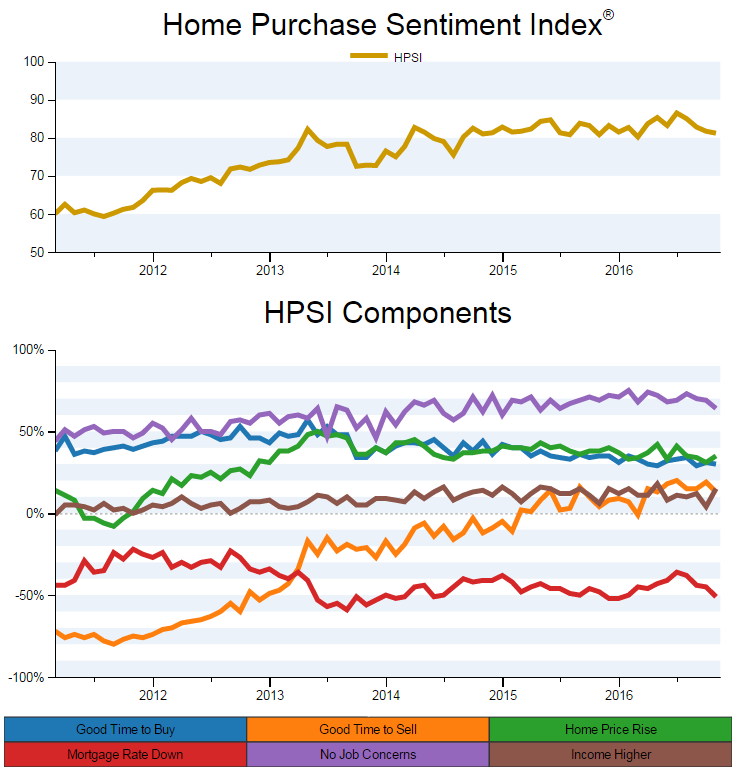

A dramatic uptick in consumer perceptions about household income kept Fannie Mae's Home Purchase Sentiment (HPSI) Index from tanking in November. Even with a net increase of 11 percent in the number of respondents reporting significantly higher household income over the last 12 months (reversing a 9 point drop in October), the Index still dipped 0.5 percent, the fourth consecutive decline.

Net responses to four of the six components that comprise the HPSI were down. Fannie Mae said this reflected mixed consumer attitudes on either side of the U.S. presidential election.

The net share of consumers who expect mortgages rates to go down over the next year and those who believe it is now a good time to sell a home both dropped 6 percentage points from October, while the net share of those reporting confidence that they would not lose their jobs was down five percent.

The net share of those expecting home prices to increase over the next year rose by 4 percentage points. The sixth component, reflecting whether consumers view this as a good time to buy a house, declined 1 percentage point.

"The November Home Purchase Sentiment Index outcome is difficult to interpret as the data collection period occurred across the Presidential election timeline," said Doug Duncan, senior vice president and chief economist at Fannie Mae. "The results are fairly evenly split between responses collected before and after the election, and there is evidence of an increase in consumer optimism in the immediate aftermath of the election. However, we caution readers against drawing conclusions about sustainable changes in consumer sentiment so soon after the election. For example, low mortgage rates have been the primary driver of positive attitudes toward the home buying and selling climate throughout the recovery. However, if mortgage rates continue their recent rise, we may see a dampening in home purchase attitudes. There are clear predecessors for rapid market changes that ultimately dissipated, which urges caution in the interpretation of stability in short-term rate changes. Most recently was the very temporary market reaction to the Brexit and, earlier, the 'Taper Tantrum,' and in both instances the rate regime returned to roughly its prior position. The drivers are somewhat different in this instance but nonetheless suggest modesty in drawing near-term conclusions. All that said, we do not see in the November HPSI results a fundamental departure from a flattening of housing activity relative to prior periods. This is consistent with our corporate forecast of a modest growth in the 12 months ahead."

The Home Purchase Sentiment Index (HPSI) distills information about consumers' home purchase sentiment from Fannie Mae's National Housing Survey® (NHS) into a single number. NHS is conducted monthly by phone among a panel of about 1,000 consumers, both homeowners and renters. They are asked about 100 questions to assess their attitudes toward owning and renting a home, home and rental price changes, homeownership distress, the economy, household finances, and overall consumer confidence.