According to The Wall Street Journal Wells Fargo Mortgage is revamping its home equity line of credit loans (HELOCs) to eliminate the interest only feature that has characterized these products. HELOCs generally have a set interest-only payment period, typically 10 years, and then convert to an amortizing loan, recasting the amount required for the monthly loan payment. The bank's reformulation will affect the majority of HELOS with some exceptions for customers with significant assets.

According to Brad Blackwell, a mortgage executive at the bank who was interviewed by the Journal's Nick Timiraos, Wells is restructuring the product to eliminate the prospect of future payment shock and to protect the consumer for the long term. Interest only payments kept homeowners from building additional equity in their homes and payments could increase sharply when the amortization period kicked in. "We took this move not only because it's the right thing to do for our customers, but because we'd like to lead the industry to a more responsible product," Blackwell said.

Blackwell indicated that Wells Fargo might also be guarding against the possibility that loan officers might use HELOCs to make an end run around new mortgage rules that require lenders to document the borrower's "ability to repay" before granting a first mortgage loan. These rules to not effect equity lending.

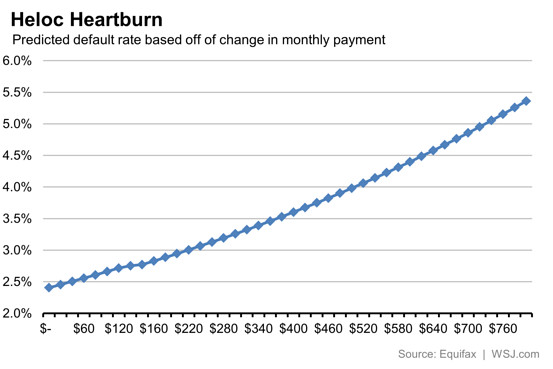

The paper said that the HELOCs originated in the years leading up to the housing crash - 2004 to 2008 - are now approaching the end of their interest only period and loans that will face a payment reset this year could see a monthly payment increase averaging over $300. That increase mounts during each subsequent origination year and those loans that will reset in 2006 and 2007 will see an average of about $425 more in each monthly bill. Equifax has produced a graph showing the effect such increases have on loan default rates

Many of the borrowers drew much of the equity out of their homes with the loans and have subsequently seen the value of those homes fall sharply. This leaves them with no way to refinance and consolidate the HELOC payment into a first mortgage with a longer amortization term.

Blackwell said the end-of-the draw event for existing loans has been less than expected. The bank reaches out to borrowers as much as two years before the reset to encourage them to refinance or pay down the debt. The bank has about $28 billion in loans, about a third of their HELOC portfolio, that will reset between now and the end of 2017.

Home equity lending peaked at nearly $500 billion in 2006 then dropped to less than $100 billion in 2010 and 2011. It has risen slowly since then and saw an uptick in the first quarter of this year as prices gave homeowners back some of the lost equity giving them leverage to borrow. Equity lending, however, is still less than a quarter of what it was during the housing boom.

Timiraos says banks see potential promise for a resurgence ahead as a combination of increasing equity and the first mortgage rates locked in by many owners who have refinanced make HELOCs a way to borrow against the home while keeping those low rates.

Wells Fargo is the nation's largest home equity lender with about a 15 percent market share. The Journal says JP Morgan Chase, the third largest lender is also considering eliminating its interest only home equity loans.