Frank E. Nothaft and Leonard Kiefer, Freddie Mac's chief and deputy chief economists have come up with a formula for lifting the economy from its continuing low-growth status to a trajectory of robust sustainable growth. And that's what they are calling it, L.I.F.T. The acronym stands for Labor, Income, Fixed Investment, and Trust and in the current edition of the company's U.S. Economic and Housing Market Outlook they lay out the parameters for each.

Labor

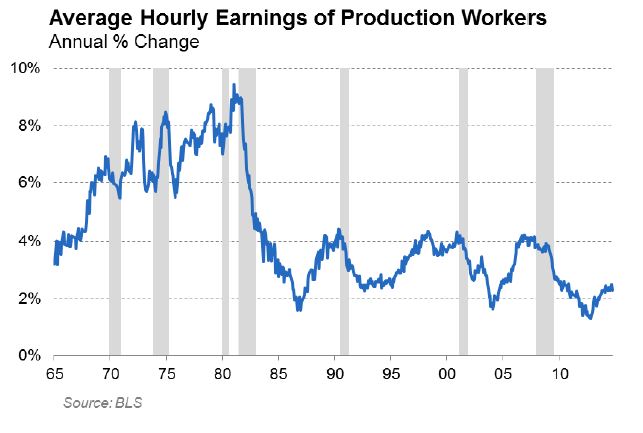

The labor market must fully recover, providing solid employment gains, less long term unemployment, and broad-based income growth. Unless the labor market recovery accelerates, any improvement in the housing market will also lag. Last month the unemployment rate finally fell below 6 percent for the first time since the recovery began but that number does not tell the full story.

There must be three other factors in addition to lower unemployment. Labor force participation among younger age groups must improve, especially for those 25 to 54 years of age. Second, long-term unemployment must return nearer to historical norms and finally, there must be sustained wage increases.

The economists see only modest further improvements in the headline unemployment rate; an average of 5.7 percent in 2015, only .2 percent below the current level, because the improving labor market will bring many dropouts in the 25-54 age cohorts back into the job hunt.

Income Growth

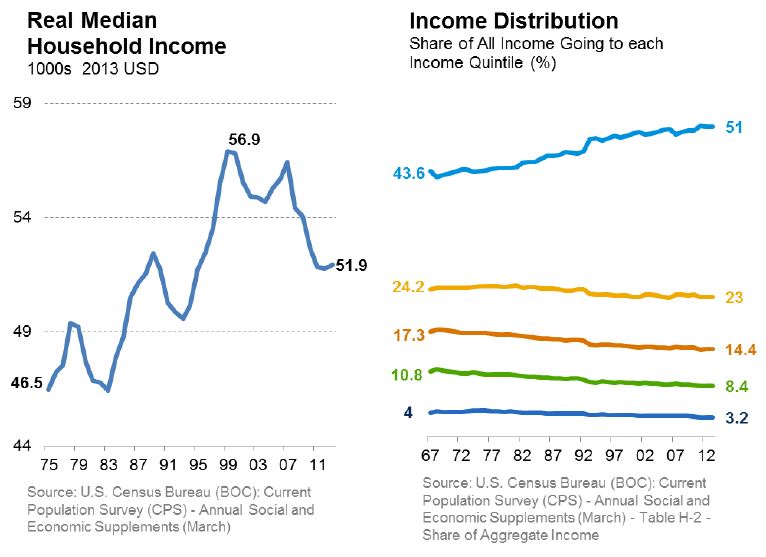

Income growth has been, in Nothaft's and Kiefer's words, "tepid at best" throughout the recovery. Per capita income has improved over the last five years but the gains have not been broad-based. From 1999 to 2013 real inflation-adjusted median household income has fallen from $56,900 to $51,900. The economy will not function at its best until incomes rise across the board. A faster growth in GDP is essential to accomplish this.

GDP growth has started to accelerate and the economists expect a robust third quarter report with over 3 percent annualized growth. For this to continue there must be normalized fixed investment, particularly in the residential sector.

Fixed Investment

Fixed investment in residential and non-residential buildings, computers, and other equipment has been slow to recover. At the end of the recession investment picked up, but as a share of total GDP is still about 2 percentage points below the levels reached prior to the Great Recession.

Residential spending is particularly depressed. Prior to the recession this type of investment, especially construction of residential units, averaged about 5 percent of GDP but since June 2009 has been around 3 percent. There have been about 1.0 million housing starts in the past 12 months while the nation needs to add perhaps as many as 1.7 million housing units per year to keep up with demand.

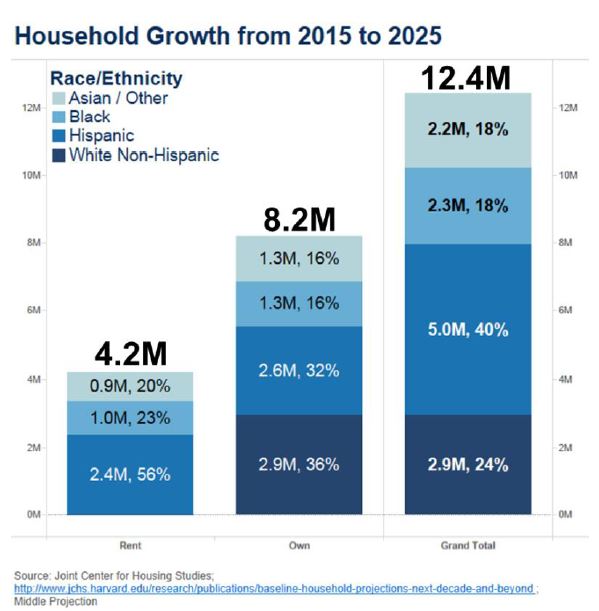

Household growth over the next ten years is projected at 12.4 million, 8.2 million of which are expected to be homeowners and there is not enough vacant housing stock to absorb them. The gap between today's residential investment and potential long-term demand demonstrates that an increase in investment could add significantly to GDP growth.

Trust and Confidence Restored

Confidence and trust in the economy are fragile today but they are needed to propel economic growth. Following the recession confidence was at historic lows and uncertainty about the future was high. Ongoing debates over fiscal and monetary policy, regulations, and concern about lawsuits have increased uncertainty. But headlines about these issues have ebbed, and economic policy uncertainty is near the lowest level since the end of the recession. Still there are many actual and potential crises both home and abroad that call for a wary eye on the economy to see if confidence falters.

Freddie Mac's economists say they remain optimistic for growth at home even if the rest of the world slows down and an improving labor market, robust GDP growth, resilient consumers, and a decline in the price of oil should help the economy in the short run. A strong pent-up demand for housing and low interest rates should do the same for the housing sector in the long-run.