With the year nearing an end Fannie Mae's chief economist Doug Duncan and his Economic & Strategic Research (ESR) Group are holding to their most recent projections for the economy; 2.2 percent growth in the current year and 2.4 percent in 2016. This expansion will be supported by "solid consumer spending growth and a pickup in construction activity and continued rising home sales and prices. Headwinds for manufacturing and exports stemming from the strength in the dollar and weak global growth are unlikely to dissipate in the near term. However, the drag on manufacturing from the inventory cycle and declining oil prices should fade next year." Consumer spending is expecting to be the primary driver of growth in the last quarter of 2015 and in early 2016 with residential investment growth projected to strengthen modestly from the 6.1 percent annualized pace in the third quarter.

The company's November economic and strategic summary noted the strong employment report and wage gains from October when nonfarm payrolls were up by 271,000 jobs. The real estate industry received some good news in that report with construction payrolls posting the biggest gain since February. The residential segment however, "remained relatively modest compared with the increases seen earlier this year."

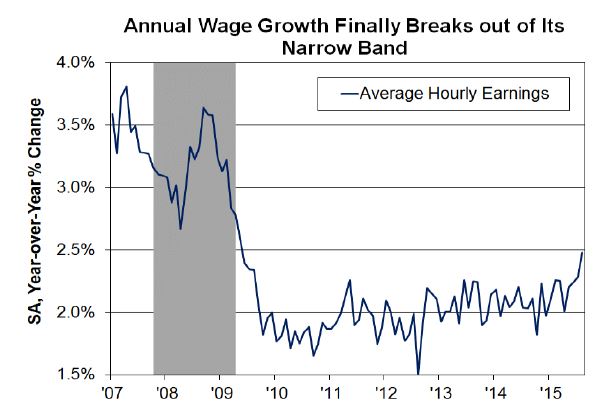

The unemployment rate edged down another 0.1 percentage point to 5.0 percent but better news for housing, given recent concerns over affordability, was the 0.4 percent jump in average hourly earnings after a flat reading in the prior month making the annual gain 2.5 percent, "breaking out of the narrow band witnessed during most of the expansion to reach the fastest rate since July 2009."

The ESR said they view a December decision from the Federal Open Markets Committee (FOMC) to raise interest rates as a strong possibility "barring a dismal November jobs report and international turmoil over the next month." "That will shift the monetary policy debate to the question of how fast the Fed will tighten."

The report called the housing news mixed. Starts rebounded in September exceeding 1.2 million units for the second time in eight years, although it was multi-family units that drove the gain, but permits fell for the second time in three months.

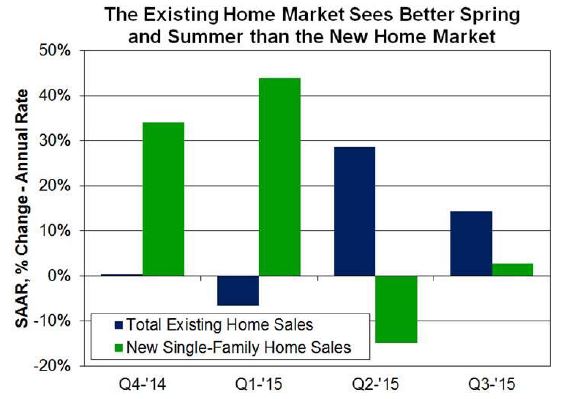

New home sales, which had increased strongly for the two prior months, plummeted in September taking the average for the third quarter down to near the average for the second quarter. Although inventories of new homes have increased on an annual basis every month since January 2013 it is likely a tight supply of more affordable units that is contributing to soft sales. Existing sales, however rebounded in September and for the third quarter as a whole those sales have a double digit annualized gain.

Existing home inventories remain lean and homes for sale September posted a fourth consecutive year-over-year drop. This tight supply combined with declining distressed home sales is putting upward pressure on home prices and the August CoreLogic and September Case-Shiller indexes each showed the strongest annual increases in around a year.

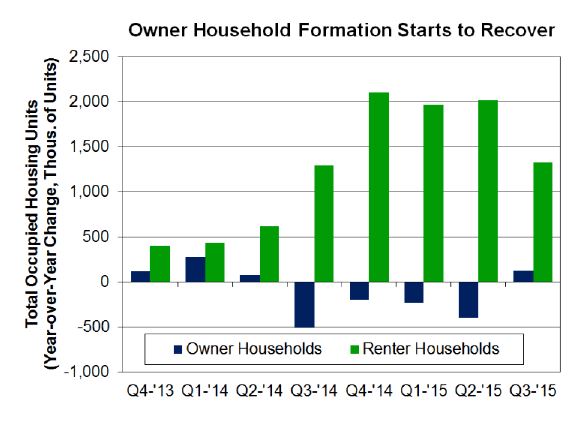

Household formation over the last year has increased by 1.4 million and the homeownership rate was up 0.3 percent in the third quarter, the first quarterly increase in two years.

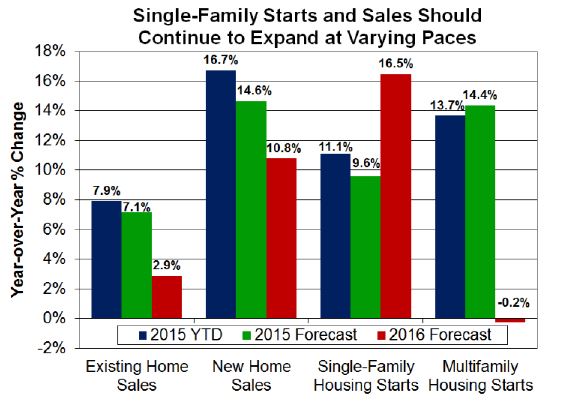

Looking forward the economists expect that fixed mortgage rates should gradually trend up to just slightly more than 4.0 percent by the end of next year, unchanged from their previous forecast. Their projections for housing activity are also little changed. Improvements in single family starts and home sales should continue in 2016, supported by continued low interest rates and the improving income trend and lending standards, especially for GSE mortgages, have eased further according to the October Federal Reserve Senior Loan Officers Survey. "These positive fundamentals should help some recently formed renter households move into homeownership, stabilizing the downtrend in the homeownership rate."

Fannie Mae expect total mortgage originations will rise approximately 32 percent to $1.71 trillion, with a refinance share of 46 percent and purchase mortgage will be driven higher by improving sales. The decline in refinance originations will outweigh the increase in purchase originations, resulting in an 18 percent drop in total mortgage origination in 2016 to $1.41 trillion, and a 14 percentage point drop in the refinance share to 32 percent.