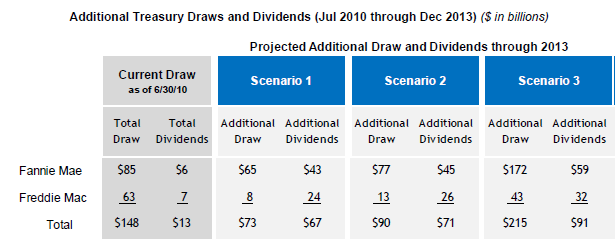

The Federal Housing Finance Agency (FHFA) has released projections showing possible future financial performances of Fannie Mae and Freddie Mac and the potential draws from the U.S. Treasury under terms of the Preferred Stock Purchase Agreements (PSPAs). To date Fannie Mae and Freddie Mac have drawn down a total of $148 billion in Treasury funds since the two government sponsored enterprises (GSEs) were placed in federal conservatorship in August 2008.

The projections, which are based on three different scenarios, result in cumulative draws by the two GSEs that range from $221 billion to $363 billion through 2013. However, dividends paid by the Enterprises to the Treasury continue to make up increasingly larger portions of those draws and if those dividends are excluded, the cumulative draws range from $142 to $259 billion.

While each GSE was directed to project revenue, mark-to-market gains and losses, credit related and other expenses earnings, and ultimately their credit draws using its own respective models, according to Acting FHFA Director Edward J. DeMarco the projections are modeled on the approach that federal banking agencies used in the Supervisory Capital Assessment Program in 2009 and are intended to give policymakers and the public useful snapshots of potential outcomes for taxpayer support "These are not predictions; the results reflect the potential effects of a limited set of hypothetical changes in house prices, a key variable driving credit losses for the Enterprises."

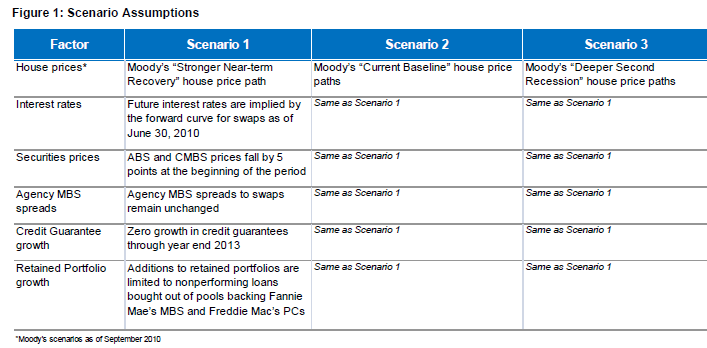

The three scenarios used to construct the projections are identical except for the variable that reflects house prices, the factor that has had the largest impact on the Enterprises financial results to date. Each scenario is based on the following assumptions:

- Future interest rates are implied by the forward curve for swaps as of June 30, 2010;

- ABS and CMBS prices fall by 5 points at the beginning of the period;

- Agency MBS spreads to swaps remain unchanged;

- Zero growth in credit guarantees through the end of 2013;

- No further addition to retained portfolios except non-performing loans bought out of pools backing Fannie Mae's MBS and Freddie Mac's PCs.

The house price factor for the first scenario is Moody's "Stronger Near-term Recovery" house price path in which increased access to credit supports the above-baseline growth and recent increases in house prices are sustained and additional increases are minimal in 2010 and 2011. From the price trough in the first quarter of 2009 to the end of the forecast period (Q4, 2013) house prices increase by 5%.

In the second scenario, the Current Baseline "small remaining home price declines" results in a peak to trough decline of 31 percent with a trough that is not reached until the third quarter of 2011 after which prices rise 8 percent by the end of the forecast period.

The third scenario assumes a Deeper Second Recession. As a result of restricted access to credit and continuing high unemployment, the moderate rebound in housing construction that occurred over the first half of 2009 not only pauses but reverses course. The peak-to-trough decline is 45 percent, reached in Q1 2012, after which prices rise by 11 percent.

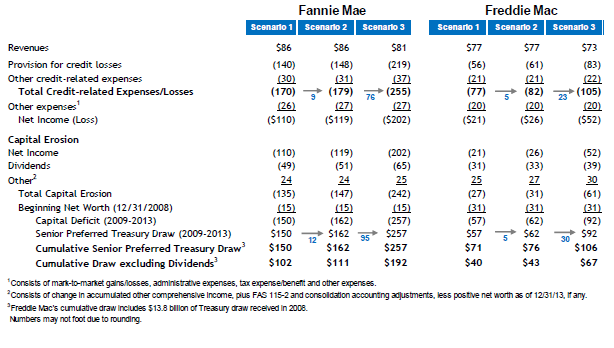

Credit-related expenses, particularly provisions for single-family credit losses, are the driver of the projected draws regardless of the scenario used. Fannie Mae's credit related expenses increase from $170 billion under Scenario One to $255 billion under Scenario Three while Freddie Mac's increase from $77 billion to $105 billion.

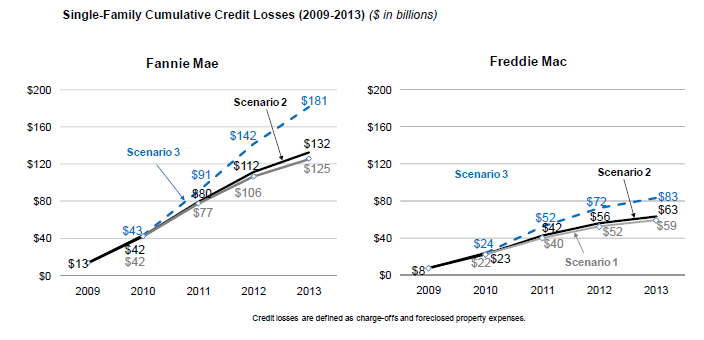

Since 2007, the GSE's provisions for single-family credit losses have been driven by increases to loan loss reserves, however, going forward it is anticipated that charge offs and foreclosed property expenses will increase as the backlog of delinquent loans is resolved. It is expected that Fannie Mae's single-family cumulative credit losses will surge from around $43 billion at present to $125 billion under Scenario One; $132 under Scenario Two and $181 billion under Scenario Three by the end of the projection period. Freddie Mac's cumulative losses, currently at around $23 billion will go to $59 billion, $63 billion, and $83 billion.

Under the three scenarios the following projections emerge for draws under the PSPAs through the end of 2013. Fannie Mae's projected draws are approximately double that of Freddie Mac in part because the former's mortgage book of business is 45 percent larger.