The Federal Housing Finance Agency reports that the two government sponsored enterprises (GSEs) Fannie Mae and Freddie Mac might together require government assistance of as much as $157.3 billion in the event of an extremely severe economic downturn. The figure comes as a result of a stress test mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act for certain financial institutions with more than $10 billion in assets, criteria which includes the two companies which are in Federal conservatorship.

The test, an annual requirement, is designed to determine whether an institution can absorb losses as a result of hypothetical adverse economic conditions. The Severely Adverse Scenario involves a deep and protracted recession in which unemployment increases by 4 percentage points from the beginning of the test horizon to a peak level of 10 percent by the middle of 2016. The real GDP declines by 4.5 percent from its beginning point to the end of 2015 and begins to recover in 2016. Short-term interest rates remain near zero though out the period and long-term rates drop significantly to 1 percent in the 4th quarter of 2014. Other conditions prevail such as a fall in equity prices of 60 percent and of home prices by 25 percent.

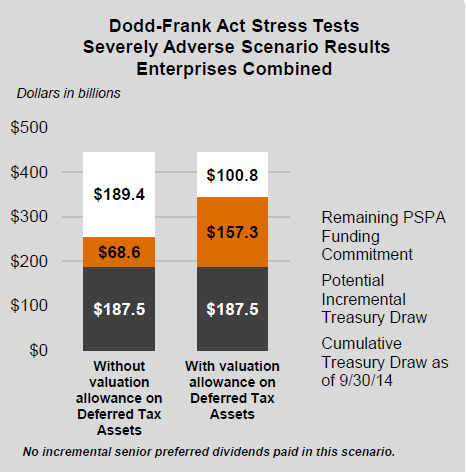

For the GSEs the combined projected credit losses under the scenario would be $43 billion, $24.9 billion for Fannie Mae and $18.1 billion for Freddie Mac. This represents 92 percent of their combined portfolios. Total projected comprehensive losses have a considerable range, between $73.4 billion and $162.1 billion depending on whether or not the GSEs reestablish a valuation allowance on deferred tax assets.

As of September 30, 2014 the GSEs have drawn a combined $187.5 billion from the Treasury under the terms of the Senior Preferred Stock Purchase Agreement (PSPA) negotiated when the they were placed into Federal Conservatorship and renegotiated in 2012. The remaining commitment under the agreement ranges between $189.4 billion and $100.8 billion depending again on the treatment of deferred tax assets.

Under the Severely Adverse Scenario the GSEs, which under the terms of the renegotiated PSPA the GSEs are not permitted to rebuild capital, would require incremental Treasury draws between $68.6 billion and $157.3 billion depending again on the tax treatment.