Despite improved consumer spending and stronger residential and non-residential investments Fannie Mae's Economic and Strategic Research team are holding to their earlier forecasts for the second half of 2015. In their current monthly report they estimate that economic growth at an annualized 2.8 percent in the second quarter, up 0.4 percent from what they projected in June, with an acceleration during the second half to about 3.0 percent. They were, they said, already ahead of the game, having upgraded their full year estimate of growth from 1.9 percent to 2.0 percent in June, based on earlier revisions to the GDP.

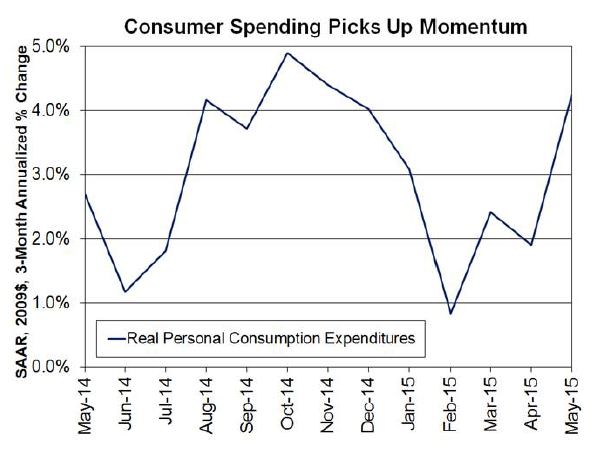

Consumer spending is expected to be the biggest driver of growth for the rest of the year. It is showing signs of a turnaround accelerating to an estimated 2.9 percent in the second quarter from 2.1 percent in the first and was at an annualized 4.2 percent over the three months ending in May. Housing and government spending will also be a major contributors to growth while net exports will be a drag as will the decline in oil prices over the last year. The debt crisis in Greece still poses a downside risk to the overall forecast as does a deteriorating economic picture in China.

Personal income followed a 0.4 percent gain in April with another 0.2 percent in May and the Consumer Confidence Index jumped 6.8 points from May to June, the second highest reading (tied with March) in the expansion. Adding a bit of frosting, household net worth had its best showing since the third quarter of 2007 and the nation is on track to add 2.5 million jobs this year - less than last year, but still what Fannie Mae calls a "solid" number.

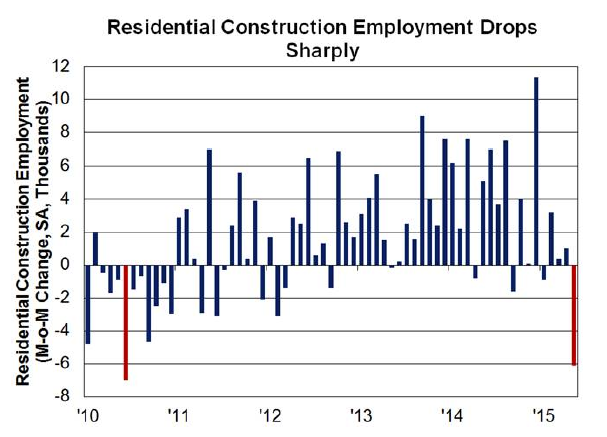

On the housing-related front, residential construction employment dropped precipitously in May but Fannie Mae said it expects home building activity and residential construction employment to pick up along with housing demand. One concern is that builders may find it increasingly difficult to hire skilled workers without substantially raising wages. Wage gains in that sector have picked up after a sharp slowdown last year. This is in contrast to the overall wage growth, which has been moving sideways at approximately 2.0 percent over the past three years.

A recent survey of single-family builders conducted by the National Association of Home Builders (NAHB) showed that home building labor shortages have become even more widespread during the past year, especially for workers with basic skills such as rough carpentry and framing. The current shortage of workers is substantially more severe than at the peak of the housing boom and rivals the widespread shortage just before the start of the expansion in 2001.

Home sales were notably stronger in May and should post a sizable increase in the second quarter. Existing home sales rebounded 5.1 percent to the strongest pace since November 2009, a date coinciding with the expiration of the first-time home buyers' tax credit. New home sales increased 2.2 percent following an 8.1 percent rebound in April. Combined, total annualized home sales of 5.9 million units in May mark the strongest pace since June 2007.

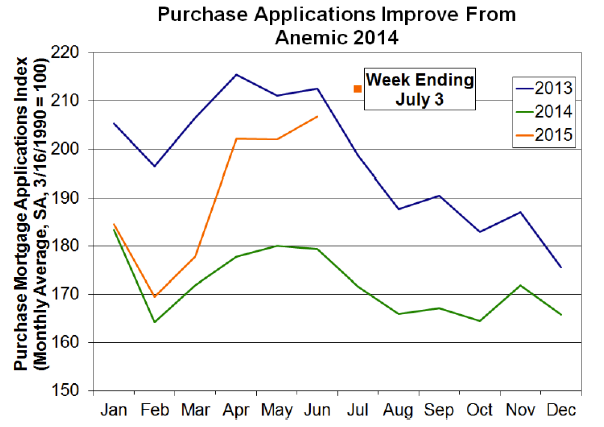

Pending home sales, at a nine-year high, and purchase mortgage applications at the second highest level in two years point to continued improvement in home sales. Meanwhile, mortgage lending standards are easing on the margin, although they remain tight by historical standards. Fannie Mae's second quarter 2015 Mortgage Lender Sentiment Survey found more lenders are loosening credit than tightening it.

Inventories remain low while home builder confidence reached 2015 highs. This combination of strong sales, lean inventories, and rising confidence to lead to increased home building activity this year. The sales and inventories are also putting upward pressure on home prices with the CoreLogic Home Price Index, the measure used by the Fed to estimate real estate value in its Financial Accounts, showing a robust 6.3 percent year-over-year gain in May, the strongest pace since last July.

Improving prices are giving consumers a reason to look favorably on the climate for selling. Fannie Mae's June National Housing Survey showed that the share of consumers who believe now is a good time to sell a home reached a new survey high, increasing three percentage points to 52 percent, above the 50-percent threshold for the first time in the survey's five-year history.

The jump in the number of renter households is putting upward pressure on rents. Household formation, lagging for five years, finally took off in late 2014. These newly created households are largely renters and increased demand has pushed vacancies lower and driven rents higher.

Details in the Consumer Price Index (CPI) showed that both tenant rent and owners' equivalent rent have risen considerably in the last two years. In May, the CPI for tenant rent was up 3.5 percent from a year ago and owners' equivalent rent rose 2.8 percent. Consumers are also primed to expect further rent increases and Fannie Mae's survey suggests that more renters may soon find owning to be more cost-effective than renting and more sellers likely to put their homes on the market.

Mortgage rates have been trending up since February, cooling refinance demand to the lowest level of the year in June. The problems in Greece and China have renewed interest in U.S. Treasuries which should help keep long-term interest rates low, helping home sales in the crucial summer selling season but will trend up going forward. Fannie Mae expects a gradual rise from about 4.0 percent currently to about 4.5 percent by the end of 2016.

Fannie Mae changed a few earlier housing forecasts, modestly upgrading projected home sales for 2015, with existing and new home sales rising by approximately 5 percent and 25 percent, respectively. The forecast of mortgage originations has the upward revision in projected purchase originations slightly outstripping the downgrade in projected refinance originations resulting in little change. For all of 2015, the economists expect total mortgage originations to rise approximately 24 percent to $1.46 trillion, with a refinance share of 47 percent.