The coming days offer little in the way of macroeconomic data, but the sparsely populated calendar does hold new stats on the housing markets.

"Housing will dominate the news in the upcoming week," said economists at IHS Global Insight. "February's housing numbers were deplorable, but they were probably dragged down by special factors such as weather and building code changes. March will bring better numbers, but the improvement will be payback, not the long anticipated pickup in demand from an improving job market."

With housing numbers expected to remain poor, the continuation of first-quarter earnings will likely take center stage. After a disappointing start to earnings season last week, equity investors are hoping to hear an encouraging tone in the week ahead. Citibank and Texas Instruments report on Monday. Goldman Sachs, Intel and IBM report on Tuesday. Apple, AT&T and Wells Fargo on Wednesday. Morgan Stanley and Verizon print Thursday.

Markets will be closed on Friday in observance of Good Friday

In his morning note, MND's Managing Editor Adam Quinones points out newly confirmed bullish sentiments in the benchmark 10-year note after key support was held at 3.50% last week. He cites a short squeeze as the underlying technical driver of the rates rally but called attention to weakening fundamental outlooks and a potentially poor earnings season ahead thanks to rising energy prices and fallout from the earthquake in Japan. He is looking for the market to confirm a break of 3.40% before benchmarks make a run at 3.31% resistance. This would bode well for home loan borrowing costs but he doesn't see conventional Best Execution Mortgage Rates moving below 4.875% without a sustained break of 3.17% in 10 year notes and a sharp flattening of the MBS yield curve.

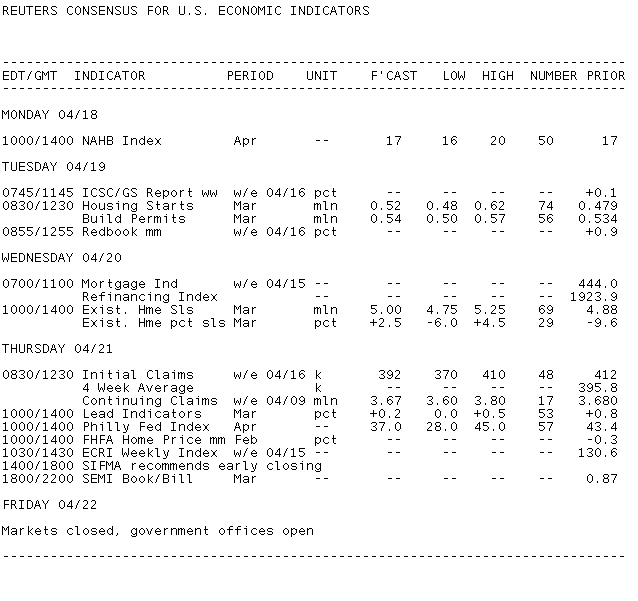

Key Events This Week:

Monday:

10:00 - Don't expect the Housing Market Index to be of any significance. The NAHB index tracks home builder sentiment and there's little for them to be more optimistic this month. Any score below 50 represents pessimism in the industry, and the last time this index was above 20 was August 2007. Last's month score was 17.

"Tight lending standards for mortgages and expectations of further declines in house prices depressed housing activity in April," added economists at Nomura Global Economics. "Our forecast for the NAHB index is 17, unchanged from the previous month."

10:00 - Federal Reserve Bank of Atlanta President Dennis Lockhart and Federal Reserve Bank of Dallas President Richard Fisher lead discussion, "Making Monetary Policy in a Globalized World" before the World Affairs Council of Atlanta. No Lockhart or Fisher media Q&A. Fisher audience Q&A expected.

12:00 - Federal Reserve Bank of St. Louis President James Bullard speaks on "The U.S. Economic Situation and Recent Monetary Policy Developments" before an event hosted by the Kentucky Department of Financial Institutions. Audience and Media Q&A expected.

12:45 - Federal Reserve Bank of Dallas President Richard Fisher speaks on "Making Monetary Policy in a Globalized World" before the Rotary Club of Atlanta. Audience and media Q&As expected.

Tuesday:

8:30 - The five-month average for Housing Starts has been relatively flat since the summer of 2009, but the month-to-month figures are wild and unpredictable. In February the index dropped a mind-numbing 22.5% to their second-lowest in the records book (which date back to 1946), but the month before in jumped 18.4%. So what's expected this month? Another big jump.

Economists polled by Thomson Reuters look for the annual pace of housing starts to leap 9.6% to 525k per year. Estimates, of course, all all over the place, from half-a-million to 625k.

"Melting snow in the Northeast and Midwest and a payback from building code changes in the West - which boosted starts in December and January at February's expense - may have played a role in February's deplorable numbers," said economists at IHS Global Insight. "We are expecting much better numbers for March, but these increases will be payback numbers, not numbers pointing to a pickup in demand."

Economists at BBVA advise keeping expectations low for the coming year.

"The housing market continues to struggle with foreclosures despite robust economic recovery," they said. "Significant declines in existing home prices attract buyers and limit demand for new homes and therefore, we expect housing starts and building permits to improve but remain weak throughout the year."

Wednesday:

10:00 - Existing Home Sales are also anticipated to jump in March following a significant downturn in February. Sales of previously-owned homes tumbled 9.6% to an annual pace of 4.88 million in February, breaking a three-month trend in the other direction. Economists forecast a rise to 5 million this time around.

Single-family home sales, the key component in the report, are expected to rise with help from lower prices: median prices were down 5.2% year-over-year in the last report.

Economists at BBVA, while predicting a sales increase in March, say housing market fundamentals are bleak and predict the residential sector will remain so in the first half of the year.

Thursday:

8:30 - The four-week average of Initial Jobless Claims has remained below 400k for seven straight now but markets weren't happy when the last survey showed weekly claims jump 27k to 412k - the highest figure since the week ending Feb. 12. The Labor Dept. attributed the jump to seasonal issues, so economists are hoping the figure retraces this week. The Street's forecast is 390k, consistent with the four-week average.

"Initial claims needs to remain below 375k in order to see sustainable and robust employment growth in nonfarm payrolls," say economists at BBVA, who noted the pace of employment growth is merely gradual right now. "We expect initial claims to remain around 400k."

10:00 - The Empire Fed index beat expectations last week, prompting forecasters to hope the trend extends to the rest of the Northeast. Economists look for the Philadelphia Fed Index to come in at a robust 36.0 in April - well above the zero threshold indicating growth. However, that score would represent a sizable drop from the 43.4 recorded in March - the strongest reading in 26 years.

"Several uncertainties, such as higher input costs and a potential shortage of Japanese-manufactured parts could slow down the pace of expansion in the manufacturing sector," said economists at Nomura Global Economics. "Against this backdrop, we expect the Philadelphia Fed's business sentiment index of manufacturers to decline to 32.0 in April from 43.4 previously."

10:00 - Leading Economic Indicators, a composite measure designed to track turning points in the economy, is set to rise 0.3% in March. The first two months of the first-quarter saw gains of 0.1% and 0.8%, so this would be roughly in line. Economists reacted to the previous survey suggesting that the index was pointing to a strong economic recovery.

"The greatest positive contribution is an improvement in vendor performance from the ISM manufacturing [index], which will contributed about 0.5 percentage points," said economists at Nomura. "An equivalent drag on the leading index is the drop in the University of Michigan's index of consumer expectations."

10:00 - The Federal Housing Finance Agency's Housing Price Index is forecast to show prices remain below last year's levels. The index last said prices were 16.5% below their peak in April 2007. According to economists at BBVA, prices continue to decline due to high foreclosure rates and banks short-selling in the housing market.

Treasury Auctions:

11:30 - 5-Year TIPS

Friday:

Good Friday - markets closed.