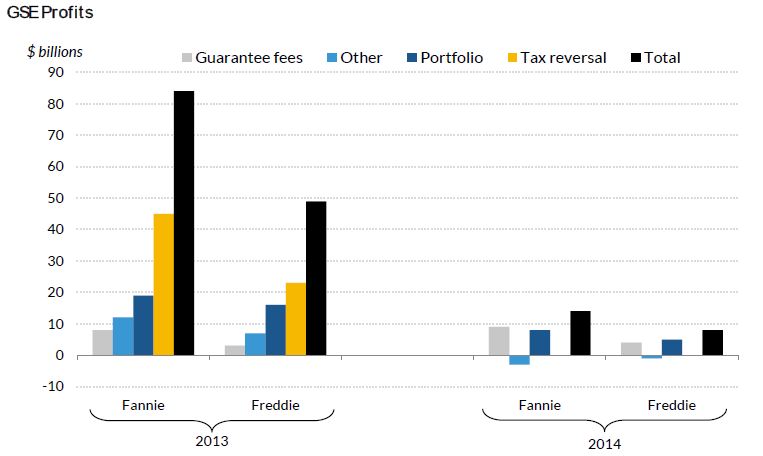

In 2013 Fannie Mae and Freddie Mac (the GSEs) both essentially bankrupt five years earlier, posted huge profits. For Fannie Mae it was $84 billion and Freddie Mac $49 billion. Both of course disclosed that much of the profit was the result of reclaiming tax assets written down during the crisis that led to their being put in government receivership in 2008. Those one-time adjustments reaped $45 billion for Fannie Mae and $23 billion for Freddie Mac.

Still it was a spectacular year for the GSEs, and in an brief written for the Urban Institute, Jim Parrott, a senior fellow at the Institute and owner of Falling Creek Advisors says talk around Washington "began to shift from winding them down to releasing them from conservatorship, taking much of the wind out of the sails of the already flagging push for overhauling the housing finance system. All reform involves risk, after all," Parrott said, "and these numbers suggested that we were risking an increasingly healthy system."

Then came 2014 and the GSEs' earnings plummeted. Fannie Mae reported a net of $14 billion and Freddie Mac $8 billion. Even more alarming, Parrott says, were Freddie's fourth quarter profits which were 90 percent lower than those of the third quarter. So now the talk shifted to whether the smaller of the two companies might soon need another draw on the U.S. Treasury.

Parrott, in his article What to Make of the Dramatic Fall in GSE Profits, says to understand what happened one must parse the 2013 figures. First, on top of the effects of the massive tax adjustments, significant amounts of income came from legal settlements arising out of bad loans sold to the GSEs prior to the housing crisis. Parrott says the exact amounts that come from this source are difficult to decipher as the moneys are dispersed among several larger revenue streams.

Finally, between a quarter and a third of the companies' profits came from the GSE portfolios; Fannie earned $19 billion and Freddie took in $16 billion. But Parrott says both of the latter sources of income are also finite; each institution is nearing the end of litigation arising from the housing crisis and their portfolios are being wound down under the terms of the Senior Preferred Stock Purchase Agreements with the Treasury.

This leaves them with only one enduring major revenue source, their core guarantee business through which they collect a fee in exchange for guaranteeing loans sold to investors. "In essence, what we're seeing - and will continue to see - is a steady decline of several large but ephemeral sources of revenue, forcing the GSEs to rely increasingly on their guarantee business for t heir profit s," he says.

Tightened post-crisis underwriting standards have improved the quality of the loans the GSEs guarantee and they also hold market dominance at present but Parrott says this guarantee fee (g-fee) revenue stream, while strong by historic standards, "represents a completely different level of profitability than we saw back in 2013." If all non-guarantee fee earnings are stripped away from those 2013 earnings Fannie would have made about $8 billion ($12 bill less taxes at 33.8 percent) and Freddie's profits would be $3 billion ($5 billion taxed at 32.6 percent.). This he says is not bad, "but a far cry from $84 billion and $49 billion."

Of Fannie Mae's $14 billion and Freddie Mac's $8 billion 2014 profit guarantee fees contributed $9 billion ($14 billion taxed at 32.8 percent) and $4 billion ($5 billion taxes at 30.1 percent) respectively. The remainder came from investments on their portfolio and other net income. Freddie's income from investments was notably lower than in prior years because of its shrinking portfolio but also because the company took a large loss on a derivative position it used to hedge portfolio risk.

This is an accounting rather than an economic loss as Freddie was required to mark-to-market its derivative positon but not the portfolio position it was attempting to hedge. Thus it had to report a loss in the value of the former position but not the gain it offset, an accounting loss that will likely reverse as interest rates rise. The improved derivative positon will cushion upcoming profits over the near term and forestall the economic reality of more modest earnings as the company begins to rely almost entirely on g-fee revenue.

So what about the possibility that Freddie Mac may need to draw against its Treasury line of credit, something neither GSE has done since 2012? Under their revised PSPAs, each GSE must pay all of its profits above a buffer amount to Treasury in the form of a dividend and the GSE is determined to need a draw when its losses exceed that capital buffer which is $1.8 billion for each in 2015. Those buffers decline each year by $600 million until extinguished in 2018. The buffer declines in sync with the GSE portfolios because the volatility in earnings the buffer is designed to protect will diminish with the portfolio investments.

Parrott says several factors should "shore up" Freddie Mac's revenue near term and decrease the likelihood of the GSE needing a draw.

- As mentioned above, previous accounting losses from its derivative position will likely reverse as interest rates rise.

- Freddie will retain a significant portfolio for the next couple of years.

- Freddie's older loans with lower g-fees will be gradually replaced by newer loans with the higher current fees. As long as the company retains a dominant market share this will mean an increase in revenue.

Things however will get trickier in the out years. When the private-label securities market finally recovers Freddie's market share will decrease and so will its g-fee revenue. Also, if the company opens its credit box it will be exposed to higher risk and, depending on how well it manages that risk, to more volatility in earnings. Without the ability to offset those losses with gains from portfolio investments it will be increasingly exposed to economic conditions and its risk of a draw goes up.

Parrott says that not much will actual happen if Freddie Mac does require a draw. It has $140 billion remaining on its line of credit and if it should draw down on that line fast enough to give investors cause to worry that the line might be exhausted during the life of their investment they will demand a discount to cover their risk. "If that happens, then Freddie's already precarious financial situation is likely to get a lot worse, and quickly."

But Parrott discounts that possibility, saying it would take some very big draws to reach that point - "likely either a dramatic draw or two that suggests more to come, or years of more moderate ones. Either way, we are a long way off from that kind of environment." He sees more likelihood of a political impact from a draw - that "Congress may finally wake up (once again) to the unsustainability of the current system, and begin negotiating steps to overhaul it, perhaps with enough external pressure this time to see it through."

He concludes that, if the only problem to be addressed as some think is the risk of a draw then the logical response is to allow Freddie and Fannie to rebuild a capital buffer to protect against that risk. However as they each garner increasingly modest profits it appears that rebuilding a buffer would be gradual at best. In addition the Obama Administration is determined that there will be no effort to recapitalize the institutions unless basic reform is part of the equation. Parrott says he will discuss that position and its implications in the future.