Despite the 3.2 percent annualized growth in the GDP in the third quarter, Fannie Mae's economists expect the full-years growth to moderate to less than 2 percent this quarter, finishing at 1.8 percent growth for the year. In the company's December Economic Development summary its Economic and Strategic Research Group (ESR) said their forecast does not include the effects of any new federal policies "due to considerable uncertainty about the President-elect's policy agenda and the extent of support he will receive from the new Congress.

The report acknowledges the significant increase in long term interest rates over the preceding month with the 10-year T-bill touching 2.6 percent, the highest rate since July 2015, and "presenting headwinds for housing." The dollar is nearing a 14-year high which could weigh on manufacturing and other exports and U.S. profits overseas. Consumer confidence is high as is consumer spending. The second estimate of third quarter GDP provided a sizable revision in real consumer spending from 2.1 percent in the first estimate to 2.8 percent. October data however, indicates that spending growth has moderated this quarter.

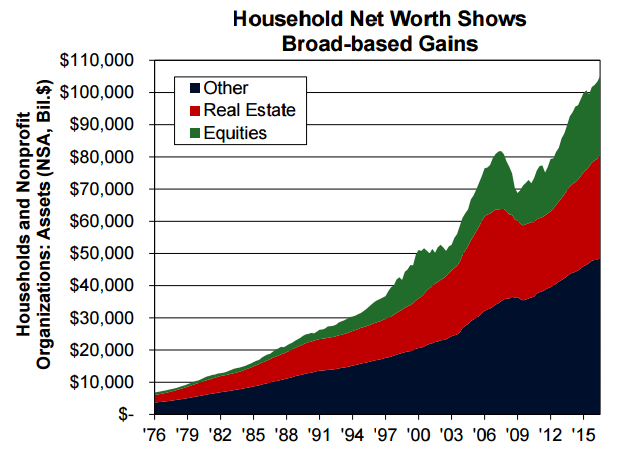

Even with the apparent slowdown in the fourth quarter, the economists expect consumer spending to continue to drive growth. Job growth remains "decent" and wage data is mixed and perhaps not conclusive. Household net worth is up, increasing by $1.6 trillion to $90.2 trillion in the third quarter, boosted by gains in both housing and stock. This should help support consumer spending.

The Federal Reserve Open Market Committee (FOMC) raised the fed funds rate at its December meeting and signaled it expected to do so three more times in 2017 rather than the two it implied in September. However, Fannie Mae points out that there was an indication at one point that there would be four increases this year rather than the one that actually materialized. "We believe that the Fed will likely be in wait-and-see mode given this substantial policy uncertainty and anticipate two hikes each in 2017 and 2018. However, the Fed will be vigilant in monitoring wage pressure, as further tightening in the labor market should lead to a pickup in compensation growth," the ESR Group says. Fed Chair Janet Yellen observed that changes in the fiscal outlook, to the extent that they influence economic growth, labor markets, and inflation forecasts, could alter the course of interest rates. She noted that fiscal stimulus that does not spur faster productivity and labor force growth could result in more upward pressure on inflation and higher interest rates."

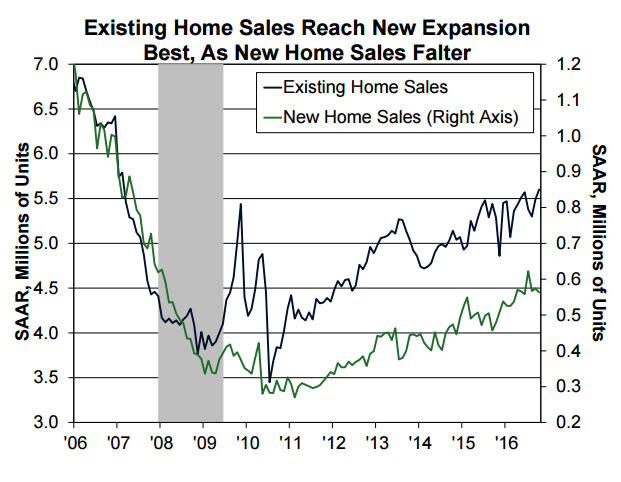

Data so far this quarter indicates a double-digit gain in residential investment. This is consistent with earlier predictions that it would add to economic growth, reversing its drag in the second and third quarters. Both single and multifamily housing starts jumped in October but sales were mixed. Existing home sales rose to an expansion high while new home sales were down.

Unchanged pending homes sales in October suggest that existing home sales will remain strong over the next few months. Another leading indicator of home sales, purchase mortgage applications, has been mixed of late. They declined in October through mid-November but then surged during the third week as the post-election spike in mortgage rates probably spurred some potential buyers to act in advance of even higher rates.

Home prices are still climbing. The CoreLogic Home Price Index, which is used by the Fed to value household real estate assets, put the October year-over-year increase at 6.7 percent. Housing wealth, strongly influenced by home values, rose $554 billion from the second to the third quarter. However, at the same time single-family debt increased 3.7 percent annualized or $93.5 billion, the fastest pace since the end of 2007. Owners home equity as a percentage of the value of household real estate increased to 57.3 percent, just below the previous peak of 59.8 percent in the fourth quarter of 2006.

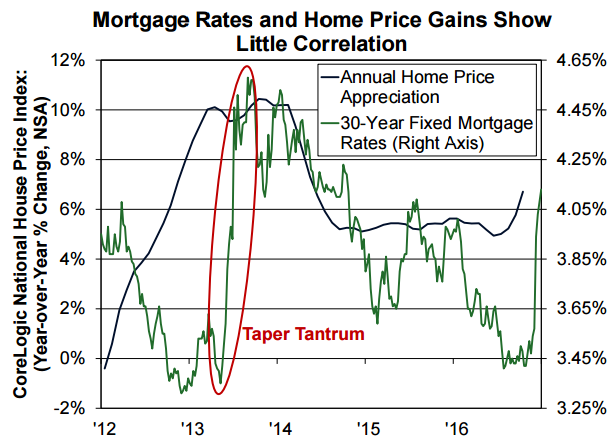

While homeowners benefit from the increases it challenges buyers, especially first timers and this is exacerbated by recent interest rate hikes. The Freddie Mac survey showed rates in early December at 4.13 percent, the highest since October 2014 and some 60 basis points higher than before the election. This could provide some headwinds to home sales but if long-term interest rate gains are accompanied by stronger economic growth, rising incomes could help support housing affordability and home sales. Research shows little correlation between rates and home prices

Fannie Mae is forecasting that rates will rise to 4.2 percent by this time next year, up from the average 3.8 percent in the fourth quarter of 2016. This is 50 basis points higher than the last projection. Their forecast for home sales is little changed from their last one for a 3 percent gain based on their expectations that rates will rise slowly while household incomes and formations continue to grow.

Projections for refinance originations have been revised higher for this year after a stronger than anticipated October, but downgraded for next year due to rising rates. ESR economists expect total mortgage originations to be up 10.0 percent in 2016 compared to 2015, hitting $1.90 trillion. Next year refinancing will decline to about one third of originations and total originations will be down 17 percent to $1.57 trillion.