To put it bluntly, not good...

Home loan borrowing costs moved higher after a better than expected jobs report this morning. The one-week winning streak that led mortgage rates back into historically low territory came to an end as a result. While economic growth seems to have stalled, this data tells us the economy isn't in free-fall mode. RECAP

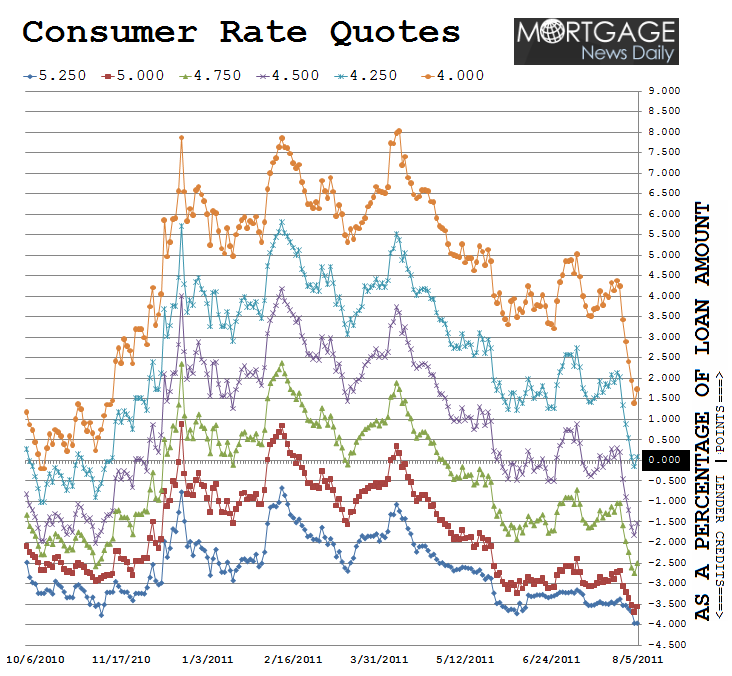

In the chart of Consumer Rate Quotes below, if the note rate line is moving up, the closing costs associated with it are on the rise. If the note rate line is moving down, costs are on the decline. Consumer borrowing costs moved sharply lower every day this week, that is before today when a small portion of positive progress was given back. Considering the size and speed of the mortgage rate rally, this reversal wasn't so bad. It still pushed borrowing costs higher though. If you locked your loan yesterday, congratulations, you took advantage of the best mortgage rates since early November 2010.

The chart above compares the average origination costs (as a percentage of loan amount) for several available mortgage note rates as quoted by the five major lenders. Each line represents a different 30 year fixed mortgage note rate. The numbers on the right vertical axis are the origination closing costs, as a percentage of your loan amount, that a borrower would be required to pay in order to close on that note rate. If the note rate graph line is below the 0.00% marker, the consumer may potentially receive closing cost help from their lender in the form of a lender credits. If the note rate line is above the 0.00% marker, the consumer should expect to pay additional points at the closing table to cover permanent buydown costs and origination fees. PLEASE SEE OUR MORTGAGE RATE DISCLAIMER BELOW

CURRENT MARKET*: The BestExecution 30-year fixed mortgage rate is 4.250%. Not many lenders are willing to offer 4.00% but 4.125% is available if you're willing to pay additional closing costs. On FHA/VA 30 year fixed BestExecution is 4.00%. Fewer lenders willing to quote 3.875% (includes additional closing costs). 15 year fixed conventional loans are still best priced at 3.75% and we're still seeing aggressive quotes at 3.625%. Five year ARMs are still best priced at 3.25. ARMs and 15 year quotes seem to have bottomed out.

It's important that we point out an increased amount of variation in what individual lenders are quoting as their BestExecution rates. This is a factor of price volatility in the secondary mortgage market. Unfortunately when volatility picks up in the secondary mortgage market, the cost of doing business gets more expensive for lenders (hedging costs go up). Those added costs are usually passed down to consumers via extra margin in rate sheets.

GUIDANCE: Our long-term mortgage rate outlook finally came true this week. And although borrowing costs rose today, we still believe mortgage rates have room to rally further, especially when considering that lenders have been slow to pass along gains this week. Recovering today's losses may take a few days or even weeks and the environment could get stressful, but our economic outlook remains supportive of a return to historic lows. We backed-up that perspective in this post: Bond Market Officially Repeats History. Reality Restored.

CAUTION: MND guidance is speculative in nature. We don't have

a crystal ball, we can't predict the future, we can only share our

outlook. Making the following considerations extra

important........................

What MUST be considered BEFORE one thinks about capitalizing on a rates rally?

1. WHAT DO YOU NEED? Rates might not rally as much as

you want/need.

2. WHEN DO YOU NEED IT BY? Rates might not rally as fast as

you want/need.

3. HOW DO YOU HANDLE STRESS? Are you ready to make tough decisions?

----------------------------

*BestExecution is the most cost efficient combination of

note rate offered and points paid at closing. This note rate is determined based

on the time it takes to recover the points you paid at closing (discount) vs.

the monthly savings of permanently buying down your mortgage rate by

0.125%. When deciding on whether or not to pay points, the borrower must

have an idea of how long they intend to keep their mortgage. For more info, ask

you originator to explain the findings of their "breakeven analysis"

on your permanent rate buy down costs.

*Important Mortgage Rate Disclaimer: The BestExecution

loan pricing quotes shared above are generally seen as the more aggressive side

of the primary mortgage market. Loan originators will only be able to offer

these rates on conforming loan amounts to very well-qualified borrowers who have

a middle FICO score over 740 and enough equity in their home to qualify for

a refinance or a large enough savings to cover their down payment and closing

costs.If the terms of your loan trigger any risk-based loan level pricing

adjustments(LLPAs), your rate quote will be higher. If you do not fall into

the"perfect borrower" category, make sure you ask your loan

originator for an explanation of the characteristics that make your loan more

expensive."No point" loan doesn't mean "no cost" loan. The

best 30year fixed conventional/FHA/VA mortgage rates still include closing

costs such as: third party fees + title charges + transfer and recording. Don't

forget the fiscal frisking that comes along with the underwriting process