Despite expecting an economic slowdown as reflected in the gross domestic product (GDP), Freddie Mac published a pretty upbeat September forecast as the month, the third quarter, and the government's fiscal year ended on Monday. The company's Economic and Housing Research Group sees consumer confidence and housing helping to shore up less positive factors.

On the downside, the company expects that government spending, business investment, and net exports will all decline, pulling the GDP down from its average growth of 2.6 percent in the first half of the year to 1.9 percent in the last half, to an average of 2.2 percent for the full year. Growth will decelerate even further in 2020, to 1.8 percent. Growth will be maintained at that level partially because of strong consumer confidence which is expected to bolster consumer spending

Mortgage rates jumped in September but remain significantly lower than at the same point last year. Freddie Mac's average for the 30-year fixed-rate mortgage was 3.64 percent for the week ending September 26th, down 1.08 percentage points from a year earlier. These rates have translated into a stronger housing market and both home sales and housing construction are firming. There should also be a noticeable increase in mortgage refinance originations in the coming quarters.

Consumer price inflation remains muted. The Consumer Price Index (CPI) increased 1.7% over the 12-months ending August 2019 and the core inflation index, the Federal Reserve's favorite measure, increased 2.4 percent in the 12-months ending in August. Stronger core inflation, which ignores food and energy prices, should translate to higher headline inflation in the coming months. The forecast is for the CPI to increase 2.2 and 2.3 percent annualized in the third and fourth quarter of 2019 respectively and then to fade next year. The average rates should be 2.1 percent for the entirety of 2019 and 2.0 percent in 2020.

There should be little change in the continuing strong labor market. The unemployment rate is expected to remain at 3.7 percent through the end of the year and the job creation to continue what is now a 107-month positive streak.

Trade concerns are still feeding volatility into the global bond markets with a resulting increase in the appetite for U.S. Treasuries. As trade talks ebb and flow, Treasury rates do as well. Despite this, Freddie Mac expects long-term rates to remain flat and the 10-year yield to average 1.8 percent next year compared to the average of 2.1 percent this year. These yields will keep mortgage rates low in the coming quarters, a projected 3.7 percent for the 30-year fixed-rate mortgage in the fourth quarter. The year should finish at an average of 4.0 percent and decline to 3.8 percent next year. This is a slight increase in their projections last month - 3.9 percent this year and 3.7 percent next year - and is their third revision in as many months.

The Federal Reserve cut its funds rate a quarter point at its September meeting and Freddie's economists expect one more reduction before the end of the year and an additional one in 2020. The rate should then stabilize at 1.6 percent.

Lower rates have boosted the housing market. Housing starts in August 2019 beat consensus estimates, increasing to 1.36 million units at an annual rate, the highest level since 2007. More housing is desperately needed and starts should average 1.25 million this year and 1.28 million next year.

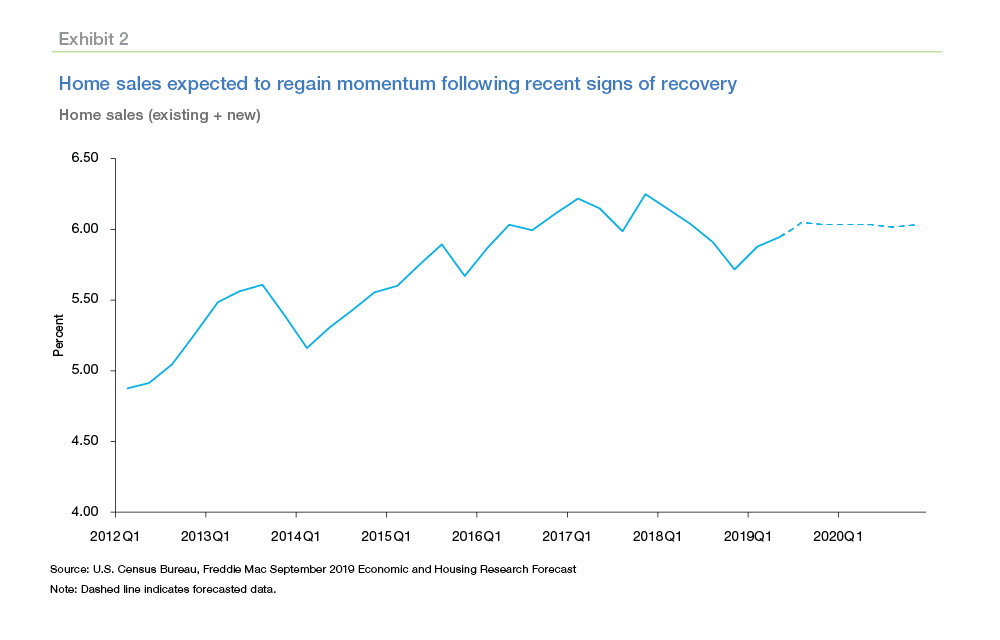

Home sales have responded to lower rates as well, and those for existing homes also beat expectations in August with an annual rate of 5.39 million. This momentum should carry over into the fourth quarter and early next year. Total sales, new and existing, will reach 5.98 million this year and 6.03 million in 2020.

After decelerating earlier in the year, incoming data over the past few months indicate that house prices will continue to beat expectations in the coming months. They should appreciate 3.4 percent this year and then taper to 2.7 percent in 2020.

Declining mortgage rates will boost mortgage origination volumes. The Mortgage Bankers Association Weekly Applications Survey reflects this, with the refinance index up 148 percent from September 2018. Surging refinance activity will lift the refinance share of mortgage originations to 44 percent for the full year 2019. Purchase mortgage originations have also seen a modest increase as home sales have increased and total annual mortgage originations are forecast at 2.1 trillion in 2019 and 1.8 trillion in 2020.