The Departments of Treasury and Housing and Urban Development have released their joint November 2011 Housing Scorecard. The report is essentially a summary of data on housing and housing finance released by public and private sources over the previous month and/or quarter. Most of the data such as new and existing home sales, permits and starts, mortgage originations, and various house price evaluations have been previously covered by MND.

The scorecard incorporates by reference the monthly report of the Making Home Affordable Program (MHA) through the end of October. This includes information on the universe of MHA programs including the Home Affordable Modification Program (HAMP), HOPE Now, and Second Lien Modifications.

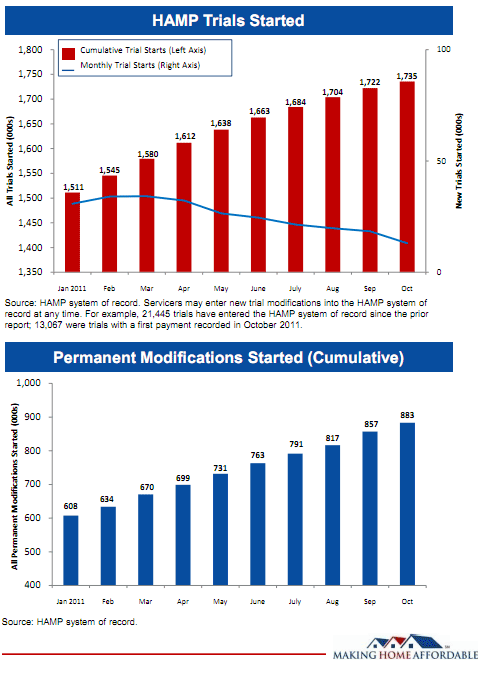

During the month of October HAMP servicers initiated 21,445 new trial modifications and converted 26,102 trial modifications to current status. Since the program was started in April, 2009 there have been 1,735,457 trials started and 883,076 permanent modifications. Slightly more than 85,000 borrowers remain in active trials. The time a borrower spends in trial status continues to improve and now stands at 3.5 months. Over the course of the program 147,600 permanent modifications have been canceled and 735,464 modifications remain in force.

Since October 2010 servicers have been required to evaluate all loans with a loan to value ratio (LTV) greater than 115 for their appropriateness for inclusion in the Principal Reduction Alternative (PRA) program. While servicers are not required to reduce the principal of any given loan, they must evaluate each loan when assessing it for HAMP. Servicers are paid an incentive for every dollar of principal forgiven on a sliding fee scale and depending on the degree to which the unmodified balance of the loan is greater than the market value of the home. Loans belonging to either of the two GSEs are specifically exempted from PRA.

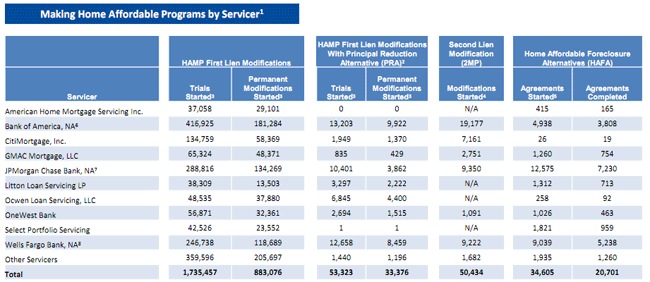

To date there have been 53,323 trial PRA modifications started and 33,376 permanent modifications including it. The median principal amount reduced on a loan in an active permanent modification is $65,172 or 31.3 percent and these loans dropped from a median LTV of 158 percent to a post modification LTV of 115 percent.

The ten largest servicers account for 97 percent of the modifications started with PRA and the top three servicers (Bank of American, Wells Fargo, and JP Morgan Chase) account for 68 percent. Three states (California, Florida and Illinois) are home to 42 percent of all HAMP modifications and 53 percent of those with PRA.

The Second Lien Modification Program (2MP) has now initiated 50,434 second lien modifications, 8,634 of which resulted in full extinguishment of the lien and 1,569 in partial extinguishments. There are 40,878 second liens in modification including the partially extinguished liens.

The Home Affordable Foreclosure Alternatives Program (HAFA) assists borrowers who wish to surrender their homes short of foreclosure, usually through a short sale. To date 34,605 homeowners have entered the program and 20,701 have completed HAFA transactions; 591 through a deed in lieu of foreclosure and the remainder through short sales.

HAMP is reporting that during the third quarter only one servicer, JP Morgan Chase Bank was found to be in need of substantial improvement following the MHA Servicer Assessments. As has been the case in each of the periods since the assessment program began, the Treasury Department will withhold all servicer incentives owed to JP Morgan Chase.

Seven servicers were found to need moderate improvement but only one, Bank of America, will have servicer incentives withheld until it makes additional improvements. The remainder of the servicers needing moderate improvements has been put on notice that they may have incentives withheld in the future unless identified improvements are made.

Treasury Calls Out JPMorgan in Servicer Assessments