If deteriorating stock market sentiment turns a corner this week, it's unlikely to be a function of optimistic data. The calendar of events is simply too light to drive a sustainable directional reversal. The schedule in the week ahead includes much Fed-speak, an anecdotal review of economic developments around the country and the Monthly Treasury Budget Statement. Besides those planned releases, Treasury will auction $66 billion in 3-year, 10-year and 30-year debt on Tuesday, Wednesday, and Thursday.

"Rate sheets look like they'll shed some basis points as the week begins on a negative note thanks to a short-term bias to sell bonds into strength in preparation for Treasury debt auctions", says MND's Managing Editor Adam Quinones. "Adding some confidence to that point of view, this price action is playing out regardless of continued weakness in global equity markets. Furthermore, trading activity was light in the overnight session as China, Hong Kong and Korea were out on holiday, leaving algorithmic models in charge of directionality. If given the opportunity these pre-programed quantitative trading models will be urging traders to sell bonds on overbought technical conditions in an effort to cheapen-up the yield curve before the auction process beings tomorrow (see steeper share of curve). With the Fannie Mae 30-year 4.0 MBS coupon down 6/32 we'd expect loan pricing to deteriorate anywhere from 10 to 25bps depending on how aggressive your lock desk left rate sheets on Friday." added Quinones.

The benchmark 10-year Treasury note yield is indeed moving higher to start the week, even as stocks fail to muster recovery rally momentum. 10s are currently -9/32 at 100-27 yielding 3.024%. 3.3bps higher from Friday's close.

The stock market looks to stumble further after five straight weeks of decline, including a 2.3% drop in the S&P 500 last week. S&P 500 futures are currently 0.25 points lower at 1,296. European equities are down about 0.70% after some weak data: the euro area producer price index rose 6.7% year-to-year in April, just higher than consensus forecasts of 6.6%, while Spain's industrial production index declined 1.6% year-to-year, following a 0.4% drop in March.

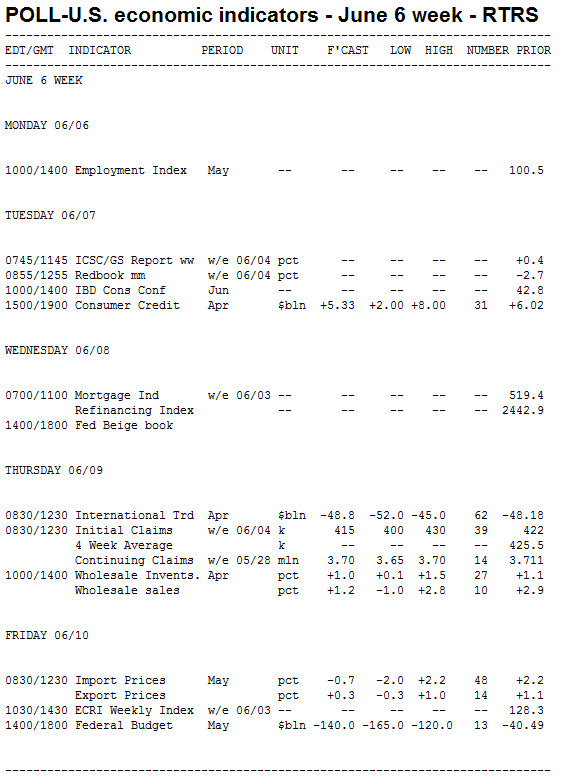

Key Events This Week:

Monday

No major economic data.

3:30am - Charles Plosser, president of the Philadelphia Fed, speaks on central bank post-crisis policy to Global Interdependence Center in Helsinki.

5:30pm - Richard Fisher, president of the Dallas Fed, speaks at a Market News International seminar in New York.

The May MBS prepayment report will be released on Monday afternoon.

Tuesday:

12:30 - Dennis Lockhart, president of the Atlanta Fed, speaks on the economic outlook to the Charlotte Economic Club, in North Carolina.

3:00 - Consumer Credit is anticipated to continue growing for the seventh consecutive month in April, following a series of crushing declines during the financial crisis. The consensus of economists look for a $5 billion expansion, compared with $6 billion and $7.6 billion gains in the prior two months. Forecasts range from $2 billion to $6 billion.

The March report was notable for its $1.9 billion increase in revolving credit - mainly credit cards - which marked just the second gain of the past 31 months, according to Nomura Global Economics.

"It appears that credit card volumes have likely bottomed, but given the increasingly conservative financial outlook of the average consumer and aging population demographics, we would expect any increase in credit outstanding to be limited to at most 75 - 80% of income growth," said economists at Janney Capital Markets. "That's the only way consumers will be able to reduce balance sheet leverage over time, and even that upper limit indicates a slow rate of leverage reductions."

According to IHS Global Insight, total consumer debt stood at $2.45 trillion in April, the same level as a year ago.

"The peak to trough loss in consumer credit between July 2008 and September 2010 was $187.0 billion," Global Insight noted last month. "Since then, consumer credit has rebounded $36.6 billion, or about 16% of the total loss. This is good news as it indicates that positive labor market developments and improving incomes are driving up consumer spending."

Janney notes that while financing incentives have tightened, a higher volume of auto sales should generate growth in consumer credit volumes.

"Consumer credit growth has resumed, reflecting an end to banks' hesitancy to lend and ... somewhat reduced consumer hesitancy to borrow," said analysts at Janney Capital Markets. "Even so, it appears that this improved demand for borrowing has been concentrated predominately in a single sector, namely auto lending."

3:45pm - Fed chairman Ben Bernanke speaks to the International Monetary Conference in Atlanta. Topic TBA.

9:00pm - Federal Reserve Bank of New York President William Dudley speaks before the Foreign Policy Association Corporate Dinner. Topic TBA. No Q&A.

Treasury Auctions:

1:00 - 3-Year Notes

Wednesday:

12:20 - Tom Hoenig, president of the Kansas City Fed, attends a business luncheon in Denver, Colorado.

2:00 - The Fed's Beige Book is an anecdotal look at the American economy compiled by the 12 Federal Reserve Districts. The last report on April 13 showed few major developments as most districts posted modest gains in consumer spending, higher auto sales, a rebound in tourism, and a pick-up in manufacturing.

But much has changed since. Stock markets have declined the last five weeks, the May employment report was a disaster, consumer confidence fell to its lowest level in a year, and manufacturing slowed down pretty dramatically.

"It now seems likely that second-quarter GDP growth (we expect 2.0%) will be little different from the first (1.8%)," said IHS Global Insight, predicting "a prolonged and subdued recovery."

Analysts at Nomura Global Economics said the Beige Book should give insight on how much of the recent slowdown is attributable directly to Japan's March 11 earthquake and tsunami.

"Districts that are heavily laden with manufacturing are likely to make note of that sector's drag on the local economy," they said. "We are bound to hear about the continuing decline of housing prices in most regions, as well as the lingering effects of higher energy prices on both business and household spending decisions, despite falling prices in recent weeks."

Treasury Auctions:

1:00 - 10-Year Notes

Thursday:

5:00 - Charles Plosser, president of the Philadelphia Fed, speaks on the economic outlook to the Society of Business Economists in London.

8:30 - Supply disruptions from the Japanese earthquake and tsunami should limit imports in April, while a weak dollar is helping exports to remain a key driver of second-quarter growth. Still, economists expect April's Trade Balance to produce a deficit of roughly $49 billion, a slightly wider gap than March's $48.2 billion figure.

"Although April trade figures reported by Japan showed roughly a $2.5 billion decline in exports from a year ago, inbound container data reported by US ports pointed to a solid increase in goods imports in the month," said economists at Nomura, who said there is " much uncertainty" in their forecast given the disruptions from Japan.

"Moreover, petroleum import prices were still on the march upward in April and should exert negative pressure on the trade deficit," they added. "Against this backdrop, we forecast a $50.9 billion deficit for April, which is $2.7 billion wider than the previous month."

Against the consensus, Citigroup expect the deficit to narrow to $45.5 billion.

"We expect that the April trade deficit narrowed substantially, after posting a large increase in March," they wrote. "In the March report, both exports and imports jumped by record or near record levels. We suspect there will be some retrenchment. In addition, motor vehicle imports likely fell sharply due to the pullback in activity from the tragedy in Japan."

8:30 - Initial Jobless Claims continue to remain above the 400k mark. The last report showed 422k new filings for unemployment insurance, with the four-week average at 425,250. This week's number is forecast at 418k, which would push the four-week average to a six-week low, according to economists at Citi.

"We do not expect next week's initial claims for unemployment insurance to be affected in any significant way by special factors, such as bad weather," said economists at Nomura. "As a result, claims will likely fall to the lower end of the recent 410k-430k range in the coming weeks, but stay above the 300k-level of March."

10:00 - Wholesale Trade Inventories are anticipated to rise 1% in April, in line with the 1.1% and 1% increases of the prior two months. Forecasts for the report, which isn't exactly a market-shaker but does have implications for GDP, range from 0.5% to 1.5%.

"Wholesale inventories are largely affected by increases in commodity prices, and prices were still on the rise in April," said economists at Nomura. "Sales, too, can be inflated by rising prices and we expect an increase of 0.5% in April on top of 2.9% in March."

Once again, disruptions from the Japanese earthquake adds an element of uncertainty to the report, warranting downside risks for inventories and sales.

"Fundamentally speaking, however, the year-over-year growth in sales continues to outstrip growth in inventories, which implies the need for further inventory building on the horizon," Nomura said.

11:30 - Janet Yellen, president of the San Francisco Fed, speaks to the Cleveland Federal Reserve Bank Policy Forum on housing.

30-year Fannie Mae and Freddie Mac MBS coupons begin the monthly settlement process. READ MORE ABOUT THE ROLL

Treasury Auctions:

1:00 - 30-Year Notes

Friday:

9:00 - Federal Reserve Bank of New York President William Dudley speaks on the national and regional economy before the Brooklyn Chamber of Commerce. Audience Q&A expected.

2:00 - The Treasury's Budget Statement for May is unlikely to bolster spirits. The monthly deficit is expected to come in at $140 billion, with forecasts ranging from $130 - $165 billion. While the April figure - typically a surplus month given tax season -

was just $40.5 billion, a comparison to May 2010 is what the market looks at. And by that measure, forecast still don't look pretty. The May 2010 deficit was $135.9 billion.

According to Bloomberg, the average deficit for the May has been $90 billion over the last decade and $120.4 billion over the past five years.

CURRENT GUIDANCE: With "The Wall" now torn down a path has been paved for mortgage rates to continue improving. An extended rally will not come without setbacks though. Short-term corrections are to be expected along the way. That means borrowers who are working on a shorter lock/float timeline should remain defensive. Your main goal is to protect new, lower rate quotes from short-term market fluctuations,which could happen as early as Monday and last all week. The overall bullish trend is very much in tact though. Intermediate to longer-term scenarios are more than justified in floating.