Will the homeownership rate fall below 50 percent? Not a question most housing industry stakeholders want to think about, but some analysts are speculating that it could happen. Freddie Mac, in its June edition of Outlook, takes a look at some of those predictions.

The company's economists start out by reiterating their oft-stated conviction that 2016 will be the best year for housing in a decade. Despite a generally weak economy they expect housing to "be an engine of growth," with residential investment providing a direct boost and higher home equity contributing to consumer confidence and leading to higher consumer expenditures. But they concede that the outlook for homeownership is mixed.

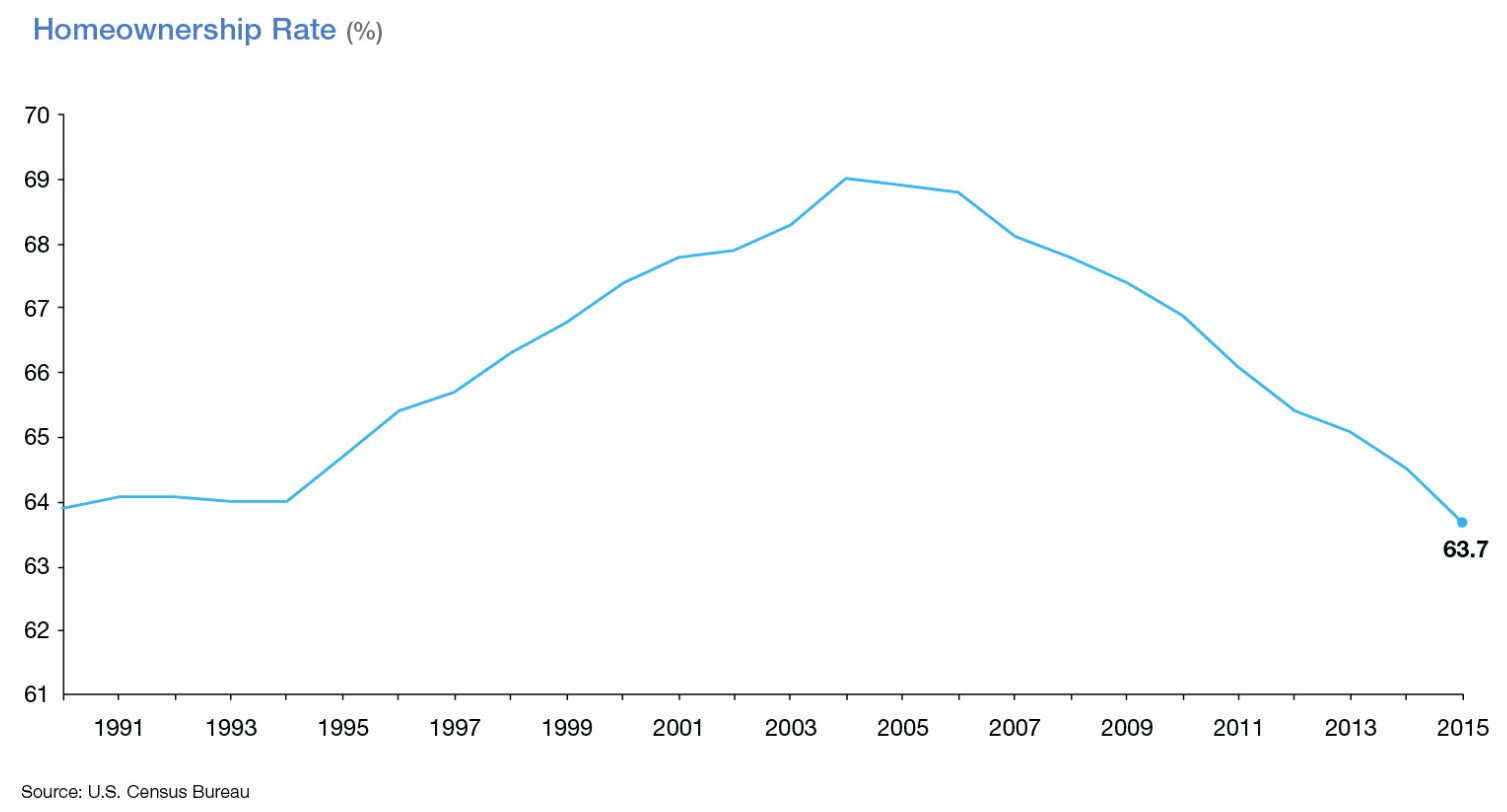

The rate of homeownership has declined precipitously since hitting a peak of 69 percent during the housing bubble. It fell to a 40-year low a few quarters ago and has remained below 64 percent. Many analysts, Freddie says, expect to see the rate fall even further.

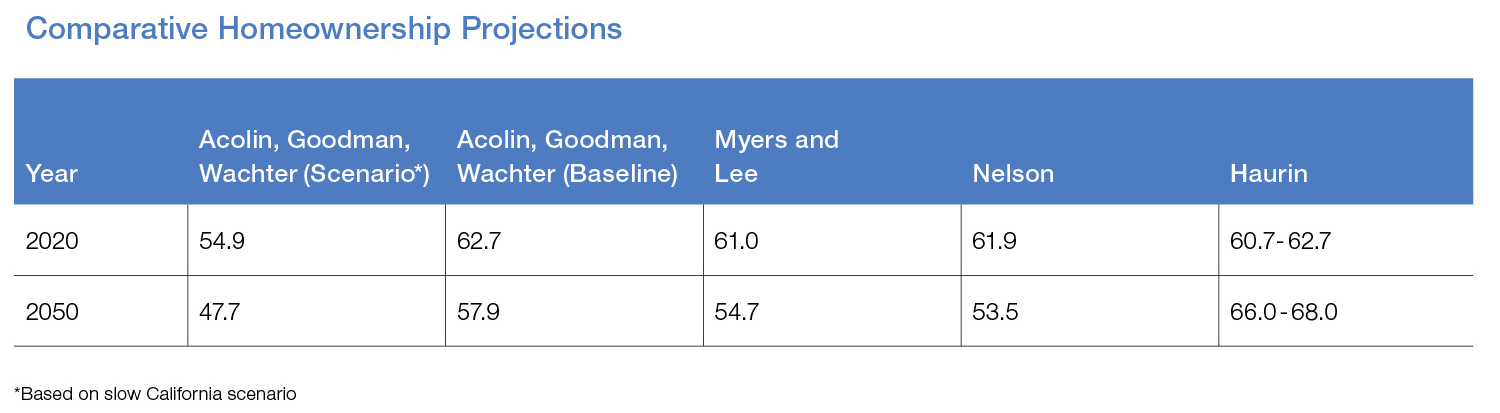

While most do not expect it to fall under 50 percent, Freddie Mac says a number of recent articles, all published in CityScape have set out a range of plausible scenarios where a drop of 20 percentage points in the rate could happen by 2050.

In a 2016 article, A. Acolin, L.S. Goodman, and S.M. Wachter state that such a decline is plausible in a market where rents and house prices increase somewhat faster than inflation and use California as representative of what the nation could become as its future demographics are expected to be similar to the California of today. California also has high rental costs and home prices relative to income.

The result of high ownership costs could be fewer people with the option of owning a home because high rentals could prevent them from saving a larger down payment, even at the 3 percent down payment rates currently available. Further, the authors believe that if this trend continues it will preclude renters from ever becoming homeowners.

Other experts, Freddie Mac said, while agreeing with the qualitative outcome, differed on the severity and emphasized different drivers. C. Nelson believes the current trends that are driving down homeownership will be difficult to reverse. D. Myers and H. Lee believe the effects of the Great Recession will echo forward for decades driving down homeownership that a major cataclysmic event such as a 35-year perpetual recession would be necessary for a 20 percentage point decrease.

D. R. Haurin contends that a 20 percent decrease in homeownership is unlikely but does think another one- to two-point decrease by 2020 is possible after which he sees a gradual increase. Haurin explains that a 20 percent decline would require a combination of plunging rents, surging house prices and/or mortgage rates, and adverse demographic changes. All of these, he argues, are unlikely to occur. Furthermore, he contends that in about a decade, potential homeowners will have adjusted to the need for higher credit and larger down payments.

Freddie Mac's economists put forth several factors they believe will drive the homeownership rate.

- Lack of income growth constrains affordability and median income in 2014, after adjusting for inflation, is at about the same level as in 1996.

- Housing cost burdens continue to increase. According to the Joint Center for Housing Studies, there have been rapid increases, particularly for renters. High renter-cost burdens make it difficult for prospective homebuyers to save up for a down payment and other expenses related to a home purchase. High home prices make the entry point into homeownership difficult for prospective homebuyers.

- Student debt burdens have risen substantially but the evidence on how much that debt has hindered homeownership has been mixed. Freddie Mac says those burdens are certainly an issue and, if they continue to rise, could weigh on the homeownership rate.

- Tight credit conditions have reduced access to credit over the last decade. Moreover, new regulations have increased the cost of mortgage origination from $4,700 in 2008 to $7,000 in 2015 and these costs as well as higher servicing costs have left many lenders leery of lending to those with less than pristine credit. The specter of possible mortgage repurchases also works against the less creditworthy but there was been a 95 percent decline in repurchases 2010 to 2015.

- Homeownership has long been viewed as a path to obtaining wealth, particularly in low income households. The Great Recession however may have altered that perception. If so, the desirability of homeownership will be reduced particularly in the face of other factors. For example, the desire for mobility may lessen that for homeownership. There is also what is called "cohort momentum." Groups that come of age during a recession carry the effects of that event throughout their lives and only gradually, if at all, see their homeownership rates match that of cohorts that come of age during an economic expansion.

- The shifting demographics in the country will have profound impacts on homeownership. White households have traditionally had higher rates than other ethnic and racial groups and the extent to which minority households close this gap will have a major impact on future rates.

- Multigenerational housing may increase along with housing cost burdens, the numbers of elderly, and ethnic diversity and, if so, homeownership rates would suffer

The opinions analyzed by Freddie Mac explicitly considered one or more of the above factors and which factors they considered affected their conclusions.

The analysts came out with varying projections for homeownership rates, both at the end of this decade and in 2050. The variation, Freddie Mac says, is largely due to the requirement of predicting the effects of uncertain parameters. The company says it is conducting its own research into how these factors might affect homeownership and the future of the housing market.