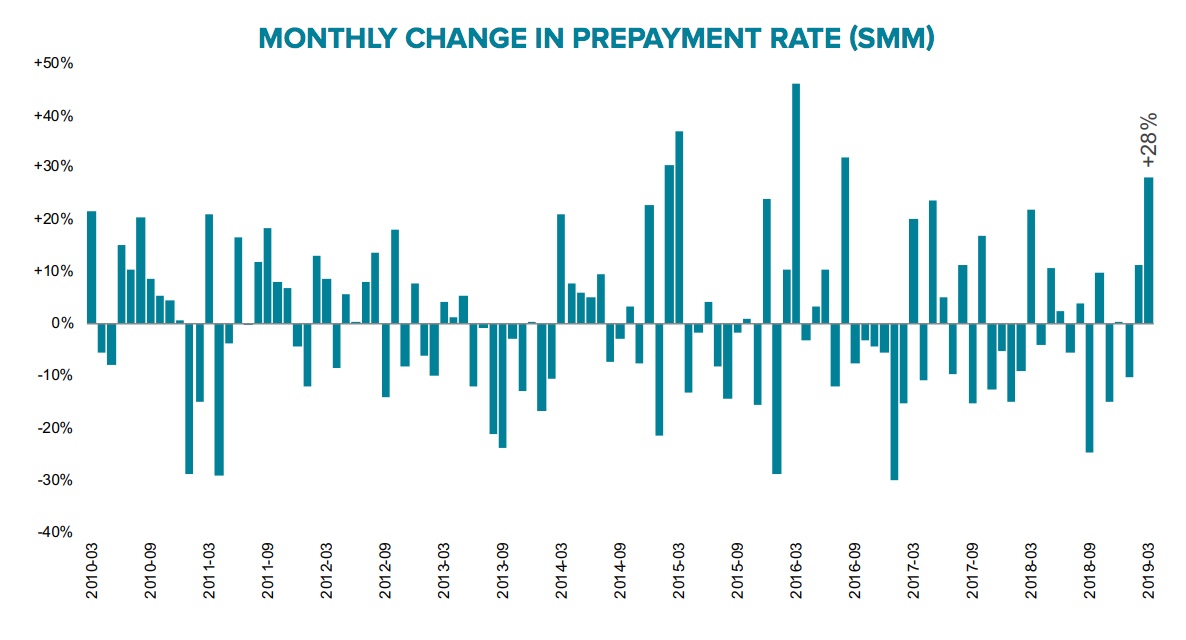

Prepayment rates historically tend to increase in the spring, but this year they have been exceptionally high. The rate has risen during March in 18 of the past 19 years with an average gain of 21 percent. In its March Mortgage Monitor Black Knight says that prepayment activity increased by a total of 40 percent in February and March and in March alone by 28 percent. It was the largest increase in 2.5 years.

While home sales are what usually drive spring increases, this time it is the softening of interest rates and a growth of refinancing. That means some significant differences in the prepayment rate across both investor types and loan vintages due to varying rate sensitivity.

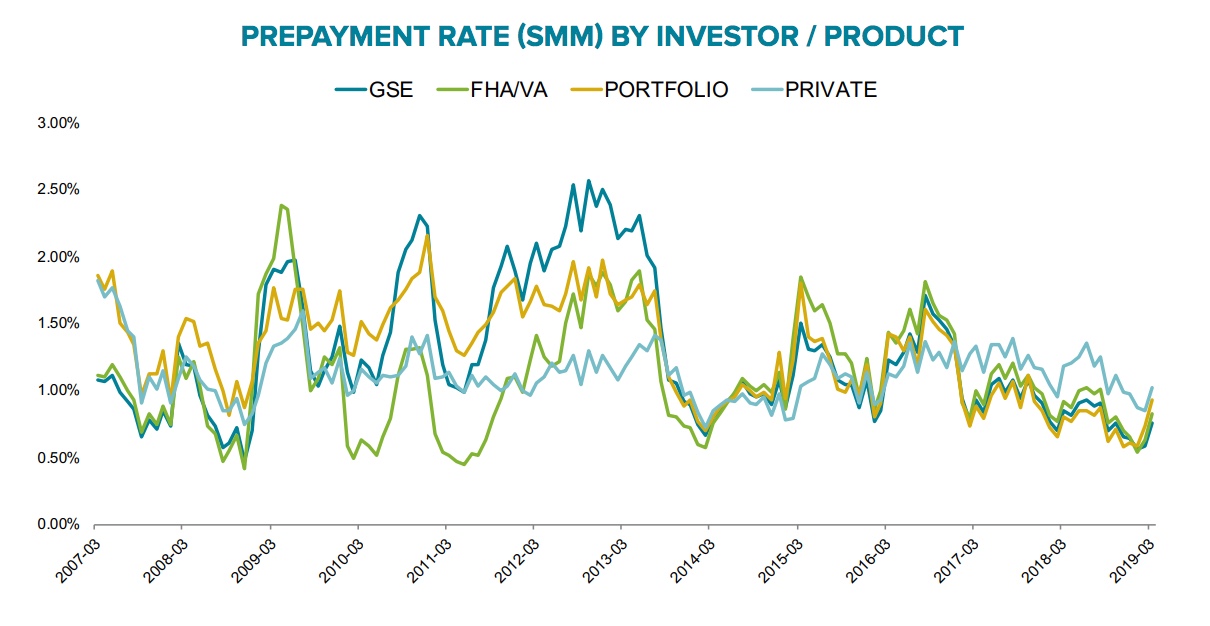

The rate is highest among portfolio lenders at an aggregate of 58 percent over the two months, and FHA/VA loans with rates over 50 percent. Portfolio loans have higher balances and credit scores on average and thus have both more motivation and more ability to refinance. The increase in government-backed loans suggests that FHA borrowers may be taking advantage of low rates and the equity that has accumulated in recent years to get rid of FHA mortgage insurance premiums.

Each of the past 14 vintages (loans originated from 2005 to 2018) have seen their prepayment speeds increase over the last two months. The increase varies from 7 percent in the 2006 vintage to 109 percent among loans originated last year. The vintages with the highest prepayment rates all correspond to years with relatively high average interest rates.

In general, borrowers with higher credit scores have seen a much more notable increase in prepayment speeds than those with lower scores. Black Knight offers several explanations. Higher scoring borrowers not only tend to be more reactive to rate movements but also to carry higher balances, reducing the payback timeline on a refinance. Those with low scores, under 620, had prepay rates of 22 percent in February and 17 percent in March compared to 29 percent and 47 percent respectively for the highest scoring borrowers. Black Knight says a large share of the under 620 cohort has long had an interest rate incentive to refinance but has not done so, "suggesting much less rate movement impact among this group."

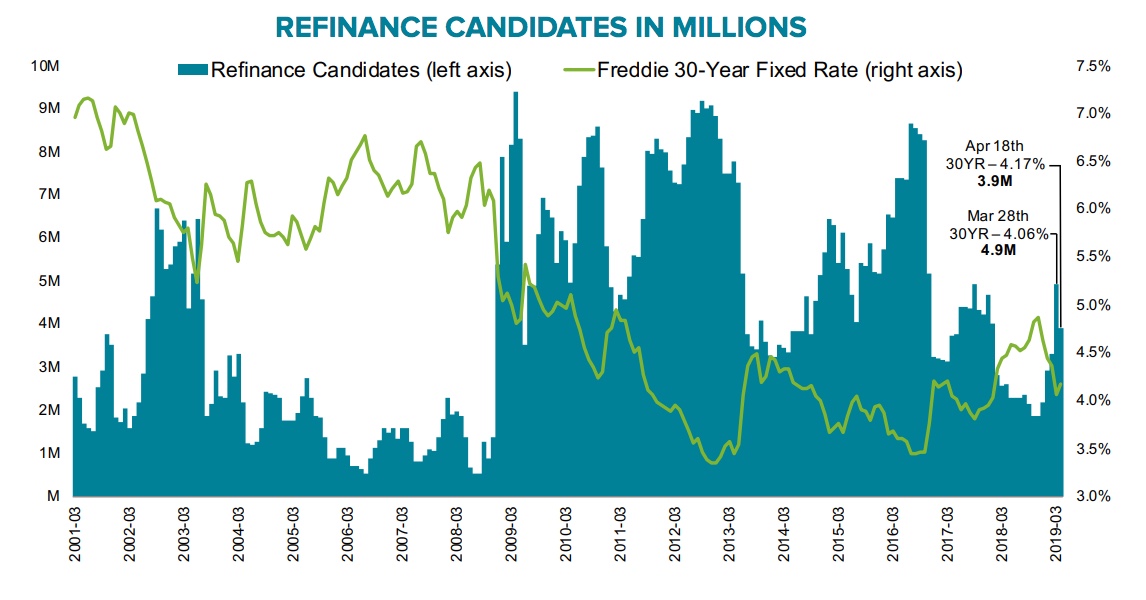

Black Knight regularly assesses the effect of interest rates on the pool of homeowners who might both qualify for and benefit from refinancing when rates change, and they do so again this month, but largely from the aspect of servicer retention rates. That is, after refinancing (or a home sale and purchase of another home) what percentage of borrowers return to their prior servicers.

The report looked at the refinance pool as of April 18 and found that 3.9 million borrowers with 30-year fixed-rate mortgages could qualify for refinancing and drop their rate by at least 75 basis points by doing so. That was down from 4.9 million less than a month previously, even though rates had risen by less than one-eighth of a percent. Black Knight says rates below 4.0 percent dramatically increase the incentive to refinance, while rates near and above 4.25 percent can cause that incentive to evaporate quickly. Small changes in rates create an outsized impact. This is because years of low rates means a steady decline in the number of borrowers who would benefit as rates move above 4.375 percent. Black Knight sets the current cutoff for refinancing incentive at 4.875 percent.

About 405,000 borrowers with loans originated in 2018 could likely qualify for a refi and save at least 75 basis points by doing so. This number was as high at 600,000 less than a month earlier when the rates recently dropped to an average of 4.05 percent.

Borrowers with loans originated in 2018 have an average interest rate roughly three-quarters of a percent higher than the market average and that cutoff point mentioned above is right at the edge of the largest distributions of 2018 vintage loans, making them noticeably more rate sensitive than the market as a whole. This represents not only the risk of premature runoff of recently originated loans, but also an opportunity for servicers to market to a lot of borrowers with a high incentive to refinance.

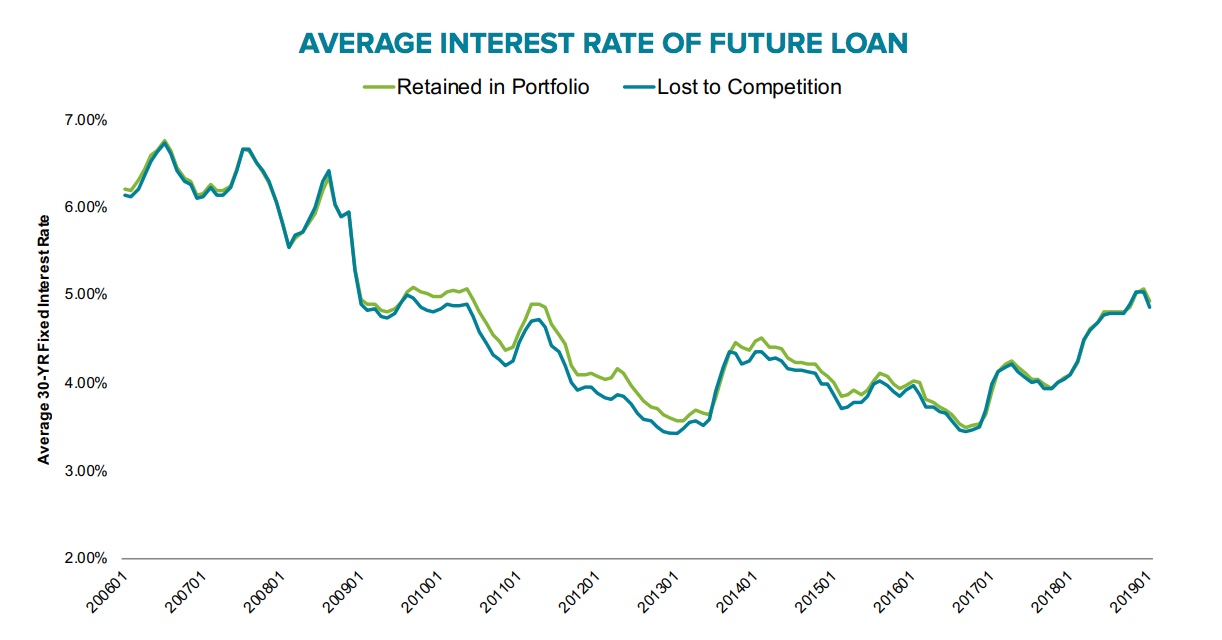

Servicers retained less than 18 percent of the loans in their portfolios that refinanced in the first quarter of 2019. Black Knight's Data & Analytics Division President Ben Graboske explains that this is the lowest retention rate since the company began tracking it 2005. "Anyone in this industry can tell you that customer retention is key - not only to success, but to survival," he says. "The challenge is that everyone is competing for a piece of a shrinking refinance market, the size of which is incredibly rate-sensitive, and therefore volatile in its make-up.

"Just a month ago, we were reporting that recent rate reductions had swelled the population of eligible refinance candidates by more than half in a single week after hitting a multi-year low just a few months before. Then, with just a slight increase in the 30-year fixed rate - less than one-eighth of a point - 1 million homeowners lost their rate incentive to refinance - almost 20% of the total eligible market.

"This is critical" Graboske continue, "because refinances driven by a homeowner seeking to reduce their rate or term have always been servicers' 'bread and butter' when it comes to customer retention. Offering lower rates to qualified existing customers is a good, and relatively simple, way to retain their business. Unfortunately, the market has shifted dramatically away from such rate/term refinances. In fact, nearly 80% of 2018 refinances involved the customer pulling equity out of their home - and more than two-thirds of those raised their interest rate to do so. Retention battles are no longer won - or lost - based on interest rates alone."

As evidence of this analysis, at the market's bottom in 2012 when a servicer lost a borrower to the competition, that borrower received, on average a ~0.25% better rate than those the servicer kept.. In 2008, there was little difference in the rates of those the servicer lost and the ones it retained.

As Graboske says, "A simple 'in the money analysis' doesn't provide the insight necessary to retain customers and can't take the place of accurately identifying borrowers who are likely to refinance and offering them the correct product. Rather, understanding equity position - and the willingness to utilize that equity - is key to accurately identifying attrition risk and reaching out to retain that business."