Mortgage-backeds are off to a slow start to the week. Not much activity to report. Price levels are nonetheless moving higher thanks to a turnaround in benchmark Treasuries, tighter swap spreads and modest buying in MBS space.

The November delivery FNCL 4.0 is currently +0-08 at 102-18. I've got the production MBS coupon marked at 3.625%, 3.2bps lower than it was on Friday afternoon. Yield spreads are slightly tighter to TSYs and swaps, but just barely. Firmer MBS yield spreads in the face of lower TSY yields and tighter swap spreads implies the few trades that have printed in the TBA market have been buy tickets. This would make sense from a tactical perspective (short term) ahead of $100 billion in TSY coupon issuance ($36 BLN 2-YR NOTES TODAY, $35 BLN 5-YR NOTE TOMORROW, $29 BLN 7-YR NOTES WEDNESDAY).

Our technical guidance continues to play a pivotal role in price movement. The FNCL 4.0 touched 102-20 before positive progress was stopped out.

Some source the underlying motivation for this modest reversal in rates back to a speech given by Fed Chairman, Ben Bernanke, on Friday evening. I could only find one obviously dovish comment, "although financial markets are for the most part functioning normally now, a concerted policy effort has so far not produced an economic recovery of sufficient vigor to significantly reduce the high level of unemployment.”

Combined with the FOMC's latest official communication, it sounds like the Fed is trying to tell us they are losing control over the crisis and are now thinking about taking unconventional measures to fight it. I discussed some of the potential reasons why the FOMC would need to shock the confidence of the system with the announcement of another asset purchase program or unconventional policy measure (housing market specific). Bernanke actually used the majority of his prepared statement to explain why economics and the application of economic theory have changed and how these shifts have impacted the perceptions of market watchers. It's long but worth a read. HERE it is.

The major concern is that the Fed has pushed interest rates to record lows, yet consumers would still rather save instead of invest or consume, regardless of the perceived high opportunity cost of saving (low rates). Notice I said "perceived" high opportunity cost. Main Streeters are saving because they are too nervous to invest or spend money on goods that are not necessities. We are not out of the woods yet and people want to be prepared for the worst case scenario.

I can point toward a couple other reasons why TSYs would be rallying, fundamentally at least. Three credit unions were shut down on Friday (READ MORE) and the Chicago Fed's National Activity Index, which flashed at 8:30am, are both potential catalysts. Here is an excerpt from the CFNA release:

"Led by declines in production- and employment-related

indicators, the Chicago Fed National Activity Index decreased to –0.53

in August from –0.11 in July. None of the four broad categories of

indicators that make up the index made a

positive contribution in August."

But that was August and old news for the most part. The credit union story reflects more BIG PICTURE weakness and it worth a raised eyebrow. I would rather lean on the bargain buying crutch as the culprit though. Just like MBS, the TSY market has been slow to get going, so more than anything it seems like a lack of sellers have allowed a few buyers to push prices higher and yields lower. I bet those buyers are focused in the Far East, where market participants were out for most of last week. Asian accounts have been a strong source of range support, so this would also make sense.

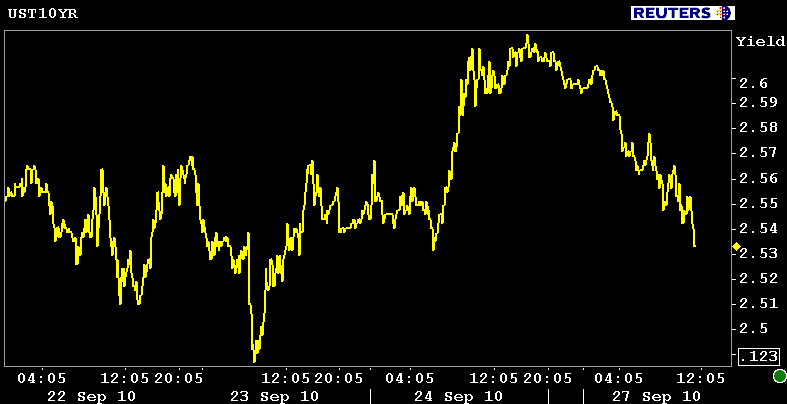

With debt supply focused on the short end of the yield curve, the long end should be outperforming the front end of the yield curve, which is exactly what is playing out this AM. The 2s/10s curve is 6bps flatter at 210bps and the 2s/30s spread is 6 bps tighter to 329bps. The 10 year note is +21/32 yielding 2.531% (-7.5bps).

10s basically rallied all night.

Benchmark 10s have room to rally as far as 2.50% before profit takers really re-emerge. Rate sheet influential MBS coupons have demonstrated a clear disdain for further positive progress as the November delivery FN 4.0 has approached the 103 handle. There is a ton of Fed speak on the schedule this week. Expect investors to be listening for any hint of another Quantitative Easing program, which would be mortgage rate supportive. On the other hand, a lack of scheduled econ data in first half of the week will make it easier for bond traders to price in Treasury debt supply concessions. This would push benchmark yields higher but MBS should be somewhat sheltered from that (see comments above).

On the mortgage rate front, lenders were busy adding pipeline protection last week (selling MBS forward). If secondary added too much coverage, lock desks will either be looking to buy the market via aggressive loan pricing. They could also just let MBS prices plummet and pair off at the price lows. Whatever happens first...right now the former seems more likely. How is your pricing this morning?