Yesterday, we discussed why rates are not actually at all-time lows. But rates are whatever they are. They're relation to previous lows doesn't really matter at the end of the day. Do you benefit from refinancing? Can you afford your new purchase payment? Great! Don't worry if the rate is technically not an all-time low. I'm just on a crusade for journalistic accuracy, shouting at my own little wall over here.

More important than the outright level of interest rates is the risk of volatility on the horizon. With everything the economy and financial markets have been through in 2020, the past few months have been surprisingly calm in the bigger picture--especially for the bond market (which has a direct bearing on mortgage rates). But there are several reasons we should be prepared for more volatility ahead.

Election. The US presidential election is weeks away. First off, this always has potential to cause market volatility. Moreover, markets seem to be getting in position for bigger movement. Both stocks and bonds are at the same levels seen in early September, and both have been flat in the bigger picture since then. Even without the election, that flatness tends to precede volatility.

Covid at home. Covid-related news is ongoing, of course. Markets continue to show a willingness to react to significant changes in case counts, vaccine trials, new treatments, mortality, and the anticipated economic effects of all of the above. Winter is coming, and we're about to learn 'something' either way. If the fight against the pandemic goes better than expected in the coming months it implies significant upward pressure on rates.

Covid abroad. Europe is arguably entering a new covid crisis. This has been helping the US bond market rethink its recent efforts to push toward higher rates.

If the situation continues to spiral, it should continue to help bonds, but only as a supporting actor. US bonds have already proven more than capable of marching to their own beat, post-covid.

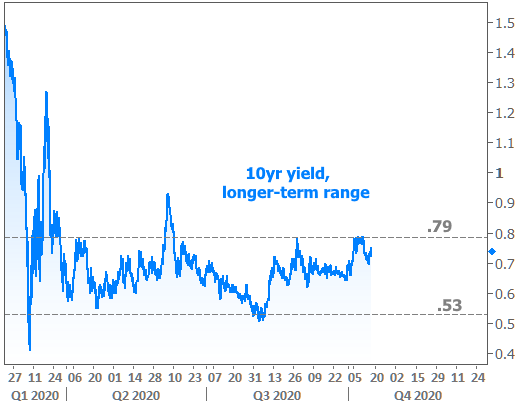

Stocks, Bonds, Technicals! 10yr Treasury yields broke out of a shorter-term range this week. They added emphasis to that breakout by failing to get back into the previous range despite several attempts this week. In other words, they bounced at 0.72 as a floor after it had been a ceiling more often than not in the past few months.

Such behavior often implies additional momentum toward higher rates, but importantly, there is a longer-term range that remains unbroken.

Stocks were on a tear before the big sell-off in early September (the one that seemed to help bonds calm down and remain in the shorter-term range). Stocks haven't made it back to recent highs. Now, both sides of the market seem to be consolidating--circling the wagons, if you will--in preparation for their next move. The timing of the presidential election and the anticipation for an impending stimulus deal are no coincidence, but markets may not be able to wait that long to make a move.

In the chart below:

1) the big stock sell-off that helped bonds calm down

2) stocks and bond yields moving higher together, but no higher than they have been in recent months.

Any Caveats?

Yes! Let's talk about one! With all of the above out of the way, there's at least one great reason to expect slightly less volatility in mortgage rates relative to the broader financial market. The reason is also very simple. Mortgage rates may be very low, but they haven't fallen remotely as quickly as their long-time companion and guidance giver: US 10yr Treasury yields. Most of the time, 10yr yields and mortgage rates look like the left side of the following chart. Things obviously changed post-covid.

What this means is that the mortgage market has some room to "soak up" a certain amount of weakness in the broader bond market. The more gradual the weakness is, the easier that would be. If 10yr yields are spiking significantly, don't expect mortgage rates to just take it in stride. But if yields are slowly working their way up from .75% to 1.0% in the coming months, it wouldn't be a huge surprise to see mortgage rates hold relatively sideways.