As more time elapses since the three hurricanes that impacted parts of the U.S. in late summer to mid fall, additional damage to the mortgage market is becoming apparent. The focus of Black Knight's Mortgage Monitor for December, as well as its recap of mortgage performance in 2017, is skewed by those weather events.

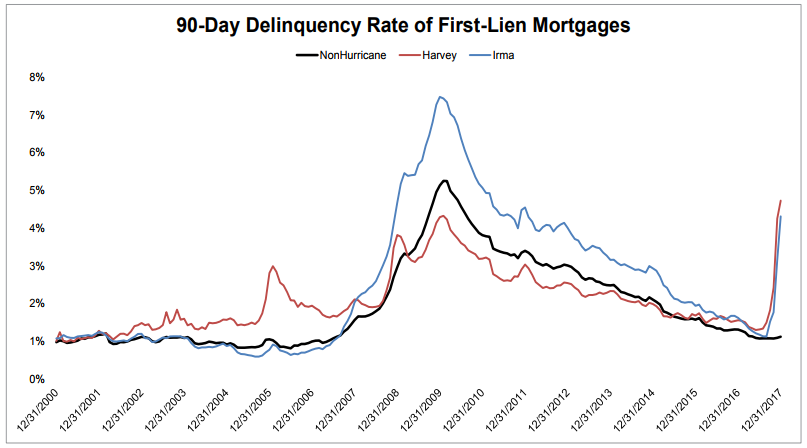

The performance of mortgages overall continued to improve in 2017. Mortgage delinquencies in non-hurricane affected parts of the country, areas outside of the Texas Gulf Coast, Florida and the eastern portion of Georgia, were down 11 percent from long-term norms. But factor in those areas hit by Hurricanes Harvey and Irma and the 164,000 additional delinquencies pushes the rate to a 23-month high.

Early stage delinquencies attributed to the hurricane have actually begun to decline. The usual seasonal effect on 30-day past due mortgages was felt in December with a 124,000-loan increase in non-disaster areas which were offset by a 35,000 decline in the storm sites. However serous delinquencies attributed to Irma and Harvey have increased fourfold over the past two months. As of December, over 80 percent of borrowers who were still behind on their mortgages are now 90 or more days past due and those borrowers account for 20 percent of all such seriously delinquent loans.

Black Knight Data & Analytics Executive Vice President Ben Graboske explained, "Hurricanes Harvey and Irma significantly impacted 2017 mortgage performance metrics. When Black Knight isolated non-hurricane-impacted areas - which represent 90 percent of the entire active U.S. mortgage universe - we see the national delinquency rate actually fell to 11 percent below long-term norms. Likewise, the 90-day delinquency rate was also up six percent from last year, with roughly a third more seriously delinquent loans than we'd expect in a healthy market. Excluding the hurricane impact, though, we see that there were 84,000 fewer loans 90 or more days past due than last year; a 14 percent reduction."

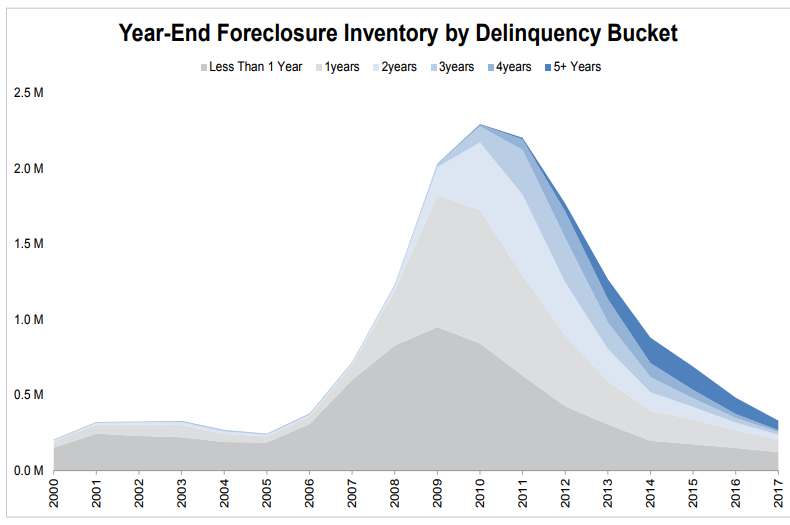

The hurricanes are recent enough, that coupled with the moratoria put into effect by major lenders, foreclosure statistics are not yet showing any storm related effects. There was a total of 649K foreclosure starts initiated in 2017, the fewest of any year since 2000. Many starts were repeats and foreclosures that were initiated for the first time on a property fell by 15 percent from 2016's levels to be the fewest on record and roughly half their pre-housing crisis annual average.

As of December, the national delinquency rate, even with the hurricane effects factored in, was 4.71 percent, 4.0 percent below the pre-crisis average. The foreclosure inventory continued to improve and may actually have been helped by the hurricane moratoria. The inventory ended the year at 0.65 percent, with just over 331,000 loans in active foreclosure. That is 150,000 fewer than at the end of 2016, and just 2.0 percent above long-term norms.

Within that inventory are a large number of cases that remain from the foreclosure crisis. More than 125 active foreclosure have had no payments made for more than two years and for almost 64,000 the delinquencies have extended more than five years. Graboske noted that, while the inventory of loans in active foreclosure is on track to normalize this year, the number of aged loans could delay that happening.

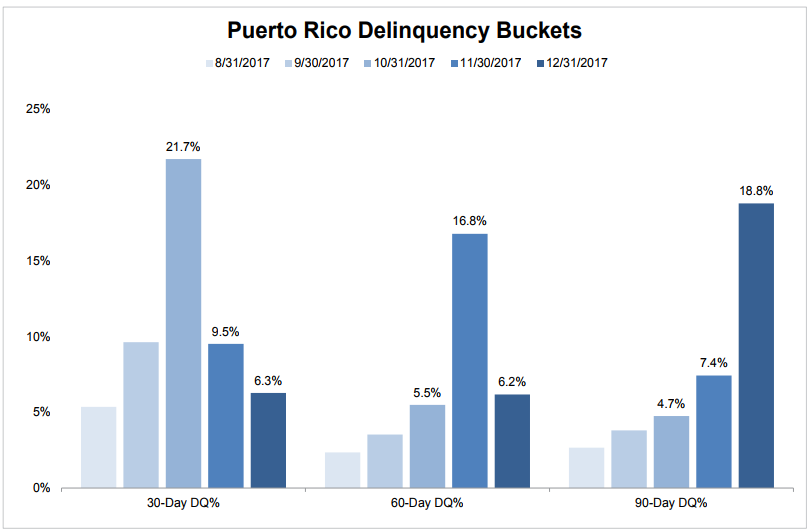

Little has been mentioned elsewhere about the Hurricane Maria's effects on Puerto Rico. Black Knight looked at those as well and, while they appear to have peaked, they are still severe. As of December, 34 percent of first mortgages in the territory are delinquent to some degree. This is down from 37 percent in November. An estimated 84,000 mortgages are past due and, while early delinquencies are returning to normal, serious ones spiked in December. About 68,000 of the non-current tally are now more than 90 days past due.

The hurricanes also affected the performance of 2nd liens, both home equity loans and HELOCs, i.e. Home Equity Lines of Credit. Black Knight found nearly 10 percent of active loans of one of the other type are located in the disaster zones, principally in Florida.

What the company called "noticeable jumps) were seen in the number of past due loans although the affect is not as strong or wide-spread as the impact on first liens. In the areas hit by Irma the share of past-due HELOCs increased from 3.2 to 4.4 percent between July and November HELOCs. Home equity loans were hit harder, jumping from 7.2 percent to 10.7 percent.

In the Harvey zone, the non-current rate of equity lines rose 79 basis points (bps) to 1.9 percent and for loans increased by 378 bps to 11.8 percent. In total, the two storms appear related to the delinquency of 17,200 second liens.

Hurricanes aren't the only factor that Black Knight sees affecting the home equity loan market. One that will impact borrowers who itemize is the revised treatment of the mortgage interest deduction (MID). The extent depends on whether the borrower has an equity loan or a HELOC.

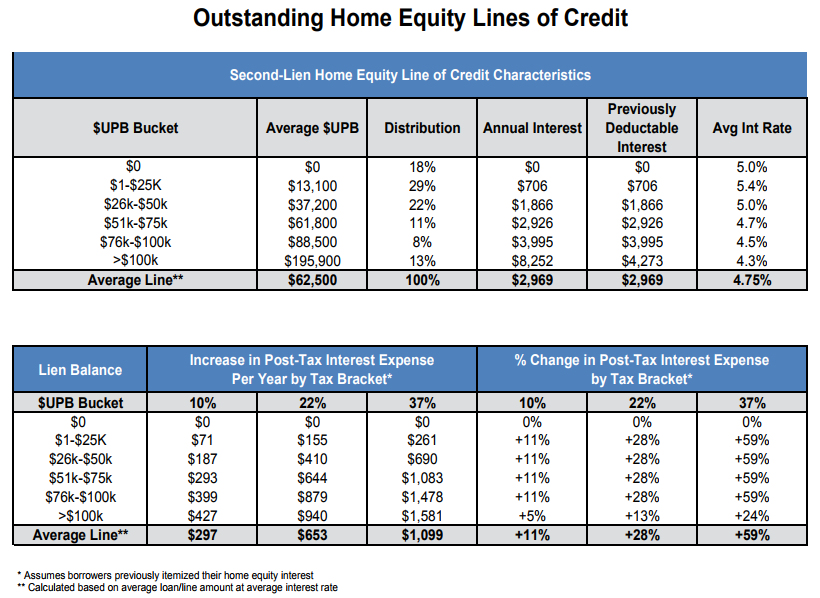

The average HELOC borrower carries a balance of $62,500 with a 4.75 percent rate and will pay $3,000 in interest in 2018. In past years that borrower would have been able to recoup between $297 and $1,099 depending on tax bracket using the MID. Under the new tax plan those amounts are no longer recoverable. For those in the lowest tax bracket the increase could be as little as 11 percent. For those with higher incomes, likely to also correspond to higher loan balances, the increase in post-tax expense could be as high as 59 percent, as much as $1,500 for those with balances above $100,000 and in the highest bracket.

On the home equity loan side, the balances tend to be lower, but interest rates are higher, 7.4 percent on average. These borrowers will see a slightly smaller increase by dollar amount than HELOC borrowers, but the percentage increases are identical.

Will the resulting higher taxes push borrowers to prepay their loans or will it cause any additional default risk? Black Knight considers the latter unlikely and sees several factors that could lesson the propensity to prepay, something which would be more likely among those with significant funds to do so.

First, monthly payments won't change due to the tax law, but given the age of most HELOCs, more than half were originated prior to 2008 and one third between 2005 and 2007, most have recently reset. This means the payments changed from interest only to interest plus principal, generally doubling the monthly obligation. Black Knight says it is reasonable to presume that borrowers with the means to pay off their lines would have been prompted to do so by those resets.

Still, over 7 percent of equity lines, some 700,000 in total, will reset this year. This, the company says, will have a significant impact on prepayment rates.

A second analysis looks at the benefits of a cash-out refi versus a HELOC under the new tax plan. The math, the company says, is dependent on a multitude of factors and the example given in the table illustrates "only one slice of a more complex pie." The complexity and the many factors that must be considered suggests that the tax changes will only alter the behavior of savvy borrowers.

That said, borrowers with lower first mortgage balances who want to extract equity may do better with cash out refinances. For some of them, the tax incentives now outweigh the likely increased interest rates they will face. As interest rates rise, the balance swings back toward HELOCs as a more economical choice.