Someone must have passed a law; if it is November, you must publish something debunking bubbles. The saturation point is near, but the latest contribution, from Freddie Mac's Chief Economist Sean Becketti, provides a better (and much longer) analysis than most, so we will attempt to summarize his arguments as to why, despite rapidly rising home prices, we aren't in a bubble. Or as he says, "Not yet."

The concern, he says, is understandable. Scars remain from the last bubble and there are plenty of warning signs regarding a new one:

- House prices have been on a tear for the last five years, growing about twice as fast as the long-run average and outpacing income growth by a cumulative 42 percent over the last 17 years;

- The number of large metropolitan statistical areas (MSAs) with unusually-high house-price-to-income ratios has grown from five in 2011 to 17 today. At the height of the last bubble there were 27.

- An increasing share of MSAs with relatively stable construction costs nonetheless have suspiciously high house prices per square foot.

It is difficult to spot a bubble before it bursts, but Becketti says there are three defining characteristics. First, they are fueled by self-fulfilling predictions, i.e. prices rise simply because people expect them to. Nobel Laureate Robert Shiller called them "a kind of social epidemic" where price increases generate enthusiasm among investors, who then bid prices higher. The feedback continues until prices get too high, and the bubble bursts.

That is the second defining feature of bubbles, they do indeed burst. Not just correct, a normal part of the ups and downs of asset prices, but crash, reflecting a sudden realization that prices have become unsupportable.

The third defining feature is the central role easy credit plays in their growth. When lenders begin to believe that price increases can go on forever, they grow less concerned about whether borrowers can repay the loan. Bubbles collapse when lenders finally get worried and restrict riskier types of credit. Paradoxically, Becketti says, in the last decade lenders restricted credit, thus pricking the housing bubble and triggering the burst they were trying to avoid.

Hunting for bubbles is problematic. Since prices might make a soft landing, it is tempting to monitor conditions a bit longer rather than act. Identifying a bubble can spook people and trigger a crash that didn't need to happen. Becketti admits that Freddie Mac is "stuck." A potentially-destructive house price bubble "is one of the key risks we have to manage as best we can."

The company has talked before about its two-part approach to identifying bubbles, first by comparing the current median house price to the median income (PTI) ratio to a historical norm of 3.5. They have found a national PTI above 4.1 is unusual enough to merit further analysis. It broke through that outlier in 2004, started to collapse in 2006, hitting bottom at 3.3 in 2011. It is currently approaching, but is still under the 4.1 threshold. Because bubbles can be local or regional, Freddie Mac also tracks the PTI ratios for the 50 largest metro areas and as noted earlier, 17 are currently a cause for concern.

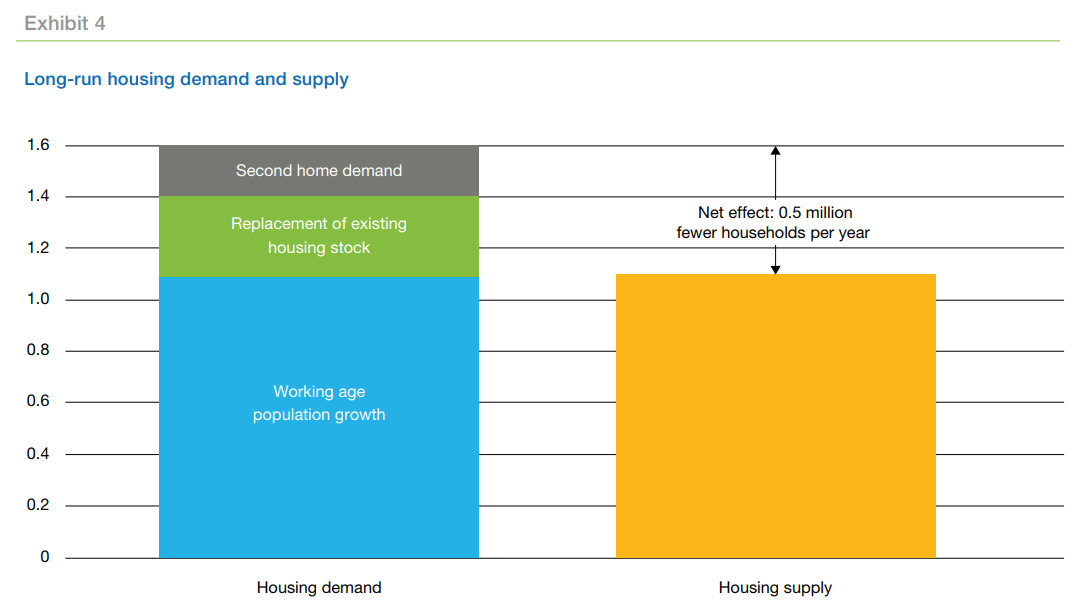

In addition to a high PTI ratio Freddie Mac looks for three other types of evidence. First, can high prices be attributed to economic fundamentals or are they a mass delusion that prices can rise forever? Today the lack of inventory is affecting virtually all of the large metros and houses are not being built fast enough to close that gap. It appears that construction is unlikely to increase fast enough to close the shortfall of houses for several more years. The rate of new home construction is falling approximately a half-million houses short of what is needed to meet demand.

The inventory shortage is strong evidence against a price bubble and the slow rate of increase in construction suggests any eventual price adjustment will be gradual rather than a collapse.

A second piece of evidence is a bubbles' reliance on easy credit. Freddie Mac looks for signs of credit deterioration. Increasing delinquencies and defaults tend to appear very late in a bubble's life, so it isn't surprising that the company's book of business "has exhibited stellar credit performance to date."

A much earlier sign is an increase in leverage; declining home equity. But the reverse is currently the case. While house prices have risen rapidly since 2001, outstanding mortgage debt has barely budged. "Homeowners, at least in aggregate, are not funding a spending spree with the equity in their homes."

So far, no sign of an imminent bubble, however there are those fast-rising home prices. Becketti says maybe they are looking in the wrong places for evidence. The national PTI ratio provided plenty of early warning about the last bubble, enough to have taken corrective action before It burst. But one possible warning sign isn't enough, confirming evidence is needed.

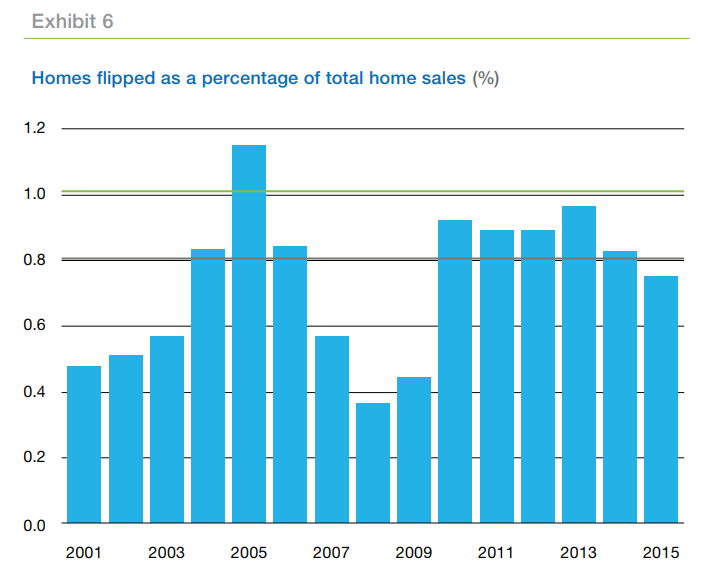

There were other signs preceding the last price collapse and by comparing those metrics' previous-to-current behavior, a body of evidence might accumulate that warns of a building bubble, or convinces that one isn't imminent. One of these is flipping. Shiller says a sharp increase in flipping-buying a house and fixing it up for quick resale-may have contributed to the last bubble as it indicates that speculators are projecting future appreciation.

The percentage of homes that were flipped rose sharply in 2004 to 2006. In Exhibit 6, the two horizonal lines serve as provisional thresholds; When flipping crosses the lower one it should alert us to look for other signs of overvaluation. When it crosses the upper line, the bubble may have already grown to dangerous levels.

From 2010 when prices were still falling through 2014 when prices were rising rapidly the share of flipping exceeded the lower threshold but not the upper one. Flipping in the early years probably reflected investor purchases of distressed properties. In the last two years the high rate of flipping probably reflected both continued distressed purchases and a growing belief among investors that the crisis was over. After 2014, flipping returned below the lower threshold and doesn't appear to indicate a bubble.

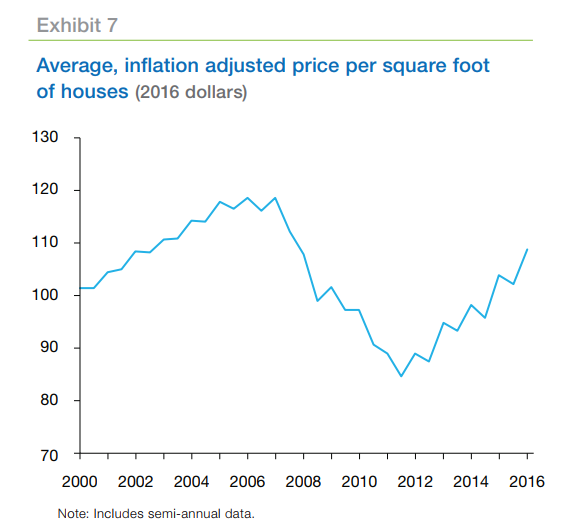

The price of a house per square foot (PSF) is determined by the costs of construction and of land. Construction costs have increased over time, but the rate has been moderate and fairly stable, so where buildable land is plentiful and land use restrictions modest, the PSF of new construction should remain stable as well. This stability normally holds down the PSF of existing houses as well.

This relationship however doesn't hold in cities where there are constraints on buildable land. In cities like San Francisco and Seattle, the increase in demand for houses produces sharp increases in price, but very few houses. Thus, swings in demand in such cities can generate big swings in the PSF of new houses.

In other places with few restrictions on building, the PSF of a new house should track construction costs and remain reasonably stable despite swings in demand. In these cities, like Kansas City or Dallas, sharp increases PSF are likely to indicate a house price increase that cannot be sustained.

Exhibit 7 displays the average, inflation-adjusted price per square foot of both new and existing houses. This average increased steadily prior to the house price collapse, plunged during the collapse and recession, and resumed increasing after 2011. Today the average remains below the 2004 level.

While the evidence does not point to a bubble, how long can house prices appreciate at twice their historical average? Becketti says that historically house prices have managed to deviate from economic fundamentals for long periods of time. But surely there is a limit to the PTI ratio. The median income today is roughly $60,000; can that really buy a $600,000 house? A $1,000,000 house? A $2,000,000 house?

Underwriting standards place a limit on the debt-to-income (DTI) ratio because a high one indicates a borrower may be unable to meet all their obligations at some future date. A high DTI is the most common reason a mortgage application is rejected.

In some cases, borrowers can qualify for a mortgage with a DTI as high as 50 percent. Exhibit 14 displays the percentage of recent borrowers whose DTI ratio would exceed 50 percent at various hypothetical increases in house prices. House prices would have to rise more than 90 percent before half these borrowers would breach that limit. As prices have increased by a cumulative 43 percent since 2011, it appears they can increase a lot more before pricing a significant share of borrowers out of the market.

The long-term relationship between house prices and incomes is always restored eventually. Perhaps several years from now inventory shortages will disappear, and supply and demand will balance, putting house prices more in line with household income.

How will that happen? Will it again be a sudden disruptive correction that roils the economy or is a soft landing likely? Becketti proposes a few possibilities.

In his first scenario, a soft landing could result as increases in residential construction eventually slow price gains. Construction is currently trending slowly upward. That slow pace is not all bad as it prevents a sudden drop in house prices that could hurt recent homebuyers.

Baby Boomers have been slower than their ancestors to sell the family home, exacerbating the inventory shortages. Eventually increasing age and mortality will release more homes onto the market. This trend will also be gradual, cushioning the market against sudden price declines.

Millennials' slow entry into homebuying has contributed to a low homeownership rate. If this continues it will take some of the heat out of housing demand.

A second scenario would have homeownership remain low while renter households increase. This could occur if residential construction doesn't pick up, and/or if Federal Reserve actions increase interest rates significantly. Either will lessen housing affordability. Regulatory constraints are likely to grow as existing homeowners lobby to protect their homes' value.

This would restore equilibrium by creating a permanent division between the housing "Haves" and "Have Nots." First-time homebuyers and moderate-income households would face severe challenges, bifurcating homeownership between the affluent and everyone else. Wealth inequality would grow as fewer households take advantage of the wealth-building associated with homeownership. Single family rentals would increase, particularly if regulatory constraints limit higher-density, multifamily development.

The final scenario pictures a worsening of the current imbalance between supply and demand, eventually creating a bubble where none currently exists. A few more years of rapid price increases could erase memories of the last crash and reset expectations of future house prices higher. Some bad pre-crash practices, such as borrowing against home equity, could return. The cycle of house price increases followed by additional borrowing eventually becomes unsustainable, and the bubble bursts.

While evidence indicates there is no current price bubble, the housing sector is significantly out of balance. What can't be predicted is how this imbalance will be resolved.