In stark contrast to the week just passed, the week ahead offers no auction supply and a light schedule of economic data, which leaves investors to focus on the FOMC Minutes and a steady drip of Federal Reserve speakers.

Key Events This Week:

Monday:

9:05 - Dennis Lockhart, president of the Atlanta Fed, speaks on the economy and monetary policy to the International Economic Forum of the Americas' Palm Beach Strategic Forum in West Palm Beach, Florida.

9:05 - Federal Reserve Bank of Chicago President Charles Evans speaks on "The Role of Government in Financial Literacy" before the Money Smart Week Chicago Financial Literacy & Education Summit, No Q&A. No

discussion of current economic conditions or monetary policy.

3:15 - Federal Reserve Bank of Chicago President Charles Evans discusses economic conditions and monetary policy issues in live interview on CNBC's "Closing Bell"

7:15pm - Ben Bernanke, chairman of the Federal Reserve, speaks to the Atlanta Federal Reserve Bank Financial Markets Conference in Stone Mountain, Georgia.

Tuesday:

8:25 - Dennis Lockhart, president of the Atlanta Fed, provides welcoming remarks at the bank's Financial Markets Conference in Stone Mountain, Georgia.

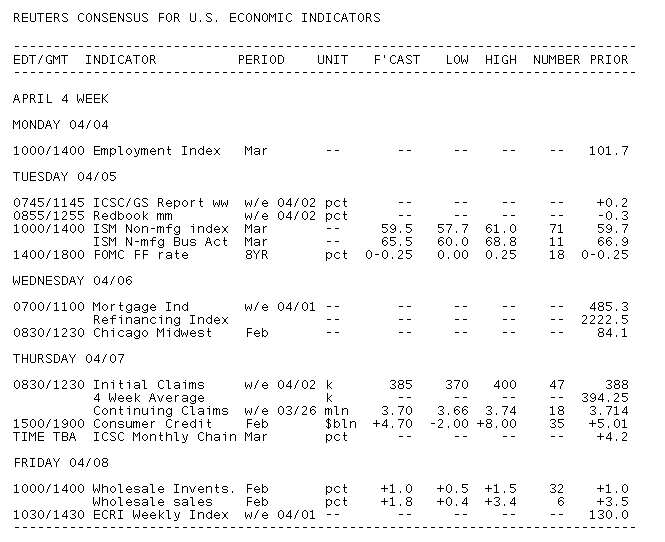

10:00 - Economists polled by Thomson Reuters forecast the ISM Non-Manufacturing Index to remain steady at a vigorous 59.7 in March. The index, which measures the services, financial, and construction industries, was previously at its highest level since the summer of 2005. It also shown expansion for 15 straight months and increased its pace for the last six. The important employment component may be ignored given that the nonfarm payrolls report has already come out, but last month it kicked up to 55.6, the strongest since April 2006.

"Various cross-currents suggest that the ISM index for services industries should inch up to 60.0 in March," said analysts at IHS Global Insight. "Business activity remained at solid levels, and freight volumes picked up in the first quarter, while financial market conditions were less buoyant. Orders pulled back slightly."

12:45 - Narayana Kocherlakota, president of the Minneapolis Fed, delivers welcoming remarks at a Minneapolis Fed workshop on homeownership.

1:30 - Charles Plosser, president of the Philadelphia Fed, moderates a panel on weathering the financial crisis at the Atlanta Fed's Financial Markets Conference in Stone Mountain, Georgia.

2:00 - The FOMC Minutes from the March 15 meeting will be closely looked at by Fed watchers, but others should be fine paying attention to the many speakers on the circuit this week. Several of them - Bullard, Fisher, Kocherlakota, Lacker and Plosser - have been musing recently about an early end to QE2 and a mid-2011 hike in the Fed Funds rate, according to economists at BMO Capital MArkets.

"The Minutes will be scoured for any clues to the timing of any potential shift in Fed policy," BMO said.

The last Fed statement kept policy unchanged but revised its language on severa fronts. Economists at Nomura Global Economics pointed out these themes at the most important:

(1) brighter economic outlook;

(2) more attention to inflation.

"The more positive language on the labor market 'improving gradually' and the economic recovery being 'on firmer footing' are essentially catching up," Nomura said.

"The minutes likely entail more detailed discussion on inflation and commodity prices. Moreover, the FOMC kept any discussion of the earthquake/tsunami in Japan, which occurred just 4 days prior to the March meeting, out of the press release; the minutes will almost certainly include some commentary on the potential economic ramifications."

Wednesday:

12:00 - Dennis Lockhart, president of the Atlanta Fed, delivers closing remarks at the bank's Financial Markets Conference in Stone Mountain, Georgia.

March MBS prepayment reports will be released on Wednesday afternoon

Thursday:

8:20 - Jeffrey Lacker, president of the Richmond Fed, speaks on innovation in a new regulatory environment at the 2011 Ferrum College Forum on Critical Thought, Innovation & Leadership in Roanoke, Virginia.

8:30 - After some holiday and seasonal volatility around the New Year, Initial Jobless Claims has been fairly consistent in reporting a downward trend in the last two months. Weekly claims for unemployment benefits have come in below 400k for three straight weeks and under under 420k for seven weeks. Last Thursday, claims fell 6k to 388k, leaving the 4-week average at 394,250. Economists anticipate 385k for the final week of March.

Last week's survey also showed the number of people continuing to receive claims fall by 51k to 3.714 million - the lowest since October 2008.

3:00 - Consumer Credit began 2011 by rising $5 billion, a fourth straight gain indicating that households were continuing to pay off debt and staying away from excessive new obligations. A consensus forecast wasn't available for the February survey, but economists at BBVA look for a $2.4 billion uptick.

"Given the strong vehicle sales we expect that non-revolving loans which includes auto loans and student loans probably increased at a solid pace in February," said economists at Nomura. "However, weakness in ex-auto consumption is expected to feed into a decline in revolving loans in the month."

11:00- Treasury announces the terms of 3-year, 10-year, and 30-year debt auctions to be held in the following week

Friday:

8:00 - Dennis Lockhart, president of the Atlanta Fed, speaks on the economy and monetary policy to the University of Tennessee's Knoxville Economics Forum in Knoxville.

10:00 - Wholesale Inventories rose 1.1% in last month's report for January, a better-than-anticipated gain led by durable goods accumulation and a price effect from higher commodity prices on nondurable goods. February is expected to post another increase, albeit at a slower pace more in the range of +0.6%.

"The latest report indicates that wholesale inventories have increased by 0.9% on average month-over-month since the end of 2009," said economists at BBVA, citing the Census Bureau. "In February, wholesale inventories are expected to continue increasing due to a relatively low inventory-to-sales ratio. We expect that wholesalers will continue to replenish sold inventory in 2011 and the ratio will converge to its historical average of 1.25."

MND's latest mortgage rate guidance. From: How Did the Employment Report Impact Mortgage Rates?

"It would have been convenient if the Employment Situation Report left markets with a renewed sense of purpose and momentum but unfortunately, we’ve only been offered more uncertainty (we say “more” because a traditionally influential piece of economic data failed to move the markets). While that makes it harder to predict the future, it does little to change our guidance. If you've got time, flexibility, or otherwise are not in any particular rush or pressing need to lock your loan, we still think it's possible that rates make one more run lower in the months ahead. If you can't afford or don't want to take a risk, lock now because it might not get any better from current market again."