value" event co-sponsored by the Organization for Economic Cooperation and Development. No Q&A.

10:00 - Don't expect much from the NAHB's Housing Market Index, a measure of homebuilder sentiment. The index fell one point to 16 last month, and economists predict a return to 17 this month. Considering that 50 represents growth, these tiny movements can be safely ignored.

"Tight lending standards for mortgages and expectations of a further declines in house prices are keeping housing activity subdued," Nomura economists wrote. "The NAHB index declined to 16 in April from 17; we expect a modest retrace back to 17 with the May report. "

Treasury Auctions:

11:30 - 3-Month Bills

11:30 -6-Month Bills

Monday is Class C Notification Day in the TBA MBS Market. Class C coupons are comprised of 30-yr Ginnie Mae MBS.

Tuesday:

8:30 - The pace of Housing Starts has been scraping along the bottom for the past two years. The annual pace is anticipated to rise to 570k in April, up from 549k the month before and 512k the month before, but still well below a long-term average of 1.4 million. Forecasts range widely this month, from 500k to 600k, on account of weather playing a key role.

"April housing starts likely showed signs of extending the March rebound from the severe late winter storms," wrote analysts at Citigroup, who expect single-family units to lead the recovery. "Building permits have been above starts for the past few months, suggesting a backlog of building waiting for better weather for actual ground breaking."

More broadly, Citi says there are few signs of fundamental improvement in the new home market.

A more positive outlook came from Janney Capital Markets.

"As the economic data season turns from winter to spring, we're apt to see increases in residential construction over and above those that will be weeded out by the usual seasonal adjustments," they wrote. "Residential construction has become super-seasonal, an impact of the absolute low level of sales and the lag of the seasonal-adjustment-adjustment process."

However, they noted the weather situation in April was complication, consumer income growth has stagnated, and distressed homes continue to glut the market.

9:15 - After a solid 0.8% gain in March, Industrial Production is only expected to rise 0.4% in April. Uncertainty is high - the culprit is the mid-March earthquake-tsunami and subsequent production shutdown in Japan, which hurt the auto sector.

"Motor vehicle production tumbled in April because of shockwaves to the supply chain following the March earthquake in Japan, leading to reduced hours at plants reliant on parts from Japan," said economists at IHS Global Insight.

"We estimate that unit production in the U.S. fell 12.2% from March," they added. "Motor vehicle plants would have been humming save for the supply shock, as vehicle sales have remained strong. The downdraft from autos comes amidst a decent, but uninspiring, month in most other manufacturing industries, after several very good months. A workmanlike month for most sectors combined with a drop in automotive output should yield either flat or slightly declining manufacturing output."

As of March, industrial production was 5.9% higher than one year ago. The index has also increased in 20 of the past 21 months, according to BBVA.

Treasury Auctions:

11:30 - 4-Week Bills

Wednesday:

2:00 - Minutes from the Federal Reserve's Open Market Committee may pack less punch this usual this time around, as Fed chairman Ben Bernanke delivered his first press conference within hours of the last monetary policy update.

That address "provided insight into the details of the meeting much earlier than usual," according to economists at Nomura. "In particular, the much-awaited updates of the FOMC members' quarterly forecasts were released at the time of the press conference."

Nomura does expect the minutes to provide more discussion of inflation, and perhaps more talk on the Fed's eventual exit strategy from current policies.

7:00pm - James Bullard, president of the St. Louis Fed, speaks to the Money Marketeers in New York.

Thursday:

8:30 - Initial Jobless Claims have come in above the 400k mark the past five consecutive weeks and despite a 44k drop to 434k in the first week of May, the four-week average actually increased to 436,750. The data is at odds with the latest payroll results, so economists at watching the numbers closely to determine if there are underlying problems in the market or if claims are elevated due to seasonal and regional mishaps.

"Throughout April and into May, a series of special factors boosted the figure, making the underlying trend difficult to decipher," said analysts at Citigroup. "We will be monitoring alternative measures of employment to determine if the rise in jobless claims is a true signal of emerging labor market weakness. Separately, the number of beneficiaries was virtually unchanged during its reference week, keeping the insured unemployment rate at 3.0%."

10:00 - Existing Home Sales are on the mend as investors and first-time homebuyers take advantage of median prices that are nearly 6% cheaper than one year ago. Investors bought 22% of all homes sold in March, helping the annual pace of sales tick up to 5.1 million from 4.92 million a month before. The April report is anticipated to see further improvement to 5.2 million, with estimates ranging from 5 to 5.35 million.

"We are projecting that existing home sales will rise in April, based on the 5% increase in the Pending Home Sales Index in March," said the forecasting team at IHS Global Insight. "Demand for homes picked up in March and April as buyers attempted to avoid higher insurance premiums imposed on FHA loans on April 18. This surge will result in higher closings in April, and possibly also in May, followed by a sharp drop off."

10:00 - Forecasts for the Philadelphia Fed Index are surprisingly wide, but a look at the recent numbers shows why. The report last posted a score of 18.5; on its own that looks stable, but it was actually a massive drop from a previous 43.4 - a 27-year high. The "consensus" this month is 18, but forecasts range from 10 to 28.

"We did not understand the big rise so the drop off did not come as a surprise," said analysts at Citi. "Since we see the lower April reading as representative of underlying activity, we do not anticipate much change in May."

"We expect a rebound of 6.5 points in the Philly Fed index to 25 in May," said economists at Nomura. "The months of record high manufacturing indices may have passed, but manufacturing remains a source of economic vitality in 2011. Even if regional surveys moderate, they are likely to signal continuing growth in manufacturing in the months ahead."

10:00 - Leading Economic Indicators, a composite of forward-looking data that seeks to track turning points in the economy, is anticipated to post a meagre 0.1% uptick in April. This follows gains of 0.6% and 1% in the prior two months. The recent jump in jobless claims is one reason the LEI should slow down, alongside declining vendor performance (as reported in the ISM manufacturing index).

Economists at Citi look for the LEI to fall 0.1% in the month - the last negative reading was June 2010.

"Permit issuance softened, the factory workweek shortened and new orders gauges declined," Citi wrote, noting six of the 10 categories fell recently. "Consumer expectations and financial market indicators probably were the only positive contributors. Away from the outsized contribution from the yield curve, the index would have fallen by 0.4%."

11:00 - Treasury announces the terms of 2-yr, 5-yr, and 7-yr debt supply to be auctioned in the following week.

Treasury Auctions:

2:00 - 10-Year TIPS

Friday:

No significant data.

Here is MND's latest guidance to home loan consumers...

CURRENT GUIDANCE: With the full week's worth of lender rate sheet information available on our chart, it's plain to see why we continue to express a bias toward locking. While there is a possibility that we've merely stalled and gone sideways before rates and costs improve further, it is not the highest probability result in the next week. It's more likely that costs will move higher. Whether that occurs temporarily or permanently is less certain, but as you can see in early March in today's chart, costs still worsened before ultimately improving on the last major occasion before we hit a similar wall. From a risk/reward standpoint, the decision is clear for shorter term outlooks. Lock 'em up. For those inclined to float or have no other choice, the possibility for an intermediate to longer term rates rally remains on the table. READ MORE: Margin Squeeze Hits Headlines. False Start Baked into Bonds .