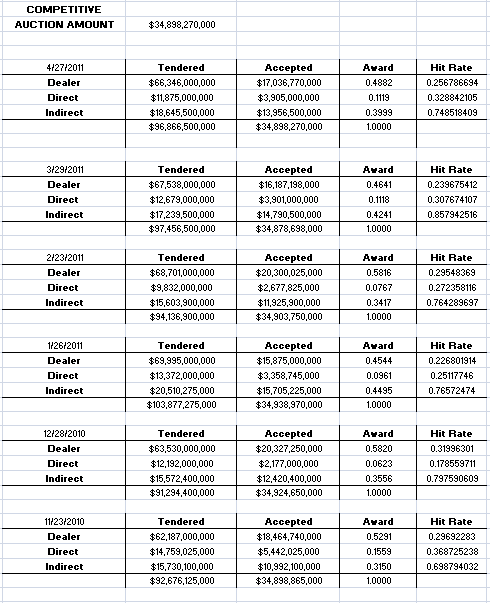

Treasury just auctioned $35bn 5s.

The bid to cover ratio, a measure of auction demand, was 2.77 bids submitted for every 1 accepted by Treasury. This is just above the five auction average but below the 2.80 ten auction average.

The high yield printed at 2.124% vs. the 11:30 "When Issued" yield of 2.121%. This is the sixth time 5s have tailed WI in the last seven auctions.

Dealers added $17.0bn in new inventory or 48.8% of the competitive bid. This takedown is below the five auction average of 52% and on the screws vs. the ten auction average.The street got 25.7% of what it bid on (hit rate) which is close to average.

Direct bidders were awarded $3.9bn or 11.2% of the competitive bid. This takedown is slightly above both the five and ten auction averages. Of particular note is a 32.9% hit rate. The highest seen since the November 2010 auction.

Indirect bidders took home $13.9bn or 39.9% of the competitive bid. This award is above the five auction average of 37.7% but the 41.1% ten auction average.

Plain and Simple: "Close to average" was the theme. The auction came and went with little fanfare...as would be expected ahead of a high-risk event like the FOMC Statement/Bernanke Press Conference. Technicians should mark their charts with the high-yield at 2.124% as an important pivot.

Market Reaction...

After forced buying in the form of short covering pushed benchmark 10yr yields all the way to a key inflection level yesterday, 10s are feeling the pain of short selling today. Ahead of the 1230 FOMC Statment...the 10yr note has drifted back to 3.36%. Another key inflection level....in this case support. If 3.36 is broken we'd short sellers to push for a breakdown of 3.40-3.42 support. If bonds like what the Fed has to say...there isn't much in the way of resistance blocking 10s from another shot at 3.30%.

FNCL 4.5s have given back yesterday's price gains and returned to a familiar pivot point at 102-10....where support has been found.

REPRICE OUTLOOK: Even though "rate sheet influential" MBS prices are down 6/32, C30 loan pricing is basically unchanged today vs. rate sheets yesterday morning. This makes sense as most lenders were hesitant to reprice for the better yesterday afternoon, so there was some cushion in loan pricing to absorb weakness in the secondary market after the afternoon rally. That said, if FNCL 4.5 prices drop another 4-5 ticks from current levels...reprices for the worse will be likely. On the other hand, if FNCL 4.5 prices recover current intraday losses and move into the green...rate sheets will be due about 0.125 in rebate.

Watch out for a knee-jerk reaction at 1230. Here is a look at my screens...